.jpg)

Managing rental funds can be tricky, and mistakes with security deposits can lead to disputes, legal headaches, or lost trust with tenants. Escrow services offer an easy way to keep money secure, stay compliant, and streamline accounting—whether you’re handling one property or a growing portfolio. In this guide, we’ll discuss multiple escrow service options from traditional banks to digital platforms to help you manage deposits efficiently and professionally.

Key takeaways

- Many states require landlords to use escrow-style accounts for security deposits to avoid illegal commingling of funds.

- Modern online real estate escrow services offer faster processing times and lower fees compared to traditional institutions.

- Understanding fee structures helps you choose the best escrow service without eroding your profit margins.

- Automated financial tools can replicate escrow functions for rental management, saving time on administrative tasks.

Role of escrow in rental property management

Escrow is the financial safety net of the real estate industry. You use escrow services to hold security deposits for your property. In many states, such as Connecticut, you are legally required to hold tenant deposits in an escrow account at a state-based financial institution. While in other states, such as California, this is not a legal requirement.

Learn how to manage escrow accounts by separating tenant money from your operating capital, ensuring you comply with strict state laws regarding tenant assets.

Why do you need escrow services for rental management

One of the core reasons for using escrow services is to maintain the separation of funds to avoid commingling funds. This occurs when you mix tenant security deposits with your personal income or general operating expenses. Depending on the state you have property in, you might be legally required to open an escrow account for security deposits to keep these funds separate.

Why separation matters

If a tenant sues you for the return of their deposit and you cannot prove the money was held separately, you could face triple damages in court. Credible escrow services for real estate management protect you from this liability.

Types of escrow services available

Choosing the right escrow service depends on your state laws, the scale of your portfolio, and how you want to track your finances.

1. Traditional bank escrow services

These are the standard options for holding security deposits or managing mortgage-related transactions.

Banks offer high security and are often required by state law to hold security deposits. They are especially useful when escrow accounts are legally mandated, but they can be less flexible and slower than digital alternatives. Opening an account may require an in-person visit, making it better suited to long-term property transactions rather than frequent rental management.

2. Online escrow services

Digital platforms have made security deposit management faster and more convenient. Online escrow services allow you to set up and manage deposits remotely, often settling transactions within 24–48 hours. This is particularly helpful for high-turnover properties, such as vacation rentals, or for out-of-state landlords who need to manage funds without visiting a branch.

Even when not legally required, keeping funds in an online escrow account ensures clear tracking, easier accounting, and simpler handling of deductions at the end of a tenancy.

3. Hybrid escrow solutions

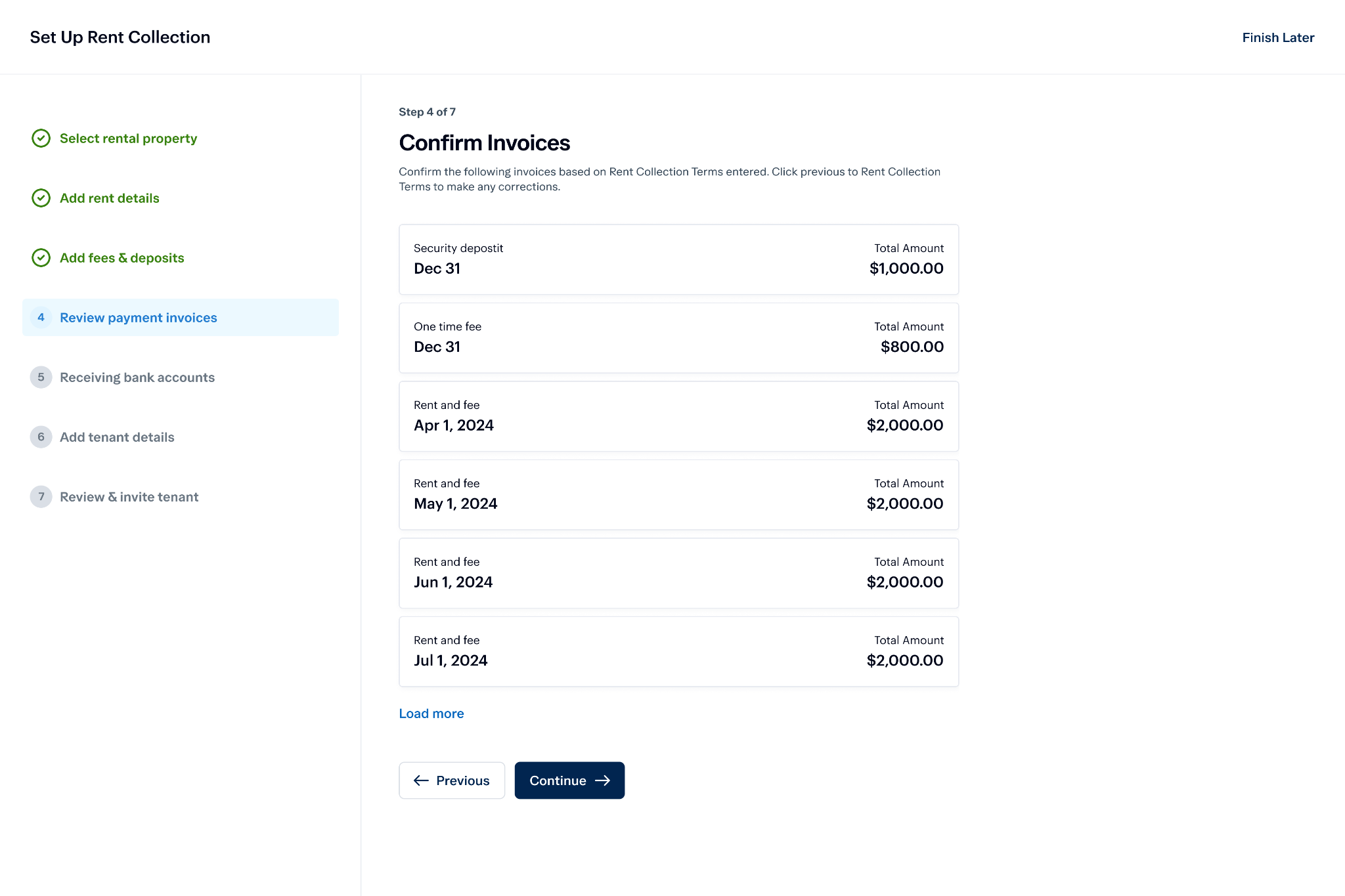

Some landlords prefer to combine the security of a traditional bank account with the convenience of digital platforms. With this approach, you collect security deposits from tenants through a digital banking platform and transfer them to a state-based bank for compliance. This setup provides a clear financial record of deposits while ensuring compliance with state requirements and giving you full control over the funds.

Baselane, for example, helps you do this with ease. You can create rent invoices for tenants, collect funds in a dedicated account, connect your bank account, and transfer funds. As Baselane also offers automated bookkeeping, you can keep a record of the funds, while the actual money sits securely in the bank.

Cost considerations for escrow services

The cost of using escrow services varies depending on the type of service and the level of convenience or compliance required. Understanding these costs can help you choose the option that best fits your portfolio and budget.

- Traditional bank escrow accounts: Charge setup fees, monthly maintenance fees, or per-transaction charges. Costs are often higher if in-person visits or paperwork are required. Traditional bank escrow accounts are often required in states that legally mandate holding security deposits in a separate account.

- Online escrow services: Flat fee per transaction or a small percentage of the funds held in escrow. While these fees can add up for high-turnover properties, online services save time and administrative effort, which can offset the cost.

- Hybrid escrow solutions: Combination of fees. The platform may charge a small transaction fee or subscription, while the bank account could have minimal maintenance costs.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Best practices for holding security deposits

Managing security deposits is the most common "escrow" activity for a landlord. Understanding how a security deposit is determined and managing it in accordance with state guidelines can help you collect the right amount and keep your rentals secure.

Assess the security deposit amount

Most states limit the security deposit to one or two months' rent. Check your state security deposit limit to make sure you’re not overcharging. Read our guide on how much a security deposit a landlord can charge to know your state’s deposit limit.

Once you determine the security deposit amount, collect it before the tenant moves in, ideally within one week of the lease being signed.

It is critical to distinguish between security deposit and rental deposit terms in your lease to avoid confusion. A "rental deposit" might sometimes refer to holding fees, whereas a security deposit is refundable.

Pay attention to interest rate and compliance

In some states, landlords are required to pay interest on security deposits held in escrow. To comply, the account must be interest-bearing, regardless of whether it is technically an escrow account. Learn about the tenant deposit interest rules for your state.

There are two main types of accounts you can use:

- Interest-bearing escrow account: An account where security deposits are held in escrow and accrue interest, which must be paid to the tenant.

- Interest-bearing account (non-escrow): An account (savings or HYSA) that accrues interest under specific state requirements, even if the funds are not held in a formal escrow account.

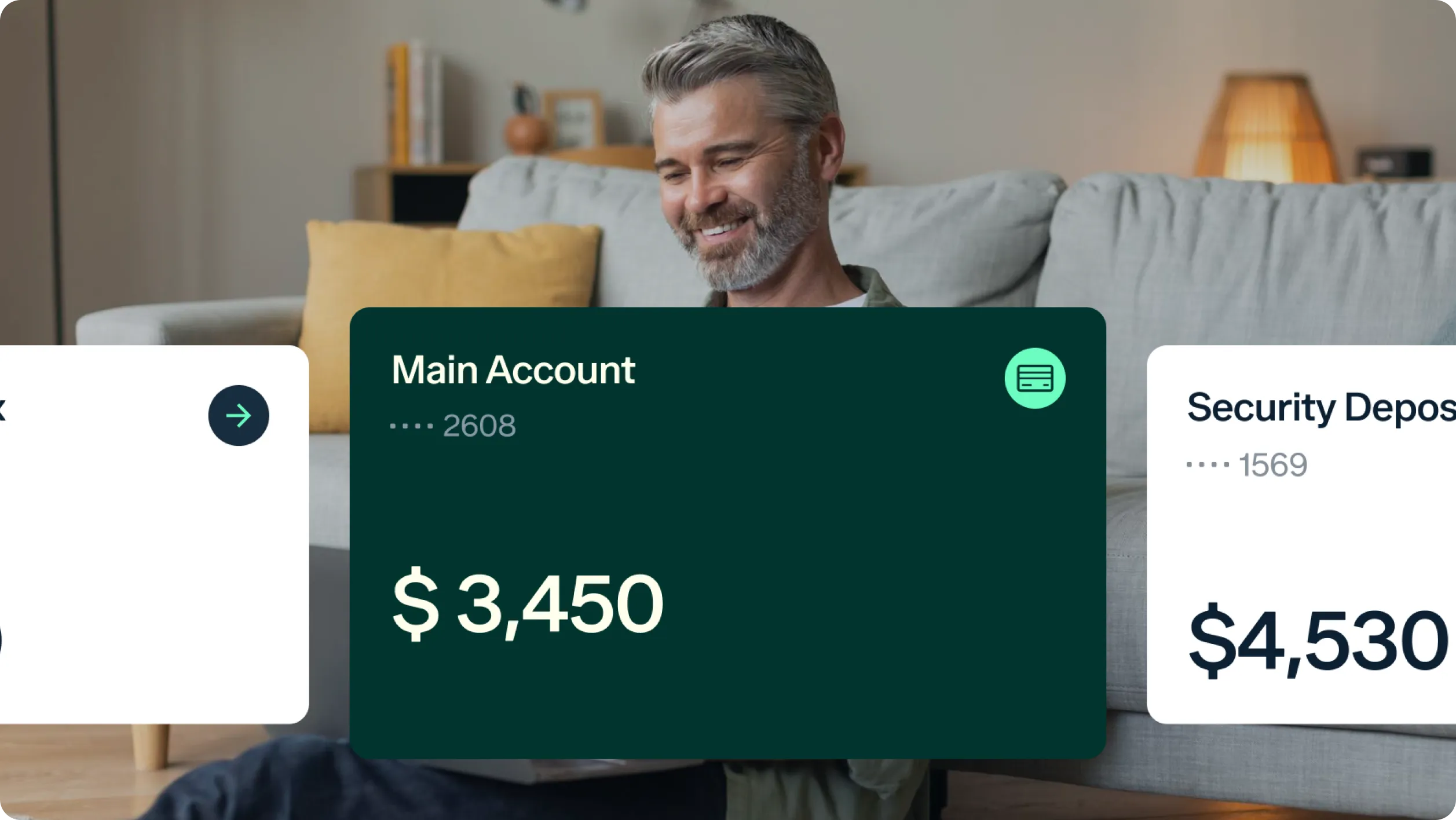

In states where escrow is not mandated, but interest is, Baselane’s high-yield savings accounts are one of the best options to earn and pay interest to tenants. You get upto [v="apyvalue"] APY², which you can transfer to the tenant directly at the end of tenancy or as per the state interest payment timelines.

Understand the refund process and timeline

When a tenant moves out, you need to return the security deposit. You typically have 14 to 30 days (some states allow up to 60 days) to return the funds in full or provide tenants with a list of security deposit deductions. Almost all the states mandate deductions, including unpaid rent, fees, utilities, damages beyond normal wear and tear, and cleaning costs.

You should send a formal security deposit refund letter detailing any withheld amounts. Always keep copies of the rent and security deposit receipts and the final deductions for your records.

Strategies for vacation and short-term rentals

Short-term rentals (STRs) introduce a different dynamic. You may need escrow services for vacation rentals to hold booking funds when booking directly rather than through Airbnb or VRBO.

Fraud prevention

A free escrow service for vacation rentals (or a low-cost one) can prevent fraud by holding the guest's money until check-in. This builds trust among guests wary of direct booking scams.

Managing turnover

With high turnover, you need a system that moves fast. Renting third-party escrow services can automate the collection and release of damage deposits for STRs. However, many hosts rely on the platform's resolution center or maintain a capital reserve in a separate account to self-insure against minor damages.

Choosing the best escrow service for your portfolio

Selecting the best escrow service depends on your specific needs.

- For rental deposits: Avoid paying monthly fees to third parties. Instead, use a banking platform that allows you to lease multiple security deposits in separate sub-accounts.

- For high-volume rentals: Consider online real estate escrow services with API integrations if you manage hundreds of units.

Additional use cases for escrow in rental management

While most landlords use escrow primarily to manage security deposits, there are other scenarios where escrow can play a role in rental management.

Rent escrow for disputes

In cases where a property becomes uninhabitable and the landlord fails to make necessary repairs, tenants may legally place rent into an escrow account through a court or local agency. This ensures the funds are secure until the issue is resolved. While not part of routine rental management, knowing how this works highlights the importance of proactive property maintenance and financial transparency.

Third-party rent collection services

Some landlords voluntarily use services that act as an escrow for rent collection. Rent is paid to the service, verified, and then transferred to the landlord. This adds security but can create slight delays. A more efficient alternative is an integrated banking solution that deposits rent straight into a dedicated account, keeping funds separated while maintaining speed and transparency.

Secure tenant deposit with escrow services

Proper escrow management simplifies bookkeeping, protects tenants’ money, and strengthens your credibility as a landlord. By using Baselane, you can collect, track, and securely transfer deposits to compliant external accounts, ensuring a smooth and clear escrow management. Open your account today!

FAQs

Do banks offer escrow services for landlords?

Yes, many banks offer escrow services for landlords, specifically for holding security deposits. However, they often require in-person setup and may charge monthly maintenance fees compared to modern digital banking platforms.

How much does an online escrow service cost?

Escrow service cost for online platforms typically ranges from 0.89% to 3.25% of the transaction value. Some services charge a flat fee of $25 to $50 for standard rental deposit transactions.

Can I use a personal account instead of a rental escrow service?

In many states, it is illegal to mix tenant deposits with personal funds in a standard personal account. You need to use a separate account that functions as an escrow to avoid liability and comply with tenant-landlord laws.

What is the fastest escrow service for rentals?

Digital escrow services are generally the fastest, often settling transactions within 24 to 48 hours. They use electronic transfers and automated verification to speed up the process compared to traditional paper-heavy methods.

.jpg)