As a real estate investor, property manager, or landlord, you know how crucial precise financial organization is for your success. Managing multiple properties, security deposits, and operating expenses can quickly become complex, leading to missed opportunities or even compliance issues. Sub-accounts offer a powerful solution, helping you gain clarity and control over your rental property finances and grow your passive income.

Key Takeaways

- Sub-accounts allow you to categorize and segregate funds within a main bank account for specific purposes.

- They provide enhanced financial organization, making budgeting, goal-setting, and reporting significantly easier.

- For real estate investors, sub-accounts are invaluable for property-specific accounting, managing security deposits, and reserving funds for capital expenditures.

- Choosing a banking platform with unlimited, unique sub-accounts and integrated tools can streamline your property management.

- Baselane offers a banking solution specifically designed for landlords, providing unlimited virtual sub-accounts and integrated financial management.

What exactly is a sub account?

A sub-account is a designated financial compartment within a primary bank account. Think of it as creating distinct "buckets" or categories for your money without opening entirely separate bank accounts. This structure enables you to organize and manage finances more effectively, offering better control and oversight of funds, expenses, and income.

Sub-accounts allow for the compartmentalization and tracking of various financial aspects. They can be used for either personal or business purposes, providing a clear view of your financial landscape. This concept helps in maintaining clarity for specific financial goals or operational needs.

While a sub-account operates under your main account, it typically has its own dedicated account number. This distinct number allows you to direct specific funds to it, such as rent payments for a particular property. Crucially, all sub-accounts usually share the same routing number as your primary account.

This distinction from entirely separate bank accounts is important for landlords. You maintain a single relationship with your bank, simplifying oversight, while gaining the organizational benefits of distinct accounts. This approach helps in streamlining your overall financial operations.

Why sub-accounts are a game-changer for your finances

Implementing sub-accounts can transform how you manage your money, bringing a new level of precision and ease to your financial life. They provide a structural advantage over traditional single-account management. This organizational tool empowers you to make smarter, data-driven decisions.

Enhanced budgeting and spending control

Sub-accounts make budgeting intuitive by allowing you to allocate funds for specific spending categories. You can dedicate money to particular expenses, ensuring funds are available when needed. This method helps prevent overspending in one area by clearly defining limits for another.

For instance, you might create sub-accounts for property taxes, utility payments, or marketing expenses. This granular control gives you real-time visibility into your available funds for each category. Such clear segmentation enhances your ability to manage your cash flow effectively.

Streamlined savings for specific goals

Setting financial goals becomes more tangible with sub-accounts. You can name your sub-savings accounts to reflect your objectives, such as "Down Payment" or "Emergency Fund”. This personalization fosters a stronger connection to your savings.

Automating transfers to these goal-specific sub-accounts ensures consistent progress without manual effort. This discipline is essential for building reserves for future investments or unexpected costs. You can open a high-yield savings account to maximize returns on these segregated funds.

Simplified tracking and reporting

Sub-accounts significantly simplify financial tracking. Each transaction can be directly linked to its relevant sub-account, making it easy to identify income and expenses for specific purposes. This detailed categorization is invaluable for accurate record-keeping.

When it comes to financial reporting, the clear segregation of funds speeds up the process. You can quickly generate reports for individual segments of your finances. This clarity helps you assess performance and prepare for tax time with minimal hassle.

Benefits of sub-accounts for real estate investors

For real estate investors, sub-accounts are not just a convenience; they are a strategic necessity for efficient property management and maximizing returns. Fragmented finances can lead to confusion and missed opportunities in a complex business like rental properties. Sub-accounts solve this by providing unparalleled clarity.

They enable you to adopt a more sophisticated property management bank account structure. This approach supports systematic financial operations across your portfolio. You can elevate your real estate financial management by leveraging these specialized accounts.

Property-specific accounting

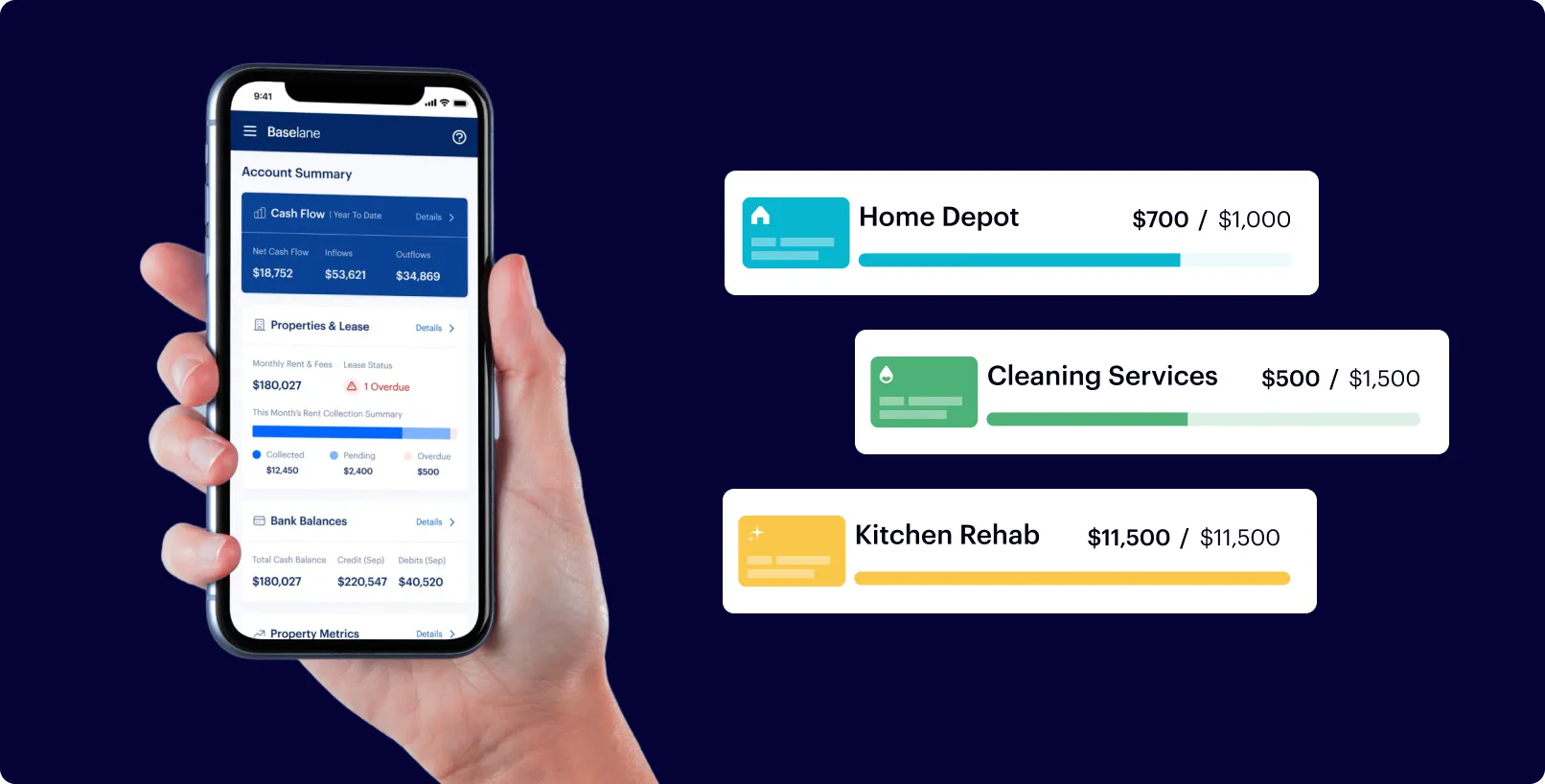

Managing multiple rental properties means tracking distinct income streams and expenses for each. Sub-accounts allow you to create a dedicated bank account for rental property, providing a clear snapshot of each property's financial performance. This clarity is crucial for assessing profitability.

For example, you can have a "123 Main Street Operating Account" and a "456 Oak Avenue Operating Account." This separation helps you understand which properties are profitable and which may need adjustments. It provides granular insights often missing in a single, commingled account.

This property-specific view streamlines expense categorization and income attribution. You can easily see rental income from one property versus another. It also simplifies the process of tracking costs like repairs, maintenance, and property taxes for each individual unit.

For short-term rentals, like Airbnb properties, having dedicated sub-accounts is equally vital. You can separate income and expenses for each listing, making it easier to analyze profitability per unit. This also streamlines tax preparation for your best bank account for airbnb.

Managing security deposit and escrow

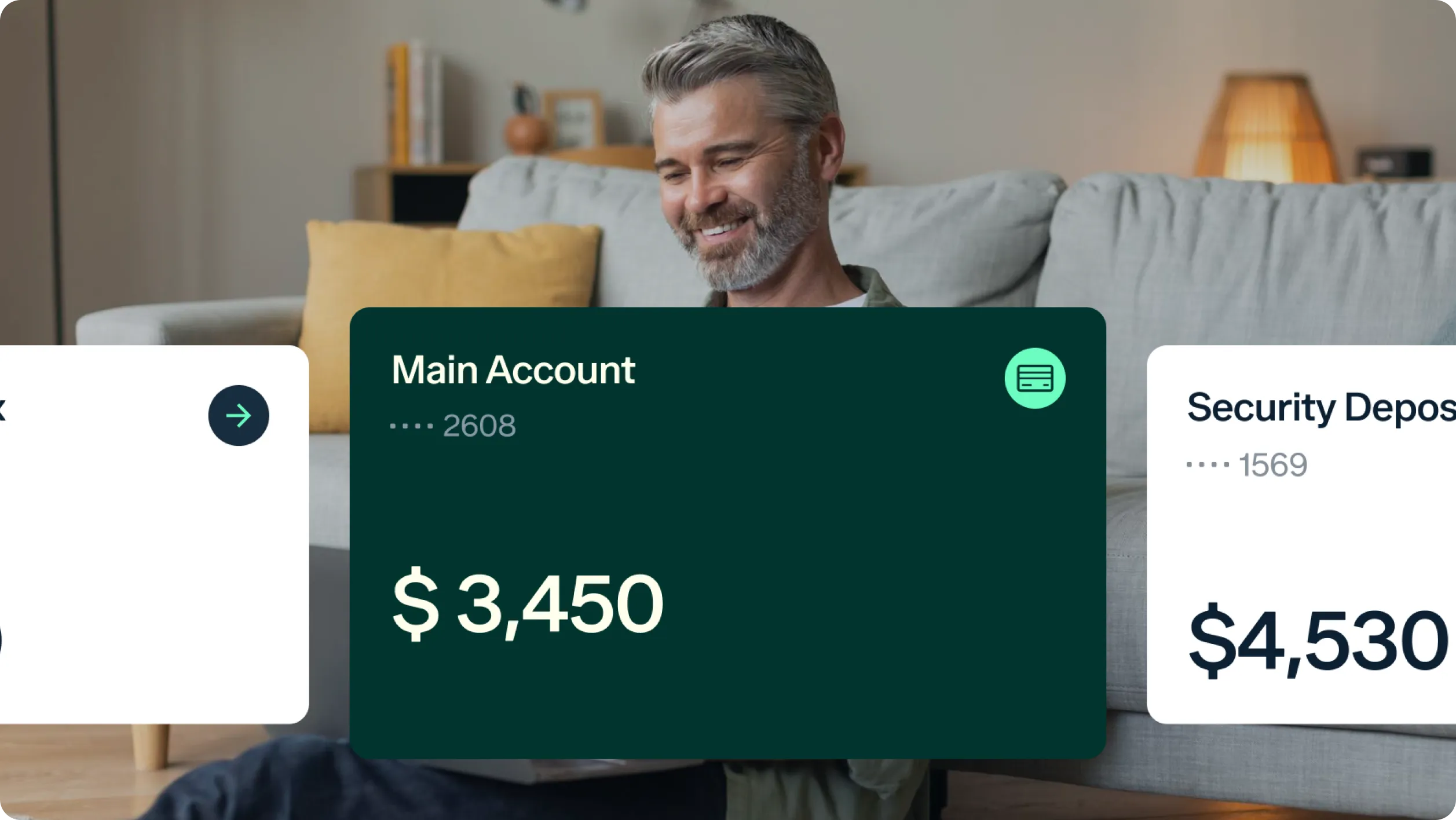

Landlords are typically required to segregate tenant security deposits from their operating funds. Sub-accounts are an ideal solution for this legal and financial requirement. You can create a distinct sub-account for each tenant's security deposit, ensuring compliance and transparency.

This segregation protects both you and your tenants. It ensures that deposit funds are always available for return, preventing accidental commingling with operational cash. Some jurisdictions may also require these deposits to earn interest in an interest reserve account.

Moreover, if you manage properties for others, sub-accounts can be used as trust or escrow accounts. This allows you to hold client funds separately and securely. It reinforces trust and ensures adherence to fiduciary responsibilities.

Capital expenditure (CapEx) and maintenance reserves

Property ownership involves inevitable repair and replacement costs. Smart investors proactively save for these significant capital expenditures (CapEx) and routine maintenance. Sub-accounts provide the perfect vehicle to build and manage these essential reserves.

You can set up distinct sub-accounts like "Roof Replacement Fund" or "HVAC Repair Reserve" for each property or across your portfolio. Consistent contributions to these accounts ensure funds are available when major repairs are needed. This proactive approach prevents unexpected cash flow crises.

Having dedicated reserves helps you maintain your properties in top condition, which can increase tenant satisfaction and property value. It allows you to undertake necessary upgrades without dipping into your operational cash or personal funds. This strategic saving contributes to long-term profitability.

Easier tax preparation and audit trails

One of the most significant benefits for landlords is simplified tax preparation. With income and expenses clearly segregated by property and purpose, gathering data for Schedule E becomes much faster. This reduces the time and effort required at tax time.

Sub-accounts provide a clear audit trail for all transactions. Should you ever face an audit, having meticulously organized funds by property and category will be invaluable. This level of detail minimizes stress and maximizes accuracy.

You can more easily keep track of rent payments and corresponding expenses for each property. This granular data helps in accurately calculating your net operating income per unit. It supports robust financial reporting for tax purposes.

Segregating business and personal funds

Maintaining a strict separation between your business and personal finances is a cornerstone of sound financial management for landlords. Sub-accounts can reinforce this critical boundary. You can clearly separate money in bank account for distinct purposes.

Even if you operate as a sole proprietorship, having designated sub-accounts for your rental business within a main account promotes financial discipline. This separation simplifies expense tracking and tax compliance. It also protects your personal assets by demonstrating clear boundaries.

This clear segregation is vital for professional credibility and potential future growth. It provides a more accurate picture of your business's financial health, independent of your personal spending. It also aids in preventing the commingling of funds, a common pitfall for new investors.

Benefits for different entity types

Regardless of your business structure, sub-accounts offer tailored advantages. For a sole proprietorship, they help establish clear financial boundaries for your rental activities. This is crucial for tax purposes and demonstrating intent to profit. You can find guidance on setting up a sole proprietorship bank account for landlords.

If you operate under a Limited Liability Company (LLC), maintaining separate finances is paramount for liability protection. Sub-accounts within your LLC's main account can segregate funds per property or for specific LLC purposes. This reinforces the corporate veil, protecting your personal assets, and you can learn how to open a limited liability company bank account.

For larger portfolios or those with multiple LLCs, sub-accounts can be linked back to a central business banking structure. This facilitates overarching financial oversight while maintaining individual property or entity distinctions. This approach helps you maintain a strong property management bank account structure across your entire portfolio.

For instance, an HOA might also benefit from sub-accounts for various community funds, such as reserve accounts for future projects or operating funds for daily expenses. Exploring options for an hoa bank could highlight how sub-accounts aid in managing diverse financial obligations within a community.

Case study/example for real estate investors

Imagine you own three rental properties: a single-family home, a duplex, and a fourplex. Without sub-accounts, all rent payments come into one main account, and all expenses are paid from it. It becomes incredibly difficult to discern which property is generating the most property management cash flow.

With sub-accounts, you establish a separate virtual account for each property. Rent for the single-family home goes into "Property A - Income," expenses for the duplex are paid from "Property B - Expenses," and so on. You also create "Property A - CapEx Reserve" for future major repairs. This provides unparalleled clarity.

At any given moment, you can see the precise profitability of each individual unit or property. This granular data allows you to make informed decisions, such as increasing rent on underperforming units or prioritizing repairs for the most valuable assets. It simplifies your financial management significantly.

How to open a sub bank account: a step-by-step guide

Opening sub-accounts is a straightforward process, especially with modern banking platforms designed for flexibility. The key is to select a banking solution that aligns with your specific needs as a real estate investor. This step-by-step guide will help you set up your sub-accounts effectively.

Step 1: Assess your needs and goals

Before opening sub-accounts, clarify what you want to achieve. Are you aiming to separate business and personal funds, track income per property, or save for specific renovations? Defining your financial goals will determine the number and types of sub-accounts you need.

Consider whether your needs are primarily personal savings goals or specific business requirements for your real estate ventures. This assessment helps you choose a bank with the right features and flexibility. Identifying these needs early ensures your sub-account structure supports your objectives.

Step 2: Choose a bank that offers sub-accounts

Not all banks provide robust sub-account functionality, especially with unique account numbers for each. Prioritize banking platforms that explicitly offer this feature, particularly those tailored to business or real estate needs. Look for platforms that allow you to customize and manage multiple sub-accounts easily.

It is important to understand that while each sub-account may have a unique account number, they typically share the same routing number as your primary account.

This means incoming payments can be directed to a specific sub-account using its unique number. Some digital banking solutions, like Baselane, offer unlimited virtual sub-accounts, which is highly beneficial for landlords managing many properties.

Step 3: Initiate the setup process

Once you've chosen a suitable banking platform, the setup process is typically initiated through their online banking portal or mobile app. You may simply click an option like "Add a Sub-Account" or "Create a New Bucket." Some banks might require you to contact customer service for initial setup.

Follow the on-screen prompts, which often involve naming the sub-account and specifying its type (e.g., checking, savings). Ensure all necessary information is provided accurately. This step is usually quick and intuitive, allowing for rapid account creation.

Step 4: Name and label your sub-accounts

Giving your sub-accounts clear, descriptive names is crucial for effective organization. Names like "Property 1 - Rent Income," "Security Deposit Fund - Tenant B," or "CapEx Reserve - Duplex" make it easy to identify their purpose. As mentioned by I Will Teach You To Be Rich, nicknames help your sub-savings accounts reflect your savings goals.

Clear labeling enhances mental accounting and promotes financial discipline. It reduces confusion and the likelihood of misallocating funds. This simple organizational step significantly improves financial clarity.

Step 5: Automate transfers for effortless management

Automating transfers between your main account and sub-accounts is key to long-term success. Set up recurring transfers for fixed expenses or savings goals, such as transferring a portion of monthly rent to a CapEx reserve. This "set it and forget it" approach ensures consistency.

Automated finances are the ultimate cure to never knowing how much you have available for specific purposes. This automation saves time and prevents manual errors. It streamlines your real estate financial management processes.

Baselane's platform allows you to automate rent collection directly into specific property sub-accounts. This feature streamlines your income management, saving you valuable time. You can set up rules to automatically categorize transactions and tag them to properties.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Choosing the right bank for your sub-accounts

Selecting the ideal banking partner is critical for leveraging sub-accounts effectively in your real estate business. Not all banking solutions offer the same level of flexibility or features crucial for landlords. You should carefully consider key functionalities before you decide how to pick a bank.

Features to prioritize

When evaluating banking platforms, look beyond just the ability to create sub-accounts. Consider features that directly support your operational needs as a landlord. These features can significantly impact your efficiency and financial oversight.

Prioritize platforms that offer unlimited sub-accounts, especially if you plan to scale your portfolio. Each sub-account should ideally have a unique account number for direct deposits and clearer tracking. This distinction is vital for maintaining clean financial records.

Look for banking solutions with no monthly fees or hidden charges. The goal is to maximize your returns, and fees can quickly erode your profits. Consider exploring avoid bank maintenance fees or best no fee checking accounts to find cost-effective options.

Integration with bookkeeping and property management tools is a major plus. This allows for automated transaction categorization and reporting, saving you countless hours.

Banks known for sub-account functionality

While traditional banks often have limitations, several modern digital banking solutions offer robust sub-account features. These platforms are increasingly popular among real estate investors due to their flexibility and integrated services. Baselane stands out as an example of such a tailored solution.

Baselane is designed specifically for landlords, offering unlimited virtual sub-accounts that can be linked directly to your properties. This allows for unparalleled organization and clarity in your financial management. FDIC insurance available up to [v="fdic_short"]¹ for funds deposited through Thread Bank; Member FDIC.¹ Pass-through insurance coverage is subject to conditions.

Other digital banking solutions like Bluevine also offer sub-accounts, with Bluevine providing up to 20 sub-accounts on its Premier Plan. These accounts typically have unique account numbers and share the same routing number as the main account. Bluevine notes that its sub-accounts are intended for general small business use, while Baselane focuses specifically on real estate investors. You can find more comprehensive comparisons of the best banks for real estate investors for your needs.

Traditional banks, while widely available, often have more restrictive sub-account options or require opening entirely separate accounts for each purpose. Digital banks like Ally might offer "buckets" or separate savings accounts, but they often lack unique account numbers for each sub-account. Therefore, evaluating your options carefully is crucial to finding the best fit for your real estate business.

Bottom line

Sub-accounts are a powerful tool for any real estate investor seeking to streamline their financial operations, gain unparalleled clarity, and ultimately grow their passive income. By enabling precise categorization and segregation of funds, they transform complex property finances into an organized, manageable system. This level of financial control empowers you to make smarter decisions and spend less time on tedious bookkeeping.

Don't let fragmented finances hold back your real estate aspirations. With the right banking solution, you can take back time and gain clarity over your investments. Explore Baselane's integrated banking solution for landlords, designed to help you organize and grow your money with ease. You can also open a high yield savings account within Baselane to maximize returns on your segregated funds.

FAQs

What is a sub-bank account?

A sub-bank account is a segregated financial compartment within your main bank account. It allows you to organize and manage funds for specific purposes, such as individual properties or savings goals, providing better control and oversight of your money. Each sub-account often has a unique account number.

How does a sub-account differ from a separate bank account?

A sub-account operates under the umbrella of your primary bank account, typically sharing the same routing number while having its own unique account number. A separate bank account is an entirely distinct account with its own unique routing and account numbers, requiring a separate application process and bank relationship.

Can you open a sub-bank account for each rental property?

Yes, modern banking platforms like Baselane allow real estate investors to open unlimited virtual sub-accounts for each rental property. This enables property-specific accounting, making it easier to track income and expenses for individual units. This feature streamlines financial management for landlords.

Do sub-accounts have unique account numbers?

Yes, typically a sub-account will have its own dedicated account number. This unique number allows you to direct specific funds, like rent payments, directly to that sub-account. However, all sub-accounts usually share the same routing number as your primary account.

What banks offer sub-accounts for real estate investors?

Many digital banking platforms are now offering robust sub-account features. Baselane is specifically designed for real estate investors, offering unlimited virtual sub-accounts with property tagging. Other digital banking solutions like Bluevine also provide sub-accounts for general business use.

.jpg)

.jpg)