When you’re managing rental income, security deposits, and CapEx reserves across multiple properties and entities, idle cash sitting in a low-yield account represents a real cost to your portfolio. A high-yield savings account (HYSA) puts those funds to work, earning a competitive Annual Percentage Yield (APY) while keeping reserves organized and accessible.

This guide covers how to get a high-yield savings account, what to consider when choosing one, and how to structure your HYSA account strategy to align with how you actually operate.

Key takeaways

- High-yield savings accounts offer higher APY than traditional savings accounts, turning idle reserves and deposits into a portfolio-wide income source.

- Online banking platforms typically offer no monthly account fees, no minimum balances, and digital tools built for multi-entity management.

- HYSAs can hold operating reserves, emergency funds, and security deposits.

- Baselane’s HYSA offers up to [v="apyvalue"] APY² with unlimited virtual accounts, so you can organize savings by property, reserve type, or LLC under one login.

How does high-yield savings work?

A HYSA operates like a standard savings account but offers a significantly higher APY. The higher rate is possible because online banking platforms have lower overhead costs than traditional branch-based institutions.

Your deposits earn compound interest, typically calculated daily and credited monthly. The APY reflects the total amount of interest earned over a year, accounting for compounding. This means security deposits, operating reserves, and CapEx funds can all generate returns while remaining liquid and accessible.

Unlike investment accounts, HYSA savings accounts carry no market risk. Your principal is protected, and deposits at FDIC-member institutions are insured. This makes HYSAs a practical choice for funds you need to access on a predictable schedule — such as property tax payments, insurance premiums, or planned capital expenditures.

How to open a high-yield savings account: Step-by-step guide

If you’re wondering how to start a high-yield savings account for your real estate portfolio, the process is more straightforward than setting up a traditional business banking relationship. Consumer prices in 2025 remain 23% higher than pre-pandemic levels, which means keeping rental funds in a low-interest account erodes your purchasing power over time. High-yield savings account rates can outpace inflation, helping preserve the value of your reserves and deposits.

Below is a step-by-step breakdown of the requirements for a high-yield savings account, how to evaluate providers, and how to fund and structure your accounts for multi-property operations.

Before we jump into the steps, let’s see the key documents you need to open your account.

Step 1: Compare high-yield savings accounts

Not all annual percentage yield savings accounts are the same, so it pays to shop around, especially when you’re managing funds across properties. Here’s what to look for:

- High APY: Target at least 2.5% or higher to generate meaningful returns on reserves and deposits across your portfolio.

- No monthly account fees: Avoid accounts that charge $5 to $15 per month per account — those fees compound when you’re running multiple entities.

- No or low minimum balance: Choose accounts that don’t penalize you for moving funds between accounts as needed.

- Digital account management: Look for platforms that support sub-accounts, property-level labeling, and automated transfers between checking and savings.

- FDIC insurance: Confirm deposits are protected up to $250,000 per depositor, per institution.

Where to open a high-yield savings account

Both online and traditional banks offer HYSAs, but digital real estate platforms typically provide high-yield savings accounts with no minimum balance and higher APYs. Lower operational overhead allows them to offer more competitive rates.

Instead of looking for banks with high APY, it’s best to go with fintech platforms that offer much more competitive APY. When choosing where to open a high-yield savings account, the best bank account for rental property owners combines a competitive APY with the account structure needed to manage multiple properties and entities. Step 2: Check the provider’s terms and conditions

Before opening a HYSA bank account, take a few minutes to review the fine print. Here’s what to look for:

- Withdrawal limits: Some banking platforms still limit savings account transfers to six per month, though this is no longer a federal requirement.

- APY requirements: To earn the advertised rate, you may need to meet certain conditions, like maintaining a minimum balance or setting up direct deposit. Confirm whether the APY applies to all balances or only up to a certain threshold.

- Deposit methods: Make sure the provider supports ACH transfers, mobile check deposits, or wire transfers for easy funding.

- Account limits: Determine whether you can open multiple savings accounts under one login, or if each entity requires a separate application and login.

Understanding these details upfront prevents operational friction, especially when comparing digital banking benefits across providers.

For provider comparisons, see our lists of the best banks for real estate investors and the best banks for Airbnb business owners.

Step 3: Gather required information

Most providers require standard documentation to verify identity and, for business accounts, entity details. Here are the typical requirements for a high-yield savings account:

For individual accounts:

- Name, address, date of birth, and Social Security number

- Government-issued photo ID (driver’s license or passport)

- Link the external bank account for initial funding

For LLC or business entity accounts:

- EIN (Employer Identification Number)

- Business formation documents (certificate of incorporation or organization)

- Operating agreement (if applicable)

Most banks offer only one savings account and free business checking accounts per entity, which creates friction when you’re managing separate reserves for each property or LLC. You’ll either need to pay for additional operating reserve accounts (if that’s an option) or open separate accounts under different logins.

Baselane’s banking platform lets you open unlimited checking and high-yield savings accounts for multiple entities under one login. Organize operating reserve accounts and separate deposits, reserves, and emergency funds in savings accounts that earn up to [v="apyvalue"] APY².

Step 4: Open and fund your account

Once you’ve selected a provider, you can open a high-yield savings account online in most cases. With Baselane, there is no minimum deposit or balance requirement, and no monthly account fees.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

How to open a high-yield savings account with Baselane

- Sign up for a free Baselane account: Head to baselane.com and click “Get Started.” Create a secure login using your email.

- Click “Add Account”: Choose whether you’re opening an account as a Sole Proprietor or under a business entity (LLC, partnership, etc.). Baselane supports both individual and business banking setups.

- Complete the application: Provide your personal or business information, including your name, address, SSN or EIN, and upload a valid photo ID.

Get approved and start banking: Once you're in, you can open unlimited checking and savings accounts, perfect for organizing funds by property or purpose.

How to fund your HYSA

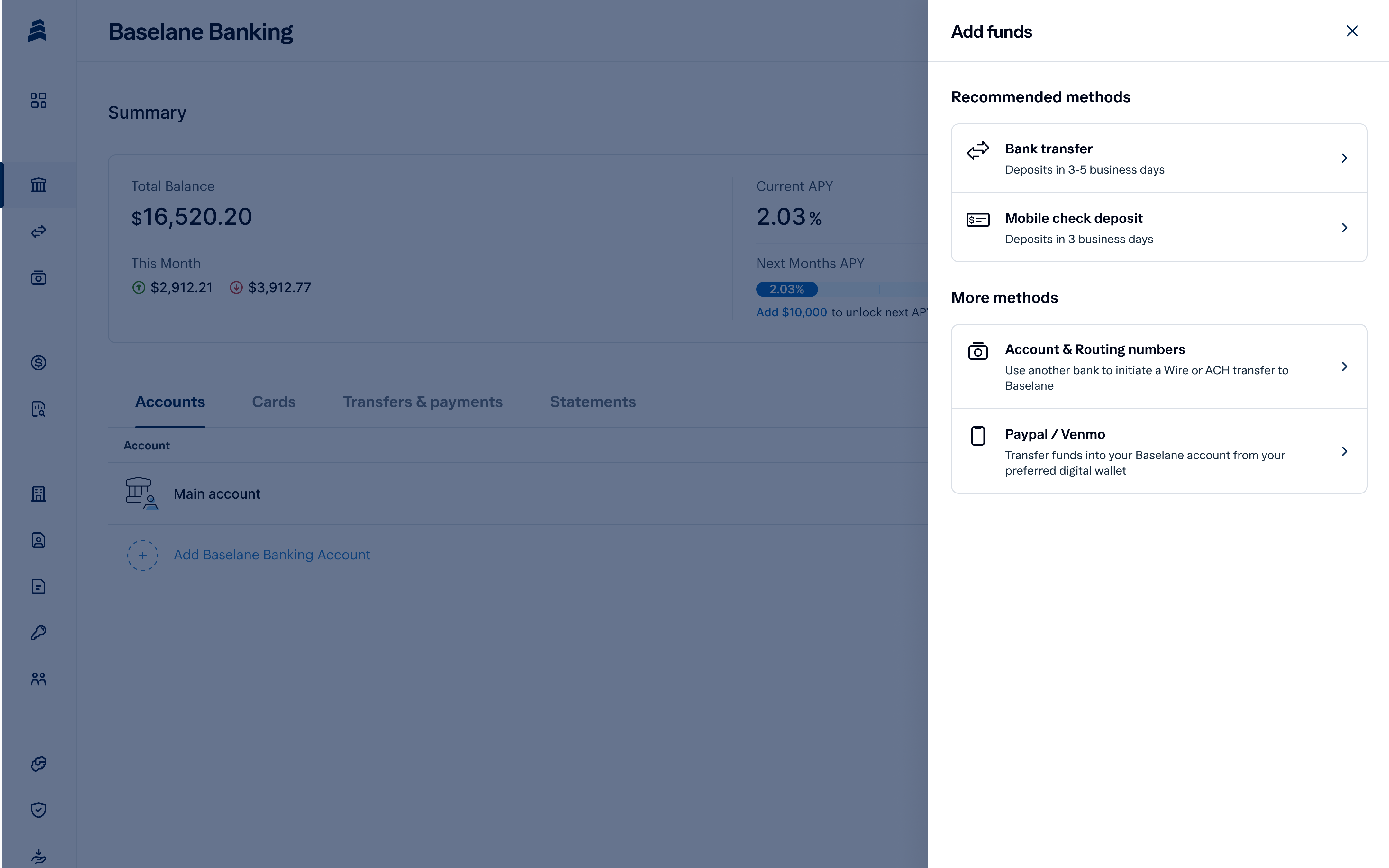

You can fund your new account using any of the following methods:

- Bank transfer: Link an external HOA bank account or digital wallet and initiate a transfer.

- Wire transfer: Receive funds via wire from another bank.

- Cash deposit: Use any in-network ATM (55,000+ Allpoint ATMs) to deposit cash.

- Check deposit: Log in from a mobile device and take a photo of the check.

Funds will be deposited into your checking account, which you can instantly transfer to your savings.

There’s no definite answer to how much to put in high yield savings account. As a rule of thumb, you should aim to cover your down payment (5% to 20% of the home price), closing costs (typically 1.5% to 4% of the purchase price), and a 3-to-6 month emergency fund for future expenses.

Set up automatic transfers

Automatic transfers help maximize returns while making sure money is in the right reserve bank accounts before bills come out. Here’s how to set up one-time or recurring transfers between your Baselane accounts:

- Log in to your Baselane account: From the dashboard, click “Move Money” then select “Transfer Funds.”

- Choose your source and destination: Select the Baselane account you want to transfer from, and the savings account you want to transfer to. You can easily label each account by property or purpose (e.g., “Security Deposit Savings – Unit 2B”).

- Set the amount and schedule: Enter the transfer amount and choose whether it should happen once or on a recurring schedule (weekly, monthly, etc.).

- Add property tags (optional): Tag your transfer to a specific property or expense type to keep bookkeeping organized for tax preparation.

Best ways to use a high-yield savings account

A high-yield savings account is a strategic solution for organizing and growing reserves across your portfolio. Here are the most effective applications for real estate investors:

- Store security deposits: Keep tenant deposits in separate, interest-earning accounts while staying compliant with state deposit regulations.

- Build emergency reserves: Set aside cash for unexpected repairs, vacancies, or seasonal expenses with escrow reserve accounts that remain isolated from operating funds.

- Save for CapEx projects: Prepare in advance for roof replacements, HVAC upgrades, or full renovations with property-specific savings accounts. Use our free property evaluation spreadsheet to find the best property for capital improvements.

- Hold funds for acquisitions: Let your down payment reserves grow while you evaluate your next investment.

- Separate reserves by property: Track expenses and reserves per property by opening multiple reserve accounts. Baselane supports you in setting up multiple banking accounts for this purpose.

- Create a renovation fund: Dedicate an account to planned improvements so capital is available when it’s time to invest in upgrades.

- Earn yield on idle funds: Whether it’s money reserved for taxes, insurance, or future investments, let your cash earn while it waits.

Earn up to [v="apyvalue"] APY² on Baselane high-yield savings accounts

Baselane’s HYSA is built specifically for real estate investors, with the account structure and automation needed to manage a growing portfolio

Here’s what makes Baselane’s HYSA stand out:

- Earn up to [v="apyvalue"] APY²: Grow your cash at rates significantly above the national average for savings accounts.

- No minimum balance or monthly fees: Keep more of your money working for you without worrying about monthly charges or balance thresholds.

- Unlimited virtual accounts: Organize funds by property, reserve type, or business entity under one login.

- Integrated bookkeeping and real-time insights: Every deposit, transfer, and withdrawal is automatically tracked and categorized.

- Built-in real estate tools: Integrated with rent collection and tenant screening, so your banking, income tracking, and operations work together.

With Baselane, your savings work harder and smarter without extra software or hidden fees. Ready to earn more on your cash? Get started today

FAQs

Where can I open a high-yield savings account?

High-yield savings accounts are available at online banks, credit unions, and some traditional banks. Online banks often offer higher APYs, while credit unions and brick-and-mortar banks may offer additional in-person support.

What are the requirements for a high-yield savings account?

Most banks require a government-issued ID, Social Security Number (SSN) or Employer Identification Number (EIN), and an existing bank account to fund the new HYSA. You’ll also need formation documents and an operating agreement if applying as a business.

How do you open a high-yield savings account?

You can open a high-yield savings account online or at a branch through traditional banks and credit unions. With Baselane, you can quickly open a high-yield savings account online without any minimum deposit or balance requirements and no monthly fees. If you’re using HYSAs for security deposit management, check your state laws for escrow requirements to ensure you’re staying compliant. Here’s a guide on how to open an escrow account for security deposits.

Can investors use a high-yield savings account for rent or deposits?

Yes, you can use HYSAs to hold reserves, rent income, or security deposits, depending on state laws. Baselane lets you open unlimited checking and savings accounts for multiple entities under a single login, making it easy to separate funds and stay organized.

Are high-yield savings accounts FDIC-insured?

Most high-yield savings accounts are FDIC-insured up to $250,000 per depositor, per bank. That means your money is protected while it earns more interest than a traditional savings account. Baselane is FDIC-insured for up to [v="fdic_short"]¹ on funds deposited via Thread Bank, Member FDIC.

What’s the difference between a high-yield and a traditional savings account?

A high-yield savings account offers a much higher interest rate than traditional savings accounts. HYSAs are most commonly offered through online banks, but you can find them at some traditional banks and credit unions, often with lower rates and higher fees.

Do high-yield savings accounts have withdrawal limits?

Some banks still cap savings withdrawals at six per month, but this is no longer a federal rule. The Federal Reserve removed the limit in 2020, though individual banks may still enforce it. Always check your bank’s terms before transferring funds to avoid bank fees or restrictions.

How do you fund a high-yield savings account?

Most high-yield savings accounts are funded through ACH transfers from an external bank account. Some banks also allow wire transfers or mobile check deposits. ACH transfers are the most common but may take a few business days.

How much money should you put in a high-yield savings account?

You can open a high-yield savings account with any amount allowed by the bank. Many people start with a small deposit and gradually add funds. HYSAs are commonly used for emergency savings or short-term cash reserves.