.jpg)

Did you know that a large portion of rental income may be eligible for a 20% pass-through tax deduction simply because of how the tax system treats business income? Many landlords miss out because they aren’t sure what counts as qualifying income or how to claim it properly.

In this article, we explain how to claim the rental property pass-through deduction, qualification criteria, multi-property strategies, and optimization tips to maximize your savings across your portfolio in 2026.

Key takeaways

- The QBI deduction allows eligible landlords to deduct up to 20% of their qualified business income from their taxable income.

- To qualify, your rental activity must generally rise to the level of a trade or business, often verified through the Safe Harbor rule.

- Accurate bookkeeping and separating funds are critical for proving eligibility and passing IRS scrutiny.

- High-income earners may face limitations based on W-2 wages paid or the unadjusted basis of the property.

What are pass-through tax deductions?

A pass-through deduction applies to businesses where income flows directly to the owner’s personal tax return rather than being taxed at the business level. For rental real estate, this typically occurs through entities like LLCs, sole proprietorships, partnerships, or S corporations.

The most common landlord deduction is the section 199a pass-through deduction, often called the QBI pass-through deduction. This allows eligible landlords to deduct up to 20% of their net rental income—after ordinary and necessary expenses—without reducing cash flow.

What is “qualified business income” for landlords

Qualified business income is your net rental income, calculated as Gross rental income – ordinary and necessary rental property operating expenses = QBI

Deductible expenses include:

- Repairs and maintenance

- Property management fees

- Insurance and taxes

- Utilities

- Depreciation

Understanding how your assets lose value over time is key to maximizing deductions — learn how to calculate depreciation on rental property across your portfolio.

Benefits of the pass-through tax deduction for rental property

- Lower taxes on the same cash flow: Deduct up to 20% of net rental income, directly reducing taxable income and your annual tax bill.

- Stable, long-term benefit: The QBI deduction is now permanent, letting you plan and underwrite deals with a reliable tax advantage.

- Tax efficiency grows with scale: Each additional property increases potential deductions, so your total tax savings grow as your portfolio expands.

- Portfolio-level aggregation: Grouping multiple rentals into a single enterprise can unlock deductions more easily, meeting hours, and other tests at the portfolio level.

- Higher after-tax returns: Proper structuring allows investors and sponsors to maximize QBI benefits, improving overall after-tax profitability.

Who qualifies for the pass-through deduction for landlords

A pass-through landlord is a property owner whose rental income flows to their personal return. Owning a rental under a particular entity does not automatically qualify you—the rental must be treated as a trade or business.

Common qualifying entities:

- Sole proprietorships

- LLCs taxed as pass-throughs

- S corporations

- Partnerships

If you're operating under a sole proprietorship, make sure you're capturing every eligible sole proprietorship tax write-off to reduce your taxable income.

Safe harbor rules for rental real estate

IRS provides safe harbor rules to simplify qualification, especially for rentals that might otherwise be considered passive. The rules are as follows:

- Group similar properties into a single enterprise (e.g., all residential rentals, excluding personal-use properties or triple-net leases).

- Perform at least 250 hours of rental services annually across the portfolio and keep contemporaneous records of all hours and activities performed:

- Advertising and marketing

- Tenant screening

- Lease negotiation

- Rent collection

- Maintenance coordination

- Supervision of employees or contractors

Using this safe harbor automatically deems your activity a qualified trade or business for QBI purposes, removing the need for subjective “facts and circumstances” tests.

Benefits of safe harbor rules for multi-unit owners:

- Management time across multiple units adds up quickly, making it easy to meet the 250-hour threshold.

- Up to 20% of portfolio-wide net rental income can be deducted.

- Helps maintain tax efficiency, even amid QBI phase-outs or wage/UBIA limits.

- Supports LPs, syndications, or multi-owner setups to pass QBI to investors.

- More deductions mean more cash flow available to grow your portfolio.

What usually does not count as a pass-through tax activity

- Income trapped inside a regular (C‑style) corporation. If your rental company is taxed as a full corporation that pays its own corporate income tax, then distributes after‑tax profits as dividends, that is not pass‑through in the QBI / pass‑through sense.

- Truly passive, one-off personal use situations. Sporadically renting a spare room or vacation property without tracking it like a business (no books, no intent to operate as a rental business) may not be treated the same way as a rental “trade or business” for special deductions. Read more about vacation rental tax rules.

Finding the right financial tools depends on your setup — compare the best accounting software for real estate management or explore the top accounting software for sole proprietors to match your business structure.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

How pass-through deductions work for landlords with multiple properties

When you own multiple rentals, the tax system generally looks at your rental activity as a whole, not as isolated properties. Here’s how it works:

- Calculate net rental income (QBI) per property or aggregated enterprise

- Aggregate hours and income to meet Safe Harbor rules.

- Apply 20% deduction to the total qualified business income, subject to income limits

- File on Form 8995 or 8995-A with Schedule E or K-1s.

To illustrate the impact of portfolio-level aggregation on your pass-through tax deduction rental property, consider how QBI deductions grow as you add more properties to your enterprise. By combining property expenses and income, and hours across multiple units, your total deduction can scale significantly compared to treating properties individually.

This example shows why aggregating properties under a single enterprise matters: cross-property expenses can offset income from other units, depreciation enhances the deduction without reducing cash flow, and overall portfolio-level aggregation maximizes your 20% pass-through tax deduction.

How to claim pass-through deductions on your rental properties

To claim pass-through deductions, start by clearly tracking the cash flow from each property. Record rent, fees, security deposit deductions, or any other tenant payments in a way that links directly to the property they come from.

Next, categorize all operating expenses of rental property —repairs, maintenance, insurance, property taxes, mortgage interest on rental property, and depreciation. Keep all receipts, invoices, and statements organized so you can match expenses to the correct property, and consider these rental property accounting tips to streamline your process.

When preparing your tax return, calculate QBI based on these records. The pass-through deduction is then applied to reduce the taxable portion of your rental income. After filing, continue maintaining documentation to support your deduction in case of an audit and make future tax filings faster and easier.

Common mistakes landlords make with pass-through deductions

We’ve seen multi-unit landlords make some of the following mistakes, costing them hundreds of dollars due to inaccurate deduction estimates.

- Mixing personal and rental transactions: Using the same bank account for personal and rental funds makes it hard to track cash flow. Keep separate accounts for each property or entity to ensure clean financial records.

- Tracking all properties as one lump sum: Combining multiple properties’ income and expenses can reduce accuracy and make it harder to claim QBI correctly. Track income and expenses at the property level and aggregate for reporting.

- Inconsistent expense categorization: If expenses are not classified consistently, you might miscalculate QBI, which directly reduces your deduction. Consider using one of the best AI bookkeeping software or explore the best alternative to QuickBooks to automate this process.

- Waiting until tax season to organize records: Scrambling to sort receipts or invoices during filing often leads to missed deductions or errors. Maintain organized, ongoing bookkeeping throughout the year. Review records regularly instead of waiting until filing.

These mistakes become more significant as your portfolio grows. Avoiding them requires consistent systems for tracking, categorizing, and recording every financial detail for each property.

Strategies for real estate pass-through deduction optimization

To maximize pass-through deductions, create a scalable management system that can handle your growing portfolio.

- Set up property-level tracking to see exactly how each property contributes to your qualified business income.

- Review your finances regularly, not just during tax season. This helps you identify errors, adjust expense categories, and ensure nothing is missing.

- Maintain clean, organized records. Well-kept records make it easier to claim deductions accurately, and they provide a clear picture of your portfolio’s performance.

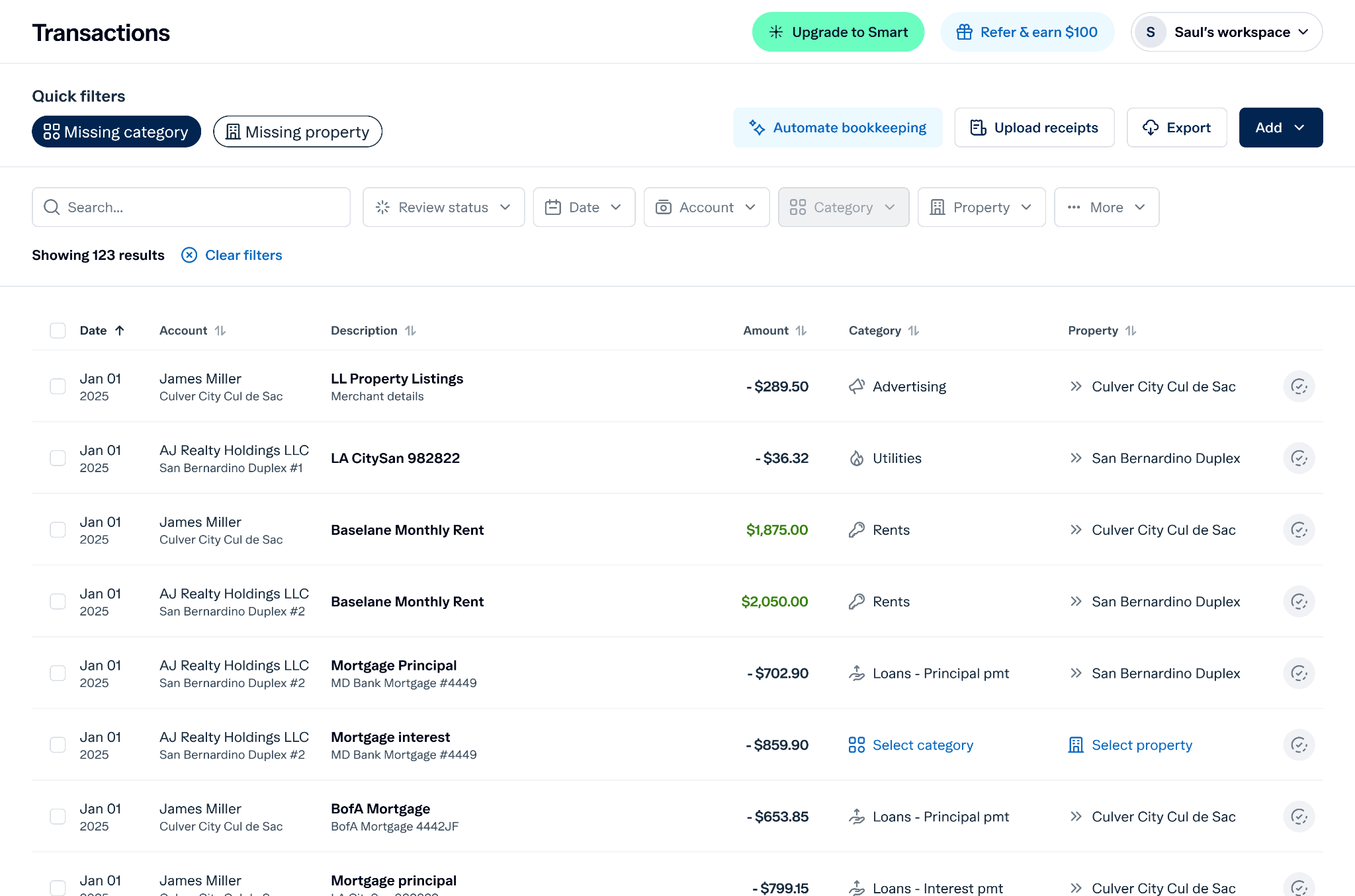

Baselane helps you automate this process through its integrated banking and bookkeeping. You open property-specific accounts and set auto-tag rules to categorize transactions based on property and Schedule E category. This helps you separate income property by property, which is crucial when you have multiple rentals.

As Baselane tags your expenses to the Schedule E category, you get property-level reporting to assess cash flow and NOI and an exportable tax package, which helps you or your CPA assess your QBI without much hassle.

Baselane helps you maintain separate records, track expenses automatically, and generate the reports your CPA needs. Don't leave money on the table due to disorganization. Start streamlining your rental finances today to ensure you are ready to maximize every deduction available. Sign up for Baselane today!

FAQs

How does the sole proprietor pass-through deduction work?

Sole proprietorship pass-through deduction is calculated based on the net profit reported on Schedule C or Schedule E. If eligible, you can deduct 20% of that net income from your taxable income on your Form 1040, subject to certain income limits and wage/asset restrictions for high earners.

Can I claim the pass-through deduction for rental property?

Yes, you can claim the pass-through rental property tax deductions if your rental activity qualifies as a "trade or business" under Section 162 or meets the IRS Safe Harbor rules. This typically requires maintaining separate books, performing at least 250 hours of rental services annually, and keeping contemporaneous records of your activities.

What expenses reduce my Qualified Business Income (QBI)?

All standard rental expenses reduce your QBI, including mortgage interest, property taxes, insurance, maintenance, management fees, and depreciation. Since the 20% deduction is applied to your net income, higher expenses result in a lower QBI deduction, though they also lower your overall taxable income.

Do high-income earners qualify for the pass-through deduction?

High-income earners may still qualify, but the deduction is subject to a phase-out and additional limitations. Once taxable income exceeds the annual threshold, the deduction may be capped based on the business's W-2 wages or the unadjusted basis of the rental property assets.

How do I track income and expenses for my Airbnb or short-term rental?

You can use a Rental Property Expenses Spreadsheet to track expenses like cleaning, maintenance, utilities, and platform fees to ensure proper QBI calculation. As your STR or vacation rental portfolio grows, consider switching to an online rental property accounting software to reduce manual workload. Use tips from our bookkeeping for Airbnb guide to record Airbnb operating expenses and income separately from personal accounts

.jpg)

.jpg)

.jpg)

.jpg)