While you can make good money as an Airbnb host, running your place can cost quite a bit. Most full-time hosts earn around $56,000 a year, but remember, a big chunk of that – between 25% and 75% – goes back into repairs, supplies, and other expenses.

In this article, we will make accounting and bookkeeping simple for Airbnb investors. By the end, you'll know how to manage your Airbnb finances to keep more of what you earn.

Key takeaways

- Use separate bank accounts with a specialized banking solution like Baselane to easily track all your Airbnb income and expenses.

- Your main Airbnb expenses are the simple ones: maintenance, repairs, cleaning, utilities, and any property management fees.

- Your tax deductions fall into two groups: direct (costs tied directly to hosting) and indirect (costs tied to property ownership).

- You're responsible for correctly reporting your income and expenses on your tax returns, and using smart accounting software like TurboTax makes filing much easier.

What is Airbnb accounting?

Airbnb accounting is keeping a detailed score of all the money that comes in and goes out of your rental business.

You need to track:

- Gross earnings: The full amount guests pay (nightly rate, cleaning fees, etc.) before Airbnb takes out its fees and taxes.

- Expenses: Every dime you spend on the rental, from a new sofa to the internet bill.

- Your Ledger: A complete record where you organize and label all your income (money in) and expenses, tax reports.

The goal is to master this so you report the right numbers to the tax office, and you stop leaving money on the table by missing easy deductions.

Common Airbnb accounting problems: Why you should care

You'll quickly realize that managing your short-term rental money is more complicated than managing a long-term rental. Here are the biggest headaches you might face when doing bookkeeping for your Airbnb:

The challenge of gross vs. net income

You might only be tracking the payout that lands in your bank account, but that's your net income (what’s left over). The IRS wants to see your gross earnings (the total amount the guest paid). If you only track the net amount, you’re missing a huge deduction for the fees Airbnb already took out, which makes your taxes much harder to file.

Hidden host fees

Unlike a long-term rental, where the rent is the rent, a single Airbnb booking involves hidden fees that you need to watch out for:

- Host fees: Airbnb doesn't include the host service fees (which can be anywhere from 3% to 16% of the booking) in the 1099-K forms they send to the IRS. You have to track these expenses separately, or you’ll overpay in taxes.

- Guest fees: Guest service fees (usually around 14%) are part of your gross income, even though they go directly to Airbnb

Mixing your funds

This is the biggest mistake you can make. When you mix your personal and rental money in the same account, you make it almost impossible to tell which expense is which. This lack of separation is the fastest way to lose out on valuable tax deductions because you can't easily prove the expense was for the business.

Tracking elusive, small expenses

As a short-term rental host, you incur dozens of small, frequent expenses that Airbnb doesn't track, like:

- A quick trip to the store for a $5 lightbulb.

- The cost of new linens or kitchen supplies.

- General maintenance, repairs, and cleaning supplies.

Manually logging these transactions and saving every paper receipt is time-consuming and stressful. You need a reliable system to track these rental expenses, or you're leaving money on the table when it's tax time.

Reservation payout complexity

A single payout from Airbnb often bundles multiple reservations from various listings. If you manage a growing portfolio, this creates a major accounting challenge. You must decipher which portion of the lump-sum payout belongs to each individual property to accurately categorize your income for Schedule E on your tax return and understand each property's profit margin.

Given the complex and varied nature of Airbnb bookkeeping, it is essential that you maintain clear and accurate books and records. This attention to detail will set the stage for the next steps in managing your finances.

How to do Airbnb accounting the right way

Airbnb accounting is really a two-step process: correctly recording your gross rental income and carefully documenting all your deductible expenses.

Step 1: Record your gross rental income

Your reportable income is your "gross earnings" from the reservation. This includes the nightly rate, cleaning fees, and other guest fees, before Airbnb deducts its host fees and commissions. Since Airbnb automatically subtracts taxes and fees before depositing the payout, your reported gross income will be higher than the actual payout you receive.

This difference is covered when you report your deductible expenses.

💡Pro tip: Don't just record the payout amount. Use your Airbnb earnings summary to report the gross earnings and then deduct the host fees and other costs later.

Step 2: Track and categorize deductible expenses

The best way to lower the income you're taxed on is by deducting rental expenses. Airbnb expenses fall into two broad categories:

Direct expenses (100% deductible)

These costs are tied directly to the rental activity and are fully deductible for the days the property is rented.

- Airbnb service fees: The commissions Airbnb charges you.

- Cleaning and maintenance: Professional cleaning fees, supplies, and minor, immediate repairs.

- Guest-related supplies: Toiletries, coffee, welcome basket items, etc.

- Advertising and listing: Photography fees, marketing costs, and listing optimization services.

Indirect expenses (prorated deduction)

These are general costs associated with owning the property. If you also use the property for personal reasons, you must prorate (apportion) these expenses based on the rental use percentage.

- Utilities: Electricity, water, gas, internet, and cable for the property.

- Insurance: Property, liability, and homeowner's insurance premiums.

- Mortgage interest: Interest paid on the mortgage loan.

- Property taxes: Annual real estate taxes.

- Depreciation: An annual deduction that accounts for the wear and tear of the property and is a major tax benefit.

💡Pro tip: If you list an apartment as an Airbnb, the entire rent paid during the period a guest is staying is fully deductible. Similarly, all utilities during a guest's stay are deductible.

How to file and report your Airbnb taxes

Before you can file, you need to know how your taxes differ from long-term rentals.

Form 1099-K and 1099-NEC

Airbnb may send you a Form 1099-K (Payment Card and Third Party Network Transactions) or a 1099-NEC (Nonemployee Compensation). Even if you don't receive either form, you are still required to report all your rental income to the IRS.

- Form 1099-K: This form reports your gross earnings—the total amount guests paid for reservations through the Airbnb platform before fees or refunds. The federal reporting threshold has been lowered to 5,000$ in total earnings.

- Form 1099-NEC: This form is for reporting nonemployee compensation (if reached $600 or more), such as income earned from offering services to guests (like a local tour or photography). It is used to report this service-based income, not the income generated from renting out your property.

The gross amount on your 1099-K is not your taxable income. You must reconcile this gross figure by deducting all your eligible expenses to determine your correct taxable net income.

Here are some steps to take if you didn't receive a Form 1099 from Airbnb:

- Check your account information: Verify your account details on Airbnb. Sometimes, a simple error like an incorrect address can send the tax form to the wrong place.

- Verify business status: Double-check that your Airbnb account is set up as a business. To do this, log in to Airbnb.com, go to 'Hosting Preferences' under 'Account Settings,' and confirm that your hosting information is correctly categorized as a business.

- Calculate earnings: If your earnings from Airbnb were less than $600, Airbnb is not required to send you a Form 1099. However, this doesn't exempt you from reporting your taxable income to the IRS.

Tax forms are typically sent out by January 31st, either by mail or email. If you haven't received a 1099 Form by that date, you can still proceed with filing your taxes. However, If the income you report differs significantly from the one recorded on your 1099-K or 1099-NEC, your tax return may be flagged for review.

Schedule E vs. Schedule C

When filing your taxes, you can use one of two forms to report income and expenses:

- Schedule E (Supplemental Income and Loss): This is the most common form for hosts who provide minimal services (e.g., basic amenities, cleaning between guests, regular maintenance). Income reported here is considered passive and is not subject to self-employment tax.

- Schedule C (Profit or Loss from Business): You use this form if the average guest stay is seven days or less, OR if the stay is fewer than 30 days and you provide guests with substantial services (e.g., daily cleaning, meals, concierge services). Income reported here is considered active and is subject to self-employment tax.

Compare the best vacation rental accounting software and top Airbnb property management software to stay on top of bookings and revenue across properties. As your short-term rental portfolio grows, dedicated short-term rental property management software can help you coordinate turnover, pricing, and guest communication at scale.

Step-by-step guide to file your Airbnb taxes

Navigating taxes is simpler when you follow a clear process.

Step 1: Collect your income and expense documents

Collect all relevant financial data, including:

- Gross earnings: Your total rental income for the year, typically found on your Airbnb Earnings Summary or Form 1099-K (if received).

- Expense ledger: Your consolidated record of all deductible expenses, categorized by Schedule E (or C) categories.

- Tax forms: Any Forms 1099-K, 1099-NEC, or 1099-MISC you received.

Step 2: Determine your tax form and calculate proration

Decide whether you’re filing with Schedule E (passive rental) or Schedule C (active business).

If you use the property personally, figure out the deductible portion of indirect expenses. For example, if you rented it for 200 days out of 365, only 54.8% of indirect costs are deductible for the whole property.

As an Airbnb host, you are subject to self-employment taxes, which include Social Security and Medicare taxes, totaling approximately 15.3% of your Airbnb income.

On the local level, you should be aware of occupancy taxes, transient occupancy taxes (TOT), and local sales taxes that may apply to short-term rentals.

Airbnb may assist in collecting some of these taxes from your customers and forwarding them to the appropriate government authorities. Ultimately, you are responsible for collecting these taxes from your guests and remitting them to their local authority.

According to the IRS 14-day rule, you are not required to report taxes on income received from rentals if:

- You rent your home for no more than 14 days during the year.

- You use the home yourself for 14 days or more during the year, or at least 10% of the total days you rent it to others.

Step 3: Report income and deductions

Enter your gross income on the appropriate form (Schedule E or C) and then enter your calculated deductible expenses. You can do this on your own or take help from an accountant. Learn more about rental income management.

Step 4: Prepare for quarterly estimated taxes

As a self-employed individual or active host, you're generally required to make quarterly estimated tax payments to cover income and self-employment taxes.

- Estimate: Set aside 30-35% of your Airbnb income to cover your quarterly tax payments.

- Due dates: Payments are typically due April 15th (Quarter 1), June 15th (Quarter 2), September 15th (Quarter 3), and January 15th of the following year (Quarter 4).

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Make Airbnb bookkeeping easy with Baselane

The key to a stress-free tax season is building a solid accounting system that does the hard work for you. Baselane’s integrated banking and bookkeeping help you level the playing field and establish a home base to run your short-term rental business like a 20-unit professional operator.

Here’s how:

Maintain separate bank accounts

With Baselane, you can open unlimited checking or savings accounts for each property/unit, giving you an easy way to keep funds separated from your personal account or when you own multiple units.

Dedicated accounts immediately eliminate the biggest Airbnb accounting headache: commingling funds. Instead of trying to sort through one messy personal account, you create a dedicated business environment.

If you own 5 rental units, here’s how you can structure them in Baselane:

This dedicated structure solves the most critical financial problems for hosts:

- When you pay the property’s electricity bill from the Operating – Unit B (Lake Cabin) account, that expense is automatically tagged to Unit B, making it simple to calculate your deductible prorated amount at year-end.

- You can issue a virtual debit card attached only to the Maintenance Buffer account, set a spending limit, and give it to your maintenance vendor. If the card is used, you instantly know which pool of money was spent and on which type of expense.

Automate transaction tagging

Instead of manually going through bank statements and trying to remember what a 75$ payment to "Home Depot" was for, Baselane automated bookkeeping automates the process. It syncs transactions from all your connected accounts (internal or external) and categorizes them using over 120+ Schedule E categories.

By creating separate accounts for each rental unit and expenses, you automate the categorization of inflow and outflow of funds by property and expense type and eliminate the pain of manually tracking every elusive, small expense.

This offers you the clarity needed to reconcile the gross income on your Form 1099-K with your long list of prorated and direct deductions.

I have been using Baselane for my business for over a year now. I love everything the platform offers; I can run my short-term rentals smoothly and effectively. Everything from the ease of money transfers to the incredible bookkeeping capabilities allows me to work so effortlessly. ~ Drew Ivey

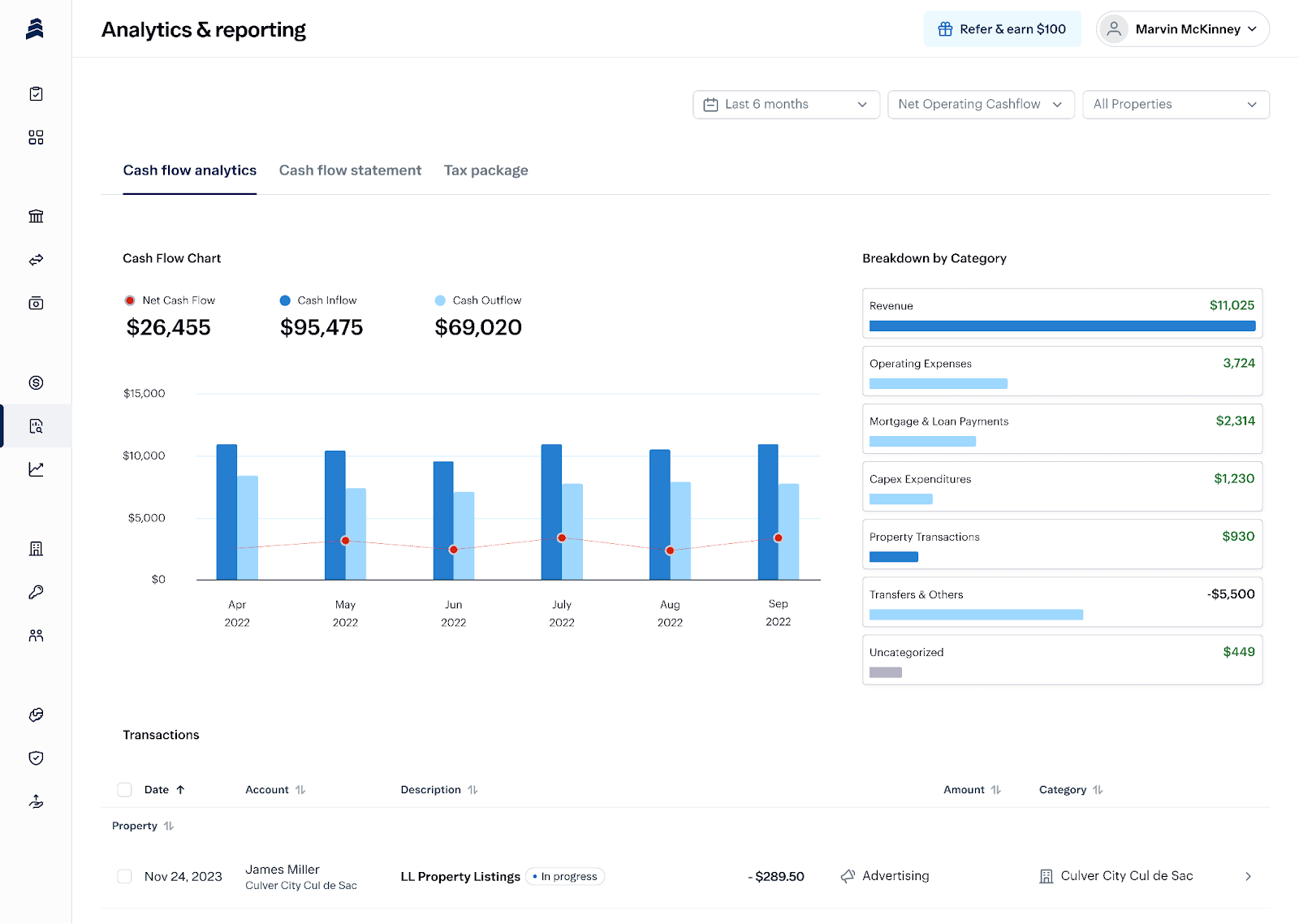

Get real-time cash flow reporting

A stunning 72% of real estate investors do not actually know their true cash-on-cash return or profit margin. Baselane solves this by generating real-time reports that are not only easy to understand but give you the ammunition you need to understand your rental business’s profitability.

- You get automated cash flow insights at property and unit level, helps you assess your actual profit—not just gross revenue.

- With property-level reporting, you can quickly see which "Operating – Unit" (e.g., Urban Loft vs. Lake Cabin) is most profitable.

- You get a customizable and downloadable tax package that includes an income statement, transaction ledger, and captured receipts. This package makes tax reporting easy and more accurate for you or your accountant.

Final thoughts

A successful Airbnb business is built on disciplined financial management. By creating separate bank accounts and automating bookkeeping, you stop letting financial busywork overwhelm you. You gain clarity and control and free up time to focus on what matters: growing your passive income.

Baselane is the best bookkeeping software for Airbnb due to its integrated banking and bookkeeping features. You can receive or send funds, keep tabs on every single transaction, and get a tax-ready package under one login. There’s no more manual reconciliation or late-night catching up on your Airbnb expenses. Baselane makes the proceeds hassle-free and gives back time to focus on growing your short-term rental business.

Get started with Baselane today and manage your finances with ease.

FAQs

Does Airbnb collect taxes such as occupancy or sales tax?

Yes, Airbnb automatically collects and remits certain taxes on behalf of hosts in areas where they have agreements with governments or are required by law. This typically applies to local taxes like occupancy taxes on vacation rental income and sometimes includes state or local sales taxes (or VAT/GST), but hosts are still responsible for assessing and manually collecting any other taxes not covered by the platform.

Is QuickBooks a good Airbnb accounting software?

While QuickBooks is a good solution for general accounting, it is not purpose-built to help you manage books for your short-term rental units effectively. It lacks essential features like automated cash flow tracking and Schedule E categories, making you do the manual reconciliation, which is time-consuming and prone to errors. Read more about accounting software for real estate.

What is Schedule E, and how does it apply to Airbnb?

Schedule E (Supplemental Income and Loss) is the IRS form most often used to report income and expenses from passive rental real estate activities. Generally, you file Schedule E if the average guest stay is longer than 7 days and you do not provide substantial services (e.g., daily maid service or meals, only cleaning between guests). If you provide substantial services or the average stay is under seven days, you may need to file Schedule C.

Do Airbnb hosts get a 1099 form?

Yes, Airbnb issues Form 1099-K (Payment Card and Third Party Network Transactions) to US hosts who meet the federal reporting threshold, which for the 2024 tax year is greater than $\$5,000$ in gross payouts. Regardless of whether you receive a 1099-K, you must still report all your rental income to the IRS.

.jpg)

%20vs%20General%20Ledger%20for%20Landlords%202026%20.jpg)