Choosing the right bank for your real estate business is more than just finding a place to park your money. Your banking partner should help you manage cash flow efficiently and support your long-term growth.

While it’s easy to focus on interest rates or big-name institutions, finding the right fit takes a more strategic approach.

This guide will walk you through how to pick a bank so you can choose one that aligns with your investment goals and supports how you run your business.

Key takeaways

- Choosing a bank isn’t just about where to store your money, it’s about finding a partner that supports how you invest and grow.

- A one-size-fits-all business bank account for sole proprietor won’t cut it. The right bank should align with your investment strategy, property volume, and digital needs.

- Start by identifying your requirements based on your strategy—whether it’s buy-and-hold, BRRRR, fix-and-flip, or commercial investing.

- Look for banking features designed for real estate, like sub-accounts by property, automated rent collection, and integrated bookkeeping.

- Ask the right questions to gauge whether a bank truly understands your goals and can move quickly when needed.

- Baselane offers real estate-specific banking with built-in tools for rent collection, automated expense tracking, and more–all with no monthly fees.

How to choose a bank for a real estate business

Banking might not be the flashiest part of real estate investing, but it plays a huge role in how efficiently you operate and how quickly you can grow. From managing rent payments to securing financing, the right bank can save you time and reduce costs. Instead of settling for a generic business account, it’s worth taking the time to choose a banking solution built around the way you invest. Here's how to find one that fits.

1. Determine your real estate banking requirements

Before comparing banks, get clear on your specific needs:

Investment strategy considerations

- Buy-and-hold: Prioritize rent collection, expense tracking, and high-yield checking or savings.

- Fix-and-flip: Look for fast access to capital and flexible lending products like bridge loans.

- BRRRR strategy: Need lenders with low down payments and in-house refinancing options.

- Commercial investing: Requires higher transaction limits and specialized lending.

Scale and Volume Factors

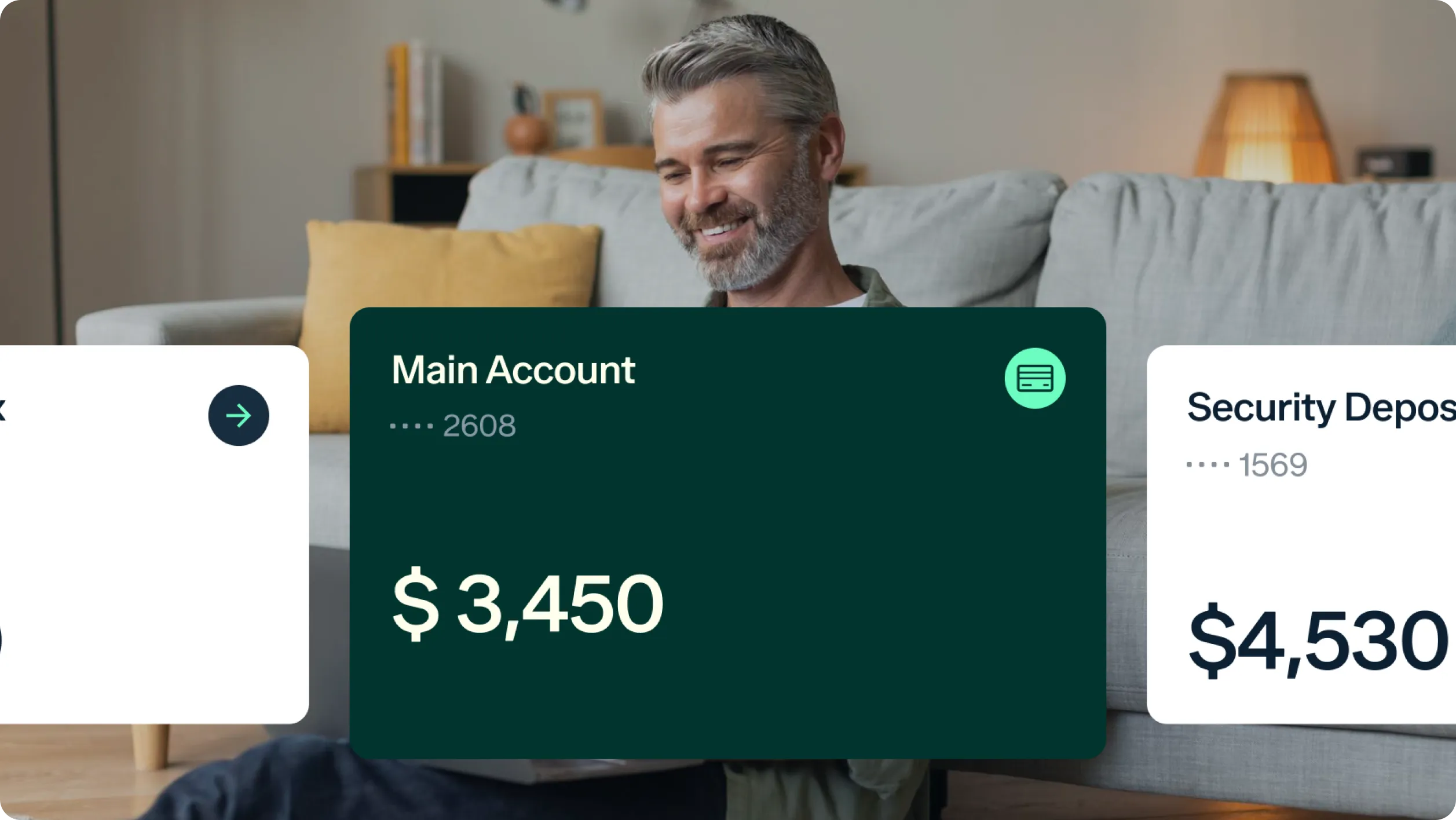

- Number of units: More properties mean more complexity. Baselane a digital real estate platform helps with this by offering virtual sub-accounts.

- Transaction volume and size: Choose banks that offers high yield savings accounts with no minimum balance.

Nearly all small business owners (97%) maintain separate operating reserve real estate accounts, and real estate investors are no exception.

Geographic Scope & Team Structure

- Local vs. out-of-state properties: Local banks offer personal support; online banks offer flexibility.

- Solo investor vs. full team: You may need role-based permissions and multi-user access.

2. Compare bank fees

Bank fees directly reduce your returns. Common charges to watch for:

- Maintenance fees: Some banks charge $15-$95/month just to keep the reserve bank account open.

- Transaction fees: Wire transfers and ACH payments can cost $15-$35.

- ATM and access fees: Out-of-network charges may add $2-$5 per withdrawal.

- Minimum balances: Avoiding fees often means keeping $1,000-$5,000+ in the account.

3. Evaluate transaction and cash management services

Your bank should support the way money moves through your business:

- High deposit and transfer limits for acquisitions or contractor payments.

- Wire and ACH capabilities with same-day options and minimal delays.

- Sub-accounts or reserve accounts to manage operating funds per property.

- Quick access to liquidity after deposits for fast-moving deals.

For active investors, especially those acquiring frequently, high transaction limits and fast fund access are essential.

4. Explore financing and loan products

Your bank should offer loan products tailored to real estate:

- Options to look for: Portfolio loans, fix-and-hold financing, lines of credit

- Favorable terms: Lower down payments, higher LTVs, fewer underwriting restrictions

- Processing speed: Conventional loans take 30–45 days; private lenders can close in under 3 weeks

- In-house lending: Prefer banks that hold and service their loans

For example, fix-and-hold loans may require as little as 10% down, compared to the usual 20-25% for traditional mortgages.

5. Look for digital banking tools and integrations

Modern real estate investing relies on strong digital infrastructure. You need a platform that’s reliable, easy to use, and built to streamline financial management.

Look for:

- User-friendly mobile and online access that makes it easy to manage finances on the go

- Built-in integrations with accounting software or property management tools

- Automated features like bill pay, recurring transfers, and real-time alerts

- Robust reporting with expense categorization and tools for tax prep and Schedule E filing

Most banks don’t offer these features out of the box, you’ll often need to pay for third-party tools or extra services to fill the gaps.

Baselane delivers built-in bookkeeping, auto-categorized transactions, rent tracking, and custom reports—designed specifically for real estate investors.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

6. Check accessibility and convenience

Think about how and where you manage your finances. Your ideal bank should match your day-to-day needs.

- Local branches are helpful if you handle cash, need safe deposit boxes, or prefer face-to-face support.

- ATM access matters if you regularly withdraw funds in multiple locations

- Bank hours should align with your business schedule

- Remote deposit tools like mobile check capture and online transfers are essential for convenience

If you work with local contractors or vendors, branch access can be a plus. But if you're managing properties from a distance, digital-first banking may offer more flexibility.

7. Consider industry expertise

One of the most underrated aspects of choosing a bank is the strength of the relationship behind it.

- Dedicated bankers who understand the real estate industry.

- Expertise in investor-specific challenges, from delayed closings to construction draws.

- Knowledge of local markets can help you make smarter decisions.

- Problem-solving support for complex transactions or unusual financing needs.

Having a banker who knows your business can save you time, unlock better terms, and help you navigate challenges more confidently.

8. Assess scalability and support

As your portfolio grows, your banking setup should grow with it.

- Multi-account structures to separate funds by property, operations, and escrow reserves.

- Business credit options, like credit cards or lines that scale with your needs

- Capacity for higher transaction volumes and more complex financial activity

- Reliable support through customer service, tech help, and educational tools

The right banking partner will adapt to your business, not hold it back, so you don’t have to switch platforms every time you expand.

9. Review security measures

Security should be a top priority, especially as digital banking becomes the norm.

- Fraud protection through real-time alerts, monitoring, and liability safeguards.

- Strong account security, like encryption and multi-factor authentication.

- FDIC insurance protects deposits up to [v="fdic_insurance_up"]¹ per account.

- Disaster recovery plans are used to ensure access during outages or disruptions.

Together, these features help protect your funds, your data, and your peace of mind as your portfolio grows.

Local vs. national vs. online banks: Which fits your needs?

Each type of bank comes with its own set of strengths and tradeoffs. Especially if you're looking for the best bank account for HOA. Understanding how they differ can help you choose the right mix for your investment strategy.

Local community banks

These small, regional banks or credit unions focus on serving specific geographic areas. They often prioritize relationship-based lending and take a hands-on approach with local investors.

Pros:

- Personalized service and direct access to decision-makers

- Strong understanding of the local market

- More flexibility with underwriting and loan structures

Cons:

- Limited branch and ATM access outside the region

- Fewer digital features or integrations

- May charge higher fees or offer lower APYs

National banks

Well-established institutions with branches and ATMs nationwide. These banks offer a wide range of services for both personal and business banking.

Pros:

- Broad branch and ATM network

- Full suite of financial products, including commercial loans

- Reliable mobile apps and online banking tools

Cons:

- Stricter lending standards

- Less personalized support

- Harder to build long-term banking relationships

Online banks

Digital-first banks that operate without physical branches. They focus on low fees, high interest rates, and seamless digital experiences.

Pros:

- Low to no monthly fees

- Higher APYs on checking and savings

- User-friendly apps, real-time tools, and 24/7 access

Cons:

- No physical locations for in-person service

- Cash deposits can be difficult

- Customer support may be less tailored

10 tips for choosing a bank

Here are things to consider when choosing a bank that will support your goals, not just store your money:

- Clarify your needs based on your investment strategy, transaction volume, and required features.

- Do your research—review bank websites, investor forums, and industry rankings to understand your options.

- Know what to ask—prepare questions around fees, lending flexibility, digital tools, and support.

- Meet with specialists—schedule calls or visits with bank managers to assess how well they understand real estate.

- Request fee disclosures in writing so you can compare true costs across banks.

- Test the tech—explore demo accounts or app previews to ensure the platform fits your workflow.

- Get referrals from fellow investors who’ve had positive banking experiences.

- Assess the relationship—how responsive is the bank? Do they offer real insights or just standard products?

What should you consider when looking for a financial institution? Start with compatibility. The best banking partner will understand how you operate, offer tools to save you time, and scale with your portfolio.

Key questions to ask potential banks:

Before you commit, ask these questions to make sure the bank is equipped to support your real estate business:

- “What experience do you have working with real estate investors using a [your strategy] approach?”

This helps you gauge whether the bank understands your needs, whether you're doing BRRRR, fix-and-flip, or buy-and-hold. - “What are your standard wire transfer limits and associated fees?”

Real estate deals often move quickly and involve large sums. Make sure the bank won’t delay your transactions or charge excessive fees. - “How are relationship managers assigned, and what is their typical real estate experience?”

A knowledgeable banker can make financing smoother and offer solutions tailored to your business. - “What digital tools do you offer specifically for tracking property-related expenses?”

Look for features like sub-accounts, tagging, or built-in bookkeeping to stay organized without third-party tools. - “How would you handle financing for my next investment property given my current portfolio?”

This gives you insight into their lending approach and whether they can scale with you. - “What are your procedures if I need emergency access to funds for a time-sensitive deal?”

In competitive markets, timing is everything. You need a bank that can move quickly when opportunities come up.

These questions will help you uncover whether a potential banking partner truly understands the needs of real estate investors—and whether they’re ready to grow with you.

Choose a bank that understands how real estate works

The best banks for real estate investors are built around how you run your business, not just where you store your money. Whether managing long-term rentals or short-term stays, your banking solution should help you stay organized, save on fees, and scale efficiently.

Baselane offers an all-in-one banking and financial platform designed specifically for landlords and property investors:

- No monthly fees or minimum balances

- High-yield checking account with up to [v="apyvalue"] APY²

- Unlimited virtual accounts to separate income and expenses by property

- Built-in rent collection via ACH, credit card, or debit (with auto-pay and reminders)

- Bookkeeping with transaction tagging and Schedule E categories

- Real-time cash flow analytics and custom reporting

- Integrated landlord tools: tenant screening and insurance

- Access to financing with investor-friendly loans and portfolio lending options

Whether you’re searching for the best bank account for rental property or the best bank for an Airbnb business, Baselane delivers modern banking with the tools you need. Sign up for a free Baselane account today!

FAQs

Do I need a separate bank account for each rental property?

You’re not required to, but using separate accounts or virtual sub-accounts can make tracking income, expenses, and taxes much simpler. If you’re managing multiple properties, opening a business bank account for landlords or setting up property-specific sub-accounts helps you stay organized and tax-ready year-round.

How important is a bank's experience with real estate investors?

It makes a big difference. Banks that specialize in real estate investing often provide tools like help on opening an escrow account, rent tracking, and landlord-specific loan products. These features can save you time and reduce headaches compared to working with a general-purpose business bank.

Should I prioritize physical branch locations or digital capabilities?

That depends on how you operate. If you need to deposit cash or prefer in-person service, branch access is helpful. But if you value automation and flexibility, digital-first banking with features like high-yield online savings accounts and integrated rent collection is often the smarter move. Especially for remote or out-of-state investing.

What's more important: the relationship with my banker or the products offered?

Both matter, but the right tools often outweigh the relationship, especially when you're starting. Look for banks with real estate–friendly features like fee-free accounts, rent automation, and strong APYs. As you grow, having a banker who understands your business and can support financing needs becomes more important.

How often should I reevaluate my banking relationship?

At least once a year, or anytime your portfolio or strategy changes. If your current setup lacks flexibility or charges too many fees, it may be time to upgrade to a more scalable platform. Revisiting your setup also helps if you’re deciding between a business vs personal bank account or looking to open a high-yield savings account to boost your returns.