Managing rental income isn’t as simple as putting checks into your personal account. The bank account you choose affects taxes, liability, bookkeeping, and even your credibility as a landlord. Let’s break down the difference between business vs personal accounts specifically for real estate investors and landlords, so you can make the right choice for your portfolio.

Key takeaways

- A personal bank account vs. a business account exposes your personal assets to potential legal issues. Using a business account under an LLC or corporation provides an extra layer of protection.

- Mixing personal and rental funds in a personal account increases the likelihood of missed deductions and overreported income. A business checking account vs a personal account ensures property-specific tracking for easier Schedule E reporting.

- Business banking vs. personal banking offers more robust features for landlords, including multi-user access, accounting integrations, rent collection, and higher transaction limits.

- Using a personal account vs a business account may be fine for one property, but a business account signals professionalism, supports scaling your portfolio, and improves relationships with lenders, partners, and contractors.

- Even sole proprietors benefit from a business bank account. Business banking vs personal banking offers cleaner financial records, clearer cash flow, and better preparation for tax season.

Key difference between a business and a personal account

When it comes to handling rental income, the type of bank account you use can make or break your financial organization. Here’s a detailed look at a business bank account vs a personal bank account.

Purpose of the account

Personal accounts: Designed for daily personal spending, like paying for groceries, bills, or subscriptions. While you can use them for rent deposits, they’re not meant to support business-level transaction needs or financial reporting.

Business accounts: A business bank account for a sole proprietor is built to manage income and expenses for your rental property. It’s structured to separate your business activity from your personal finances, giving you a clearer picture of cash flow and profitability.

Ownership & liability

Personal accounts: If you use your personal bank account for rental income, your personal and property finances are mixed. That means any legal issue tied to your rental property could potentially affect your personal finances.

For example, if a tenant slips on your property and decides to sue, your personal savings could be at risk if your rentals aren’t legally separated.

Business accounts: A business account tied to an LLC or corporation keeps your rental income and property expenses separate from your personal finances. This separation protects personal assets, like your home or savings, if a legal issue occurs. This is why investors with multiple properties or LLCs often use business accounts. A business account adds an extra layer of protection that a personal account cannot, even if you own a handful of units.

Taxes & accounting

Personal accounts: When rental income and personal funds live in the same account, tax filing becomes overwhelming. You end up spending hours combing through bank statements to separate mortgage payments, property taxes, repairs, insurance, and everyday personal spending. Over time, it becomes harder—and honestly exhausting—to know what’s deductible and what’s not.

The bigger issue is that this setup increases the risk of overpaying taxes. When expenses aren’t clearly tracked or properly documented, many landlords miss legitimate deductions. That means your net rental income can look higher on paper than it actually is, which can lead to a higher tax bill and mistakes on Schedule E.

Business accounts: A business account keeps your real estate finances away from personal ones, which makes bookkeeping much easier. Your CPA will thank you because it’s easier to prepare taxes, claim deductions, and ensure accuracy in reporting.

Fees, features, & bank support

Personal accounts: Typically, personal accounts have lower fees and fewer minimum balance requirements. But if you start managing multiple properties, they may not support frequent transactions, ACH payments, or integrated accounting, which makes tracking multiple rentals difficult.

Business accounts: Business accounts may have slightly higher fees, but they often include perks valuable to landlords: unlimited transactions, free or low-cost ACH payments for rent, and high-yield interest. Banks also usually offer credit cards, lines of credit, and business loans more easily through business accounts.

To help you compare, here’s a breakdown of typical costs and features for business and personal accounts used for rental property management:

Rent collection & cash flow management

Personal accounts: You can accept rent payments through a personal account, but mixing it with your everyday spending makes it hard to see your actual cash flow. You might lose track of which income came from which property, making it difficult to measure profitability.

Business accounts: Business accounts allow you to track rent and expenses for each property clearly, sometimes even letting you integrate directly with property management software. This makes it easy to measure property-specific profits and understand where your money is going.

Credibility & growth potential

Personal accounts: For one or two rental units, a personal account may be sufficient. But lenders, partners, or contractors may see using a personal account as less professional, which can affect your ability to grow your business.

Business accounts: Using a business account signals that you are a serious investor. It can make it easier to secure financing, work with partners, or attract tenants who see you as a professional landlord.

Business account vs personal account comparison table

When to use a personal bank account

Here are situations where a personal account can make sense:

- You own one rental and haven’t formed a legal entity like an LLC or sole proprietorship.

- Your rental income is minimal, and you want simple bookkeeping.

- You don’t anticipate legal issues or scaling anytime soon.

- You’re just ready to invest in a dedicated property management software for real estate investors.

When to use a business bank account

A business account is almost always better if you fit any of these situations:

- You own several rentals and need to track cash flow per property.

- You operate under an LLC or legal entity and need to maintain liability protection.

- You are planning to grow beyond a few properties or bring in partners.

- Working with lenders, contractors, or property managers where credibility matters.

- You want organized, property-specific statements to make tax deductions and Schedule E reporting easier.

- You’re applying for loans or setting up a Roth IRA for a real estate strategy.

How to open a business bank account

You can open a business bank account through one of the best banks for real estate investors (Chase, Axos, Wells Fargo) or a digital real estate banking platform (Baselane). The process is largely similar: you provide your business documents (LLC paperwork or EIN), verify your identity, and link the account to your tax ID.

The key difference is that Baselane, an all-in-one banking platform, is explicitly built for real estate investors and landlords. They not only handle your business banking needs but also make tracking rental income, expenses, and property-specific cash flow much easier than traditional banks.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Next, let’s walk through how to set up a business bank account with Baselane so you can manage your rental finances efficiently.

How to set up a business bank account with Baselane

Baselane makes it simple for real estate investors to open and manage business bank accounts.

To open a Baselane business checking account, you first create a Baselane account, then add a business banking account. It takes no longer than a few minutes online to complete the application.

Step 1: Get your info ready

Before you start, gather:

- Your government ID (like a driver’s license or passport).

- Your business EIN (for LLC, corporation, or partnership; required for Baselane business entities).

- Your business formation documents (Articles of Organization/Incorporation, partnership agreement, etc.).

- Your business address and basic details (industry, ownership, contact info).

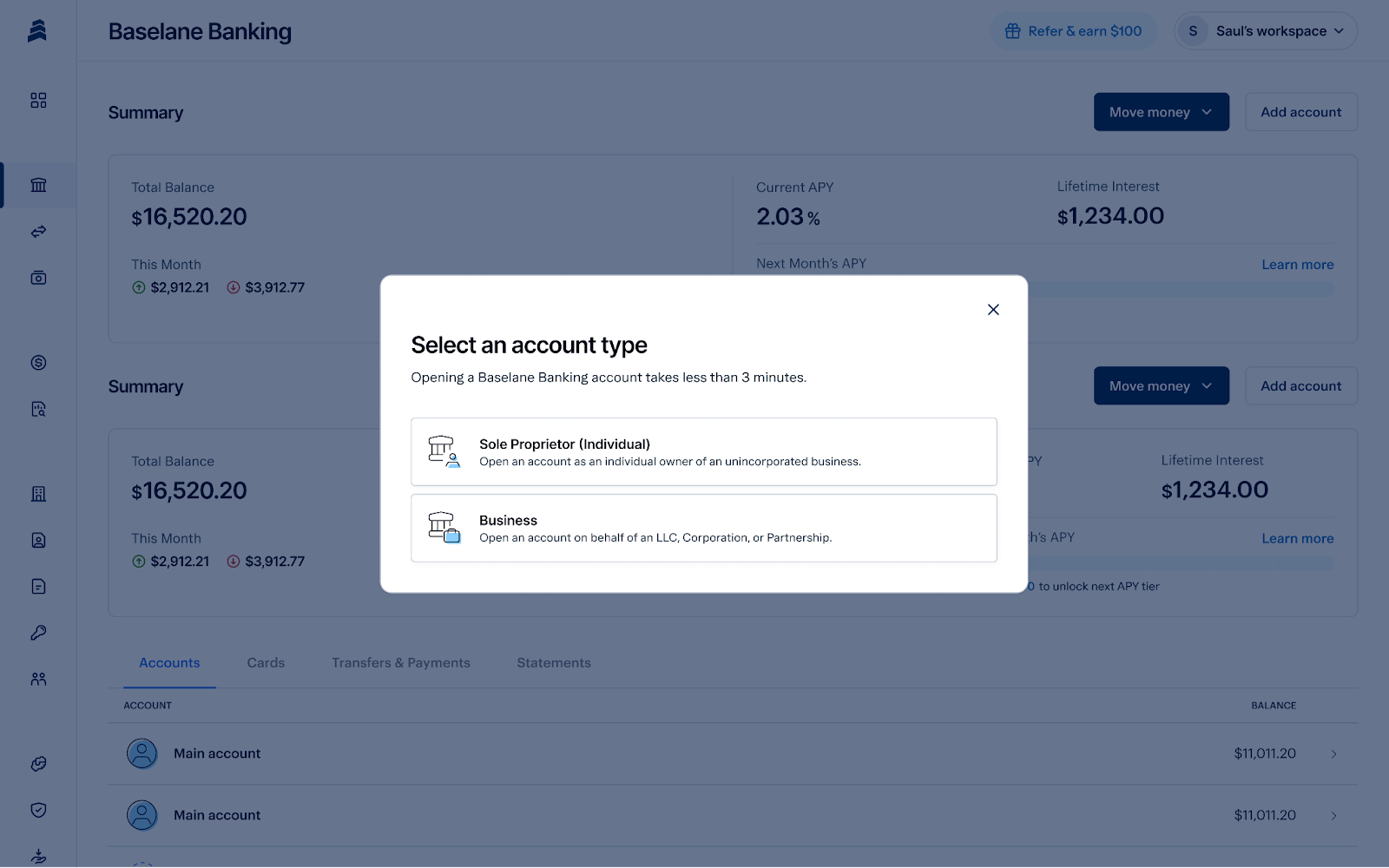

Step 2: Start the banking application

- Log in to your Baselane account dashboard.

- Go to the “Banking” tab > Click “Add Account.”

- Choose “Business entity” when asked for the account type, then pick your business type (LLC, corporation, partnership, etc.).

Note for sole proprietors: Even if you’re operating as a sole proprietor and aren’t legally required to open a business bank account, using a dedicated business account for your rental properties is still a smart move. It helps keep rental income and expenses separate from personal spending, makes tax reporting easier, and gives you a clearer picture of your property’s cash flow.

Step 4: Enter business and personal details

- Type in your business information: legal name, business type, EIN, business address, and industry.

- Enter your personal details: name, home address, date of birth, SSN (for identity check), and contact information.

- Upload any requested documents, such as your formation documents and proof of address, so Baselane can verify your business.

Step 5: Apply and wait for approval

After you review and submit your application, our team will conduct identity and business verification checks. Once we verify the documents, applications are often approved within a few business days or minutes.

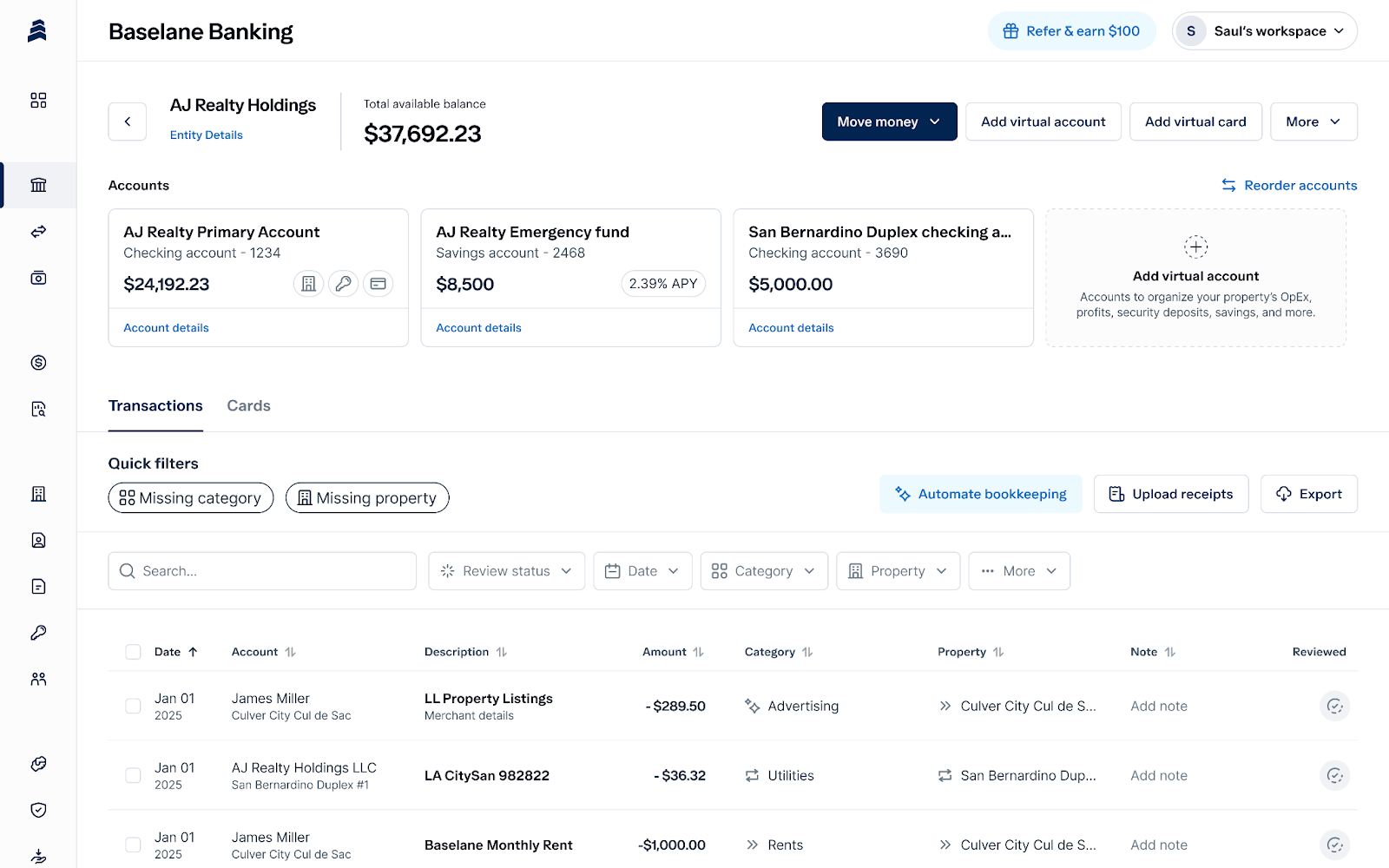

Upon approval, you will get a primary free business checking account and a debit card. At that point, you can add funds to this account or open multiple bank accounts (checking or savings) to organize your banking for specific properties.

Unlike traditional business accounts, Baselane gives you complete financial control with no extra software required. Whether you're collecting rent, managing security deposits, or preparing for tax season, Baselane helps you do it all without any monthly fees.

Looking for a smarter way to manage your rental income? Open a Baselane account and take the hassle out of property finances.

FAQs

Do I need a business bank account for rental income?

Yes. If you collect rent through an LLC or manage multiple properties, a business bank account separates funds, protects personal assets, and simplifies taxes. Personal accounts blur lines and complicate bookkeeping. It’s also a smart move for anyone—including those managing short-term rentals or HOAs. Read our guides on best bank for Airbnb business and best bank account for HOA .

What is the difference between business checking and personal?

A business account manages company or rental finances under an EIN, offering multi-user access and reporting tools. A personal account is tied to your SSN and used for individual expenses. The main difference between a personal account and a business account lies in ownership, access, and liability protection.

Can I use my personal bank account for business income?

You can, but shouldn’t. Using a personal account for business income mixes funds, weakens legal separation, and complicates tax reporting. A business account keeps transactions organized and professional.

Why separate business and personal bank accounts?

Separation ensures clear records, easier tax filing, and liability protection. Mixing accounts can cause audit issues and blur personal vs business expenses, especially for landlords with multiple properties.

What are the benefits of having a business bank account?

Business accounts provide cleaner bookkeeping, better reporting, and professional credibility. They support multiple users and integrations, and can also support security deposit management as per the state regulations.

Is a business bank account required for landlords?

It’s required for LLCs and corporations, and strongly recommended for sole proprietors. Keeping rental income separate protects your personal finances and supports accurate tax reporting. It's a smart choice if you plan to scale or adopt strategies like Roth IRA real estate investing.

How to open a business bank account for rentals?

Provide your business name, EIN, and formation documents. Choose a bank that supports landlord features and low fees—like Baselane’s business banking built for property owners.

What documents are needed to open a business bank account?

You’ll need identification, EIN, business formation papers (like LLC docs), and proof of address. Some banks may ask for your lease or ownership documents.

Do business bank accounts have higher fees than personal ones?

Usually, yes—but not always. Traditional business accounts often charge monthly or transaction fees, while personal accounts may be free. Baselane offers no-fee business banking for landlords.

What are the tax benefits of a business bank account?

A business account separates deductible expenses and rental income, making tax filing easier and reducing audit risks. Personal accounts can’t provide that clarity.