.jpg)

Whether you own a single duplex or manage multiple properties across several LLCs, your banking structure plays a major role in how protected, organized, and tax-ready your business really is. Separate bank accounts aren’t just a formality—they’re the foundation of clean bookkeeping, strong liability protection, and scalable growth.

This guide breaks down how landlords should think about LLC banking in 2026, from structure decisions to the best platforms available today.

Key takeaways

- Separate bank accounts are essential for LLC landlords to maintain liability protection, simplify bookkeeping, and stay tax-ready.

- Your LLC structure—single property, multiple properties, or holding company—should directly inform how you organize your bank accounts.

- Operating accounts and reserve accounts are the minimum every LLC should have, with additional accounts added as complexity grows.

- Banks in 2026 require stricter documentation, ownership verification, and physical address validation for LLC accounts.

- Platforms built specifically for landlords, like Baselane, make it easier to manage multiple properties and LLCs without unnecessary complexity.

Why your LLC needs separate bank accounts

By separating your LLC finances across multiple accounts, you can not only keep records neat but also protect your assets, simplify your taxes, and make your life far easier.

Protects your personal and business assets

Keeping a separate bank account for each LLC creates a clear line between personal and business finances, reinforcing that your LLC is a legitimate, independent business entity.

Liability protection is one of the biggest advantages of forming an LLC, but this protection only holds up in court if your finances are clearly separated.

Simplifies bookkeeping and tax preparation

Separate accounts for each LLC make it much easier to track income, expenses, and cash flow per property.

For example, let’s say you have three LLCs: one for a long-term multi-family building, one for a duplex, and one for a short-term vacation rental. If all the rent, maintenance payments, and mortgage transactions flow through a single account, it becomes a bookkeeping nightmare. You can end up making errors due to an overwhelming amount of transactions and lose out on tax deductions.

Separate accounts for single-person LLCs (or for multi-member LLCs) give you a clean, automatic way to categorize everything by property or portfolio, reducing stress for both you and your accountant.

Streamlines property finances

Separate accounts also make managing multiple properties far smoother.

When each LLC has its own operating account for collecting rent, paying property taxes, covering maintenance, and handling insurance, you can analyze profitability, determine cash reserves, or plan renovations. There’s no digging through a messy, consolidated account trying to figure out which transactions belong where.

Boost credibility and professionalism

A separate account for your LLC also signals to banks, lenders, and tenants that you take your business seriously. Banks often require a dedicated account for LLCs when processing loans or financing, and tenants are more likely to take you seriously if rent checks are made out to a business rather than your personal name.

Types of bank accounts your LLC needs

Not every landlord needs a separate account for every little thing—but having the right combination makes bookkeeping, tax preparation, and cash flow management much easier.

Operating account (Checking)

The operating account is the workhorse of your LLC’s finances. This is where all income and expenses related to the property flow. Think of it as the hub for daily operations:

- Income: Rent payments, short-term rental revenue, security deposits (when legally allowed to be held here), and any other property-related income.

- Expenses: Mortgage payments, property taxes, insurance premiums, utilities, maintenance, cleaning, and vendor payments.

Reserve account (Savings)

Use a reserve account to set aside money for unexpected expenses or planned capital improvements, such as emergency repairs, large scheduled upgrades, or unexpected property tax increases or insurance deductibles.

If your duplex LLC collects $3,000 in rent per month, you might allocate $500 to the reserve account each month. Over time, it builds a safety net without impacting your ability to cover regular expenses.

For more on maximizing your deposits, explore how to get a high-yield savings account or learn the key differences between a savings account vs. checking account.

Holding or capital account

If you operate a holding LLC with subsidiary LLCs, you might need a central holding or capital account. This account doesn’t handle daily property expenses, but is used for:

- Funding subsidiary LLCs with initial capital

- Receiving returns from subsidiaries if they pay distributions up to the holding company

- Consolidating funds for portfolio-level expenses or investments

Optional specialized accounts

Depending on your property type, you can also consider opening the following accounts.

- Tenant security deposit account: Some states legally require security deposits to be held in a separate account.

- Payroll account: If your LLC employs property managers, maintenance staff, or other team members directly, a separate payroll account simplifies payroll processing and tax reporting.

- Short-term rental booking account: For Airbnb or VRBO properties, some landlords create a separate account to receive platform payouts before moving funds into the main operating account. This helps track short-term rental revenue distinctly from long-term rental income.

Banking for different LLC structures: Rules & nuances

Your banking approach should match your legal setup to maximize asset protection, simplify bookkeeping, and maintain tax readiness.

Single LLC owning one property

Banking for a single property under an LLC is straightforward. You open one business checking account and use it for all property income and expenses, including rent collection, maintenance, mortgage payments, and property taxes. But make sure not mix personal and business funds as it can compromise liability protection and make bookkeeping a tedious task.

One LLC owning multiple properties

When you manage multiple properties under a single LLC for multiple properties, fund separation becomes critical. You can organize the banking structure in two ways:

Option 1: One primary account per LLC with sub-accounts for each property

You maintain one main operating account for the LLC, then create sub-accounts (or virtual accounts) for each property. Rent flows into each property’s sub-account, while expenses are paid from the corresponding sub-account or swept into the main account as needed.

This structure works well when:

- Properties are similar in size or performance

- You want fewer bank accounts to manage

- Your bank or platform offers a bank account with sub-accounts or property-level tagging

Option 2: One primary account per property and a sub-account for different use cases

In this approach, each property gets its own primary operating account, and within that account, you may create sub-accounts for specific purposes—such as reserves, taxes, or capital expenditures. Rent and expenses never mix across properties, even though they’re legally owned by the same entity.

This structure works well when:

- Properties vary significantly in size or risk

- You want clean, property-specific financial statements

- You plan to sell, refinance, or spin off individual properties later

Holding LLC with subsidiary LLCs

Many seasoned landlords use a holding company structure, where a parent LLC owns multiple subsidiary LLCs, each holding one or a few properties. This structure is especially common for landlords with short-term rentals or riskier properties, since it isolates liability.

Banking in this setup has a few important nuances:

- Separate accounts for each subsidiary LLC: Each subsidiary should have its own account for rent, mortgage, and operating expenses. This ensures you separate liabilities and clearly see property-level cash flow.

- Optional holding account: The parent LLC may have a central account for equity contributions, loan disbursements, or holding reserves. Funds are transferred to subsidiaries as needed, but day-to-day operations are conducted through subsidiary accounts.

- Documentation matters: Keep formal records of transfers between the holding company and subsidiaries. Treat these like any intercompany transaction—they’re not “free money,” and sloppy documentation can create tax or legal complications.

This approach is slightly more complex but provides the best combination of asset protection, financial clarity, and scalability.

Special considerations for vacation rentals or riskier units

Short-term rentals carry unique risks—liability from guests, higher maintenance costs, or stricter insurance requirements. It’s a good practice to isolate these properties in separate LLCs with dedicated accounts to protect other long-term holdings.

- Account naming: Clearly name accounts by property or LLC to avoid confusion. For example: “Sunset Villas LLC – Operations” rather than “LLC Bank Account 1.”

- Expense segregation: Use the account strictly for property-related expenses. Maintenance, cleaning, and utilities all go here.

Best LLC banking options for landlords in 2026

The banking market has split into two camps: traditional banks with physical branches and fintech platforms. For a real estate LLC, you need a bank that minimizes fees while maximizing organization.

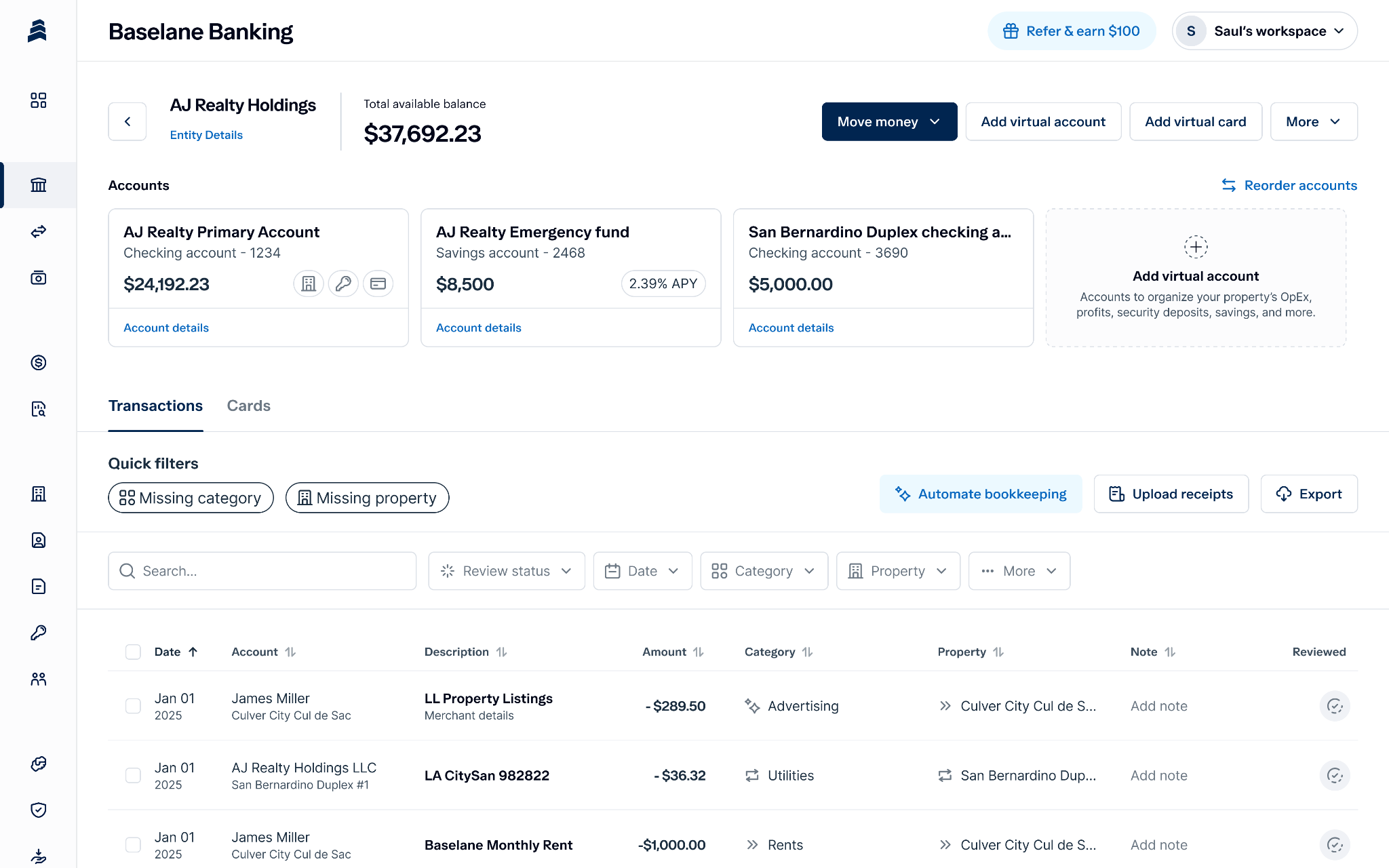

Baselane

Baselane is a landlord-first financial platform that offers integrated banking and bookkeeping to keep your LLC finances organized and tax‑ready.

Key features

- Offers unlimited checking and savings accounts per property or entity, so you can separate income, reserves, and expenses.

- Automated rent collection and tagging that links rent payments directly to the right LLC and Schedule E categories without manual entry.

- Automated bookkeeping helps you get tax-ready reports from customized tax packages to the balance sheet.

- Custom debit cards with spend controls make it easier to manage property‑related spending and share cards with property managers or contractors.

Pricing

Baselane’s Core tier is free, giving you access to banking and bookkeeping with no minimum balances or monthly account fees. Our paid Smart tier ($20/mo) offers advanced automations such as AI‑driven tagging, 2-day rent deposits, and shared access.

Baselane has made managing the finances a ton easier. As someone with multiple entities and partners, it makes it really easy to see things at the property and LLC levels. ~ Antonio Cucciniello owns 11 properties under multiple entities

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Relay

Relay is a digital business banking platform for small businesses and is great for landlords who want to organize multiple bank accounts under one business and give team members controlled access. Relay doesn’t specialize in rentals, but its cash‑flow tools can help you keep funds separated by purpose.

Key features

- 50 business bank accounts per business (highest-paid tier); 20 on the free plan.

- Physical and virtual debit cards with customizable access and controls.

- Integrations with QuickBooks, Xero, payroll tools, and payment processors.

Pricing

Starter plan costs $0/month and gives you access to core business banking. Paid plan starts at $30/month.

Novo

Novo is a simple, fee‑free online business checking account ideal for landlords and small LLCs who want straightforward banking without maintenance fees or minimum balance.

Key features

- Basic expense tracking and bookkeeping tools.

- Integrates with QuickBooks, Stripe, PayPal, and other business tools.

- Business debit card with no hidden fees and mobile banking access.

Pricing

Novo’s primary business checking is free to use, with no ongoing maintenance costs or minimums.

Lili

Lili is a small business-focused banking platform that offers built-in tax and finance tools. It’s often a good option for single‑property LLCs with straightforward banking needs.

Key features

- Cashback on eligible purchases with a debit card.

- 50+ business integrations across accounting, payroll, and payments.

- Express ACH, domestic and international wires, and check deposits.

- Team access and roles allow multiple users (like accountants) to view financial data.

Pricing

LiLi Core is free to use, and paid plans start at $15/mo.

Bluevine

Bulevine is another general‑purpose business bank with high‑yield checking options and flexibility for landlords who want to earn interest on idle funds while managing multiple sub‑accounts.

Key features

- High APY on business checking balances (up to ~3.0% on higher‑tier plans).

- Open a sub-account per property, although limited.

- Automated payments and approval workflows for team collaboration.

- Invoicing and bill‑pay tools, though not specific to LLC rental finance management.

Pricing

Offer a free plan. Paid plans start at $30/month and unlock the APY tier.

Comparison table: Top LLC banking platforms

Here is how the top online business checking account options compare:

To take your banking structure further, learn how to open a sub-bank account for each property or explore the best banks for real estate investors managing multiple units.

How financial institutions evaluate LLC accounts

Opening a business bank account for landlords in 2026 is more involved than it used to be. Banks face stricter anti-fraud and anti-money-laundering regulations, so expect more underwriting, documentation checks, and identity verification—especially for LLCs.

Essential documents and identity verification

To open a landlord bank account for an LLC, banks need to confirm the business exists and that you’re authorized to act on its behalf. While requirements vary, most institutions ask for:

- EIN (Employer Identification Number): The tax ID for your LLC.

- Articles of Organization: Prove the LLC is registered with the state.

- Operating Agreement: Used to verify ownership and who has the authority to open and manage accounts.

- Government-issued ID: Typically, a driver’s license or passport for owners or signers.

Beneficial ownership information (BOI) compliance

Under federal BOI rules, banks must identify individuals who own or control an LLC. If any of your partners owns 25% or more, they may be required to submit identification—even if they won’t be listed as an account signer.

Risk flags and address requirements

Banks also evaluate risk based on your address and activity. A P.O. Box alone is usually not acceptable; most banks require a physical street address, such as a home address or office. Virtual offices may be allowed but are reviewed more closely.

Manage LLC finances with Baselane

The right banking setup removes friction and makes bookkeeping easier, tax prep easier, and growth decisions more data-driven.

While many platforms offer general banking, Baselane stands out as purpose-built for landlords, combining banking and bookkeeping on a single platform to help you maintain clear records across properties and get real-time cash flow reports. Get started today!

FAQs

Do I need a separate bank account for single member LLC?

Yes, single-member LLC needs a separate bank account. It helps you keep funds separate and maintain liability protection.

What is the primary risk of not having a separate bank account for a real estate LLC?

The primary risk is "piercing the corporate veil." If you commingle personal and business funds, a court may rule that your LLC is not a separate entity, making you personally liable for business debts and lawsuits.

How does the Beneficial Ownership Information (BOI) rule affect opening an account?

Banks are federally required to verify the identity of anyone who owns 25% or more of an LLC or has significant control. You must provide personal identification for these individuals during the account opening process.

Can I have multiple bank accounts for one LLC?

Yes, you can, and often, for one LLC, a separate bank account is recommended. Many investors set up multiple bank accounts (or sub-accounts) for security deposits, tax reserves, and operating expenses to keep funds organized and compliant.

.jpg)