Unexpected costs are an inevitable part of owning rental property, from emergency repairs like a burst pipe to covering rent during a vacancy period. A reserve account is your essential financial safety net, helping you manage these surprises without derailing your cash flow or plans. Establishing reserve accounts is a crucial step for every landlord and property manager aiming for stability and long-term success.

Key takeaways

- A reserve account is dedicated savings for planned and unexpected rental property expenses.

- It protects your investment from financial shocks like major repairs or vacancies.

- The amount to keep in reserves varies based on property specifics and risk tolerance.

- Common calculation methods include months of rent or a percentage of income.

- Consistent contributions and replenishment are key to a healthy reserve balance.

What is a reserve account?

In the context of rental properties, a reserve account is a dedicated fund set aside specifically to cover future expenses related to the property. It acts as a buffer against unforeseen costs and planned capital expenditures. Think of it as your property's emergency fund and future investment pot.

Using a dedicated reserve account bank also keeps your business finances clear and makes bookkeeping much easier.

What type of account is a reserve account?

A reserve account is typically a type of reserve savings account or a money market account. It holds funds separate from your regular operating income and expenses. While you could theoretically use a checking reserve account, a savings or money market account is often preferred because it can earn interest over time.

For landlords, using a dedicated reserve bank account is highly recommended for clarity and tracking purposes. Mixing these funds with a personal bank or a business account is strongly discouraged for clarity and legal protection. This is distinct from concepts like an HOA reserve account, which is managed by a homeowners association, or an inventory reserve account, used in retail.

What is a reserve account used for?

A reserve account is primarily used to fund expenses that aren't part of your regular monthly operating budget. This includes unexpected repairs, tenant turnover costs, periods of vacancy, and planned upgrades. Having funds available ensures you can address issues promptly, keeping tenants happy and protecting your property's value.

Benefits of having reserve accounts as a landlord

Whether you're managing long-term rentals or short-term stays, a reserve fund kept in the right account type, like a fee-free bank account, can help you enjoy multiple benefits.

Boost property value

Timely and quality maintenance, repairs, and necessary upgrades (like a new roof or updated appliances) preserve and can even enhance your property's value. Your reserve fund makes it possible to address issues promptly and invest in the property. Waiting due to a lack of funds can lead to deterioration and reduced market value.

Reduce stress and increase peace of mind

Knowing you have a financial cushion for emergencies provides significant peace of mind. You won't be constantly worried about how you'll pay for the next repair or potential vacancy. This allows you to focus on strategic aspects of managing your properties.

Avoid creating debt for emergencies

Without a reserve, a major repair could force you to take out a loan or use high-interest credit cards, adding debt and interest costs that eat into your profits. Your reserve account helps you avoid this expensive scenario by using your own saved funds.

If a tenant leaves and you have a vacancy for months, you can pull out money from your reserve funds to cover operating expenses like electricity, repairs, etc. Having a reserve account ready means you don't have to scramble for funds or dip into a personal reserve.

Planning for large capital expenditures

As properties age, they might require huge upgrades like reinstalling appliances, roof repairs, or major renovations. Planning and saving for these expenses in advance ensures you can maintain your property's competitiveness and value.

What expenses does your reserve account cover?

Your reserve account should be prepared to cover a range of costs that fall outside your regular monthly budget. These are often unpredictable or occur infrequently, but can be substantial.

Emergency repairs

These are sudden, critical issues that require immediate attention to protect the property or tenant safety. Examples include a failed heating system in winter, a significant plumbing leak, or electrical faults. Having funds readily available is vital for timely repairs.

Common unexpected expenses and average costs

The costs of unexpected repairs can vary widely based on the issue and location. According to research, HVAC repairs might cost between $500 and $3,000. Replacing an HVAC system can range from $5,000 to $16,000. Plumbing leak repairs commonly fall between $250 and $1,000. Roof replacement is a significant expense, potentially costing between $5,700 and $16,000.

Routine maintenance & minor repairs

While some minor maintenance is budgeted monthly, larger routine tasks or clusters of small repairs can deplete regular funds. Your reserve can cover things like tree trimming, gutter cleaning, or repairing multiple small items identified during an inspection. This helps prevent small issues from becoming expensive problems.

Tenant turnover and vacancy costs

A reserve fund can cover vacancy and turnover costs including deep cleaning, painting, minor drywall repairs, and carpet cleaning. Beyond vacancy-related expenses, you can use these funds to cover operating expenses, mortgage payments, taxes, insurance, and utilities, preventing the need to use personal funds or incur debt.

Property taxes and insurance

While often predictable, unexpected increases in property taxes or insurance premiums can occur. A reserve provides a cushion to absorb these higher costs without straining your cash flow. It ensures these critical payments are always made on time.

Planned upgrades and capital improvements

Over time, properties need updates to remain competitive and attractive to tenants. This could involve a bathroom renovation, a kitchen update, or replacing major appliances. Appliance replacement typically costs between $350 and $1,700.

How much should you keep in your reserve account?

Determining the ideal reserve account balance is crucial. There's no one-size-fits-all answer, but several common strategies and factors can help you decide. The goal is to have enough set aside to handle potential issues without tying up excessive capital unnecessarily.

Common calculation strategies

Real estate experts and experienced landlords recommend several methods for calculating your reserve needs. You can choose the strategy that best fits your property and risk tolerance.

Strategy 1: X months of rent

A widely cited guideline suggests keeping a reserve equal to one month's rent per property. Some recommend a higher amount, such as 4-6 months of operating expenses, especially for newer landlords. This provides a substantial cushion.

Strategy 2: Percentage of income

Another common approach is to save a percentage of your rental income or profits. Some experts suggest setting aside 6-8% of monthly rent specifically for reserves. Others recommend saving 10% of profits monthly until a specific dollar amount is reached. This method builds the reserve over time.

Strategy 3: Fixed dollar amount

Some landlords aim for a specific dollar amount as their target reserve account balance. A common reserve account example is saving until reaching $10,000-$15,000 per property. This figure is often seen as sufficient to cover many common major repairs or extended vacancies.

Strategy 4: Capital spending study

For larger portfolios or more complex properties, a formal capital spending study can be valuable. This involves analyzing the age and condition of major systems (roof, HVAC, etc.) and estimating future replacement costs and timelines. This provides a data-driven basis for reserve calculations.

Factors influencing your ideal reserve amount

Several variables unique to your situation should influence the amount you keep in your reserve savings account. These help you tailor the general guidelines to your specific needs.

- Property Age & Condition: Older properties with original systems require larger reserves.

- Property Type & Location: Affects maintenance costs and vacancy rates.

- Number of Units: Multiple units spread risk, but could face simultaneous issues.

- Historical Turnover & Vacancy Rates: Provide valuable data for estimating future needs.

Personal Risk Tolerance: A higher reserve is advisable for greater security.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Setting up and managing your rental property reserve account

Once you've determined your target reserve account balance, the next step is to establish and maintain the fund. Proper setup and management ensure the funds are accessible when needed and kept separate from operating capital.

Here are the steps for setting up your reserve account.

Step 1: Set a clear cash reserve target

Before opening a reserve account, determine how much you should set aside. Most landlords use one of two approaches:

- Percentage of rental income: Common benchmarks range from 6-8% of gross rental income.

- Fixed dollar amount per unit: $3,000–$5,000 per unit is a common rule of thumb, depending on property age and type.

A clear target gives you a financial buffer for unexpected repairs, vacancies, and capital improvements, without derailing your cash flow.

Step 2: Sign up for a free Baselane account

Getting started with Baselane takes just a few minutes, and there are no monthly fees or minimum balance requirements.

How to open your account:

- Go to baselane.com and click “Get Started for Free.”

- Create a secure login with your email and password

- Select whether you’re opening the account as an individual (sole proprietor) or as a business entity (LLC, partnership, etc.)

- Submit the required information:

- Name, address, date of birth

- Social Security Number (SSN) or Employer Identification Number (EIN)

- Valid photo ID (driver’s license or passport)

- Name, address, date of birth

Once approved, you’ll get instant access to your Baselane dashboard, where you can open and manage unlimited accounts.

Step 3: Open your reserve account

After creating your Baselane account, it’s time to set up a dedicated account for your reserves. Keeping reserves separate from your operating capital is crucial for clear bookkeeping and financial protection.

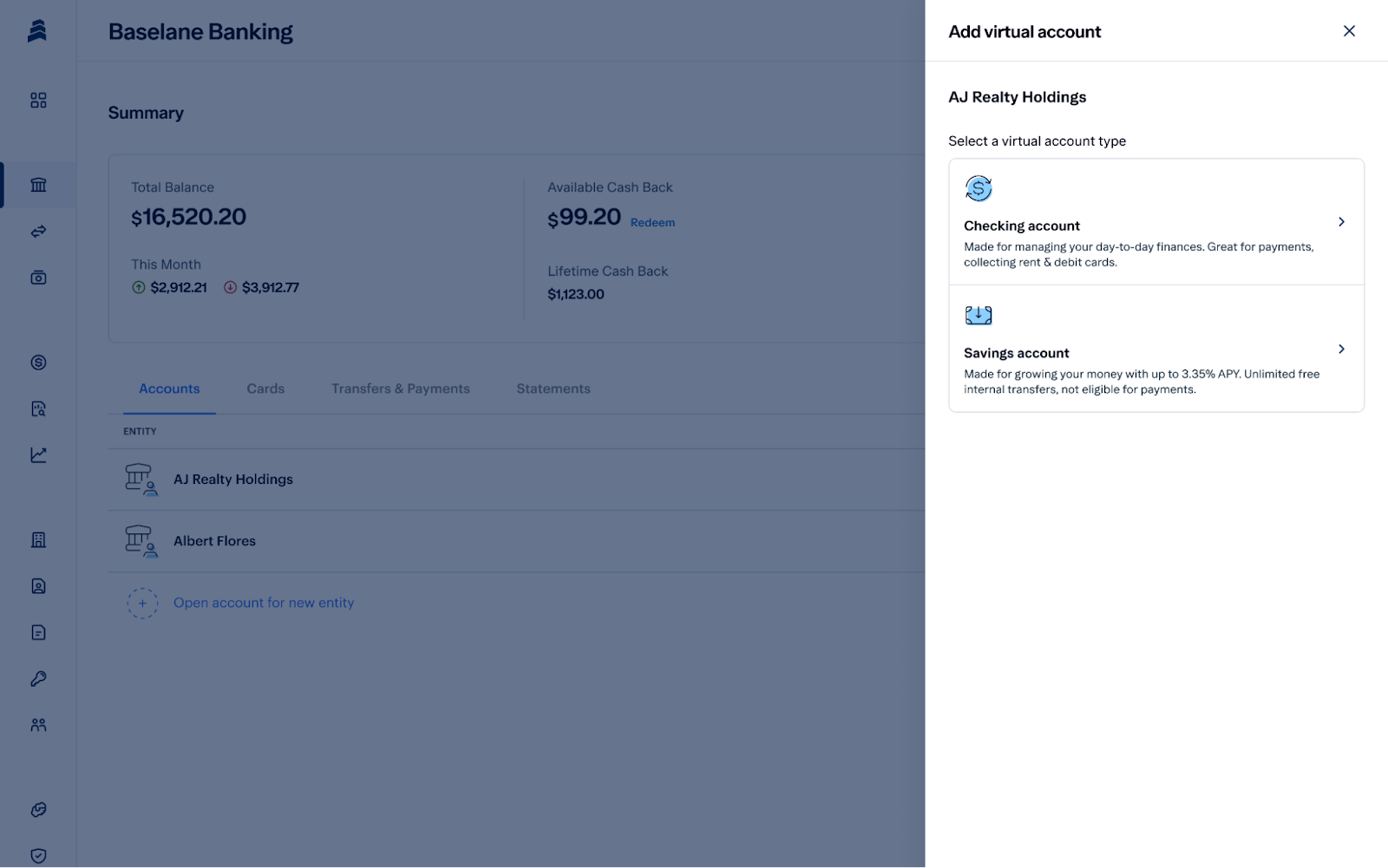

To open a reserve account in Baselane:

- From your dashboard, click “Add Account”

- Choose “Savings Account”

- Label the account (e.g., “Capital Reserves – Property A”)

- Optionally, tag the account by property or purpose to keep things organized

Baselane allows you to open unlimited savings and checking accounts under a single login, perfect for landlords managing multiple properties or entities.

Step 4: Fund your reserve account

You can fund your Baselane account in a few different ways:

- Bank transfer: Link an external account and initiate an ACH transfer

- Wire transfer: Use the wire details provided in your Baselane dashboard

- Cash deposit: Use any in-network Allpoint ATM (55,000+ locations nationwide)

- Check deposit: Log in from a mobile device and take a photo of the check

Once the money is in your Baselane checking account, you can easily move it to your designated reserve account.

Step 5: Automate your monthly contributions

Building your reserve fund is all about consistency. With Baselane, you can automate recurring transfers, so you’re always setting money aside after rent is collected.

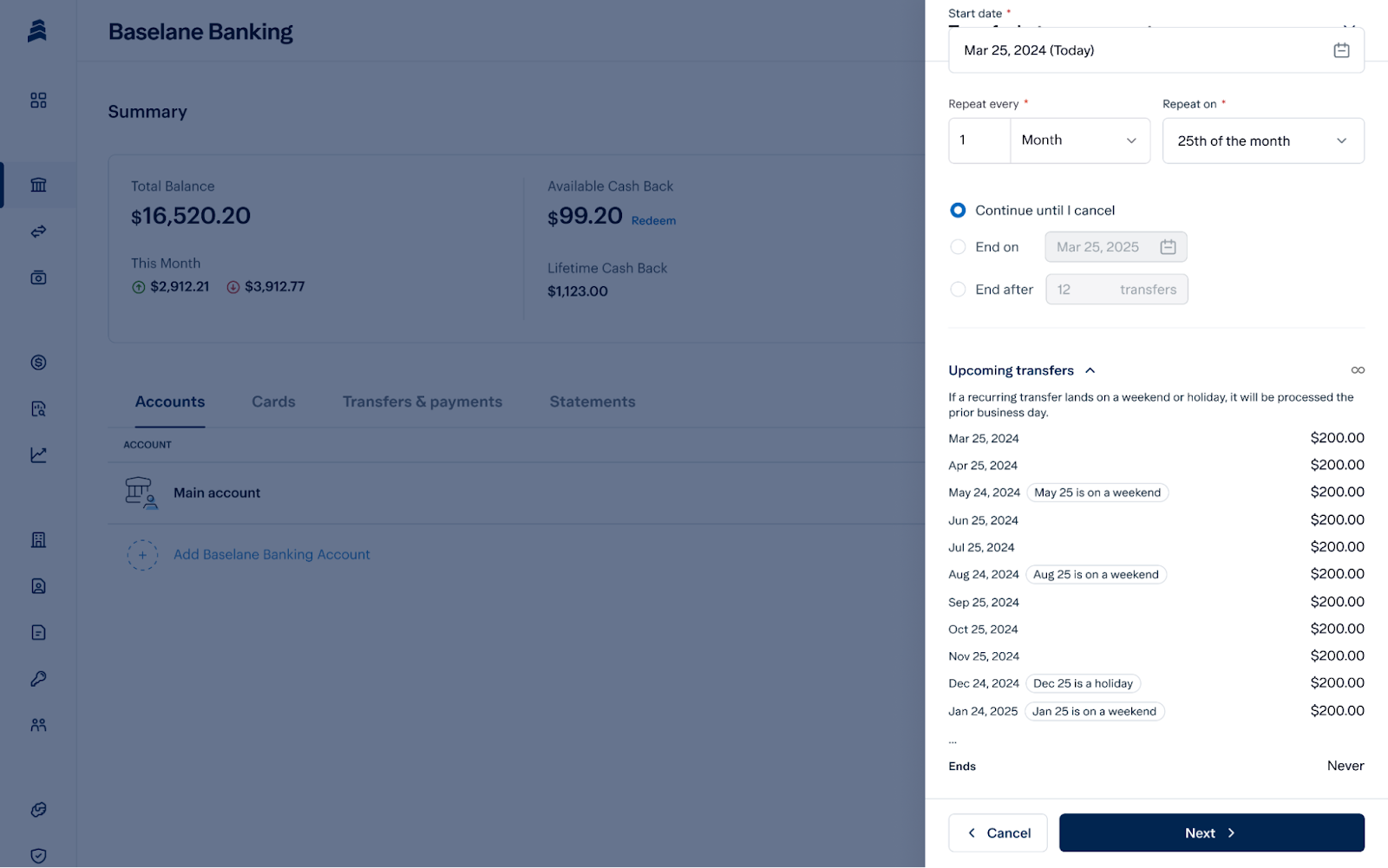

To set up an automatic transfer:

- Go to your dashboard and select “Transfer Funds”

- Choose the source (e.g., Operating Account) and destination (e.g., “Capital Reserve – Unit 3B”)

- Enter the amount and set the frequency (monthly, biweekly, etc.)

- Optionally, tag the transfer by property or category to streamline bookkeeping

You’ll get reminders, transfer logs, and visibility into upcoming transactions—all within Baselane.

Step 6: Track and optimize your reserves

With your Baselane account fully set up, you can now monitor your reserves in real time and adjust as your portfolio grows.

- Use Baselane’s dashboards to view balances, reserve targets, and property-level breakdowns

- Make updates easily, rename accounts, increase contributions, or add new accounts for each unit or reserve type

- Use Baselane’s built-in bookkeeping system to tag transactions to a specific property for smooth tax prep

How to use and manage your reserve funds

Once you’ve opened your reserve fund account, the next step is to access and start depositing money in it.

How to access and use reserve funds

Accessing reserve funds should be straightforward for legitimate reserve expenses (repairs, vacancy, etc.). Ensure your reserve account bank allows easy transfers to your operating account when needed. You'll then use the funds from your operating account to pay vendors or cover costs. Maintaining accurate records of when and why funds are withdrawn is important for bookkeeping and tax purposes. Tools that help track rental income and expenses can assist here.

Replenishing your reserve after use

After using funds from your reserve account, it's crucial to replenish it. Treat replenishing the reserve like any other essential expense. Adjust your automated contributions temporarily if necessary to build the balance back up to your target amount. Consistently maintaining your target reserve account balance ensures long-term financial stability.

Is a reserve account the same as a savings account?

This is a common question. So, is a reserve account a savings account? Not exactly, but a reserve account is typically held within a savings account or money market account. A reserve account describes the purpose of the funds; they are reserved for specific future uses related to your rental property.

A landlord's business bank account is the type of bank account that holds those funds, an account designed for saving money and often earning interest. Using a dedicated savings account makes it a reserve savings account.

Learn more about how to get a high-yield savings account.

Open a reserve account with Baselane

Building and maintaining a strong cash reserve account isn’t just good practice; it’s essential for long-term success in rental property management. A well-funded business reserve account protects you against unexpected repairs, tenant turnover, and capital expenses, all while preserving your cash flow and property value.

The most effective way to manage your reserve is with a dedicated, high-yield savings account that makes automation easy and organization simple. Baselane’s landlord banking platform is built for exactly this. With high-yield online savings accounts, unlimited virtual sub-accounts to separate funds by property or purpose, and automated transfers, you can stay financially prepared without the manual work.

Baselane also offers integrated bookkeeping, helping you manage and organize your transactions with ease. Sign up for free today.

FAQs

What is a reserve account for landlords?

A reserve account for landlords is a dedicated savings fund set aside to cover planned and unexpected expenses related to a rental property, such as major repairs, vacancies, or tenant turnover costs. It acts as a crucial financial safety net.

What type of account is a reserve account?

A reserve account for rental properties is typically held in a reserve savings account or money market account, which allows the funds to be kept separate from operating cash and potentially earn interest.

How much should I keep in my rental property reserve account?

The recommended reserve account balance varies, but common strategies include saving one month's rent per property, 6-8% of monthly rental income, or a fixed amount like $10,000-$15,000 per property. Factors like property age and condition influence the amount.

What is a reserve account used for in property management?

A reserve account in property management is used to fund significant, non-recurring expenses like emergency repairs (e.g., HVAC, plumbing), tenant turnover costs, covering costs during vacancy periods, and funding planned capital improvements.

Is a reserve account the same as a savings account?

No, they are distinct concepts. A reserve account refers to the purpose of the funds (set aside for future property needs), while a savings account is the type of account where these reserve funds are typically held to keep them separate and earn interest.