If managing rental income feels harder every year—especially at tax time—it’s usually not because you’re earning more. It’s because your money isn’t organized in a way that matches how real estate actually works.

When rent, repairs, reserves, and personal spending all flow through the same account, it becomes impossible to answer basic questions like:

- How much did this property really make?

- How much can I safely reinvest?

- Am I putting myself at legal or tax risk?

Separating and organizing your bank accounts isn’t about adding complexity. It’s about creating clarity, reducing risk, and giving you control as your portfolio grows.

Key takeaways

- Keeping personal, operating, and reserve accounts separate protects you legally and simplifies tax reporting.

- Organized accounts make it easy to see which properties are profitable and how much cash is available for reinvestment.

- Each bank account should have a key focus—operating, reserve, or personal—to reduce errors and confusion.

- One property may only need a single operating account, while multiple properties benefit from property-level or reserve accounts.

- Baselane helps you can easily track, categorize, and report on your finances at the property level.

- Quarterly reviews of balances, automated transfers, and sub-account allocations keep your system effective and up to date.

Why separating your rental finances matters

Most landlords don’t set out to mix rental and personal money—it usually happens out of convenience. You collect rent in the same account you already have, pay a few expenses from there, and tell yourself you’ll sort it out later. That approach works early on, but it breaks down fast as soon as you add another property, form an LLC, or hit your first serious tax season.

Separating your rental finances matters because it directly affects how much risk you carry, how clearly you understand your numbers, and how easy it is to operate going forward.

Here’s what clean financial separation actually gives you:

- Cleaner, faster tax preparation: When rental income and expenses live in separate bank accounts, transactions are easier to categorize, deductions are easier to defend, and tax prep becomes a routine process instead of a stressful cleanup job.

- Stronger legal boundaries: If you’re operating through an LLC, mixing personal and rental funds weakens the separation between you and the business. Dedicated accounts show that the rental activity is its own entity, which is precisely what matters if a court ever questions liability protection.

- Clear visibility into property performance: Separate accounts—or at least clear separation by property—lets you see which rentals are generating real cash flow and which ones are quietly struggling.

- Better cash flow awareness: When money is separated, you can see what’s truly available after expenses, reserves, and obligations, so your investment decisions are based on reality, not assumptions.

- Fewer bookkeeping mistakes as you scale: Systems that rely on manual notes, labels, or memory tend to fail as portfolios grow. Dedicated accounts create a structure that holds up whether you own one property or ten.

- Simpler, more intentional owner payments: Clear separation makes it easier to distinguish between reimbursing yourself, taking income, and distributing profit.

How many bank accounts do you actually need?

There’s no universal rule that says you must open a certain number of bank accounts to “do it right.” What matters is that each account has a clear purpose and that your setup doesn’t rely on constant manual work to stay organized.

The number of accounts you need depends on how many properties you own, how they’re held, and how much visibility you want.

If you own a single rental property, one dedicated rental operating account is usually enough—as long as it’s completely separate from your personal finances. This is the account where you collect rent and pay for day-to-day property expenses.

If you own multiple properties under the same ownership, you generally have two workable options:

- Separate operating accounts per property: Each property has its own operating account. This gives you the clearest picture of income, expenses, and cash flow.

- One operating account with strong property-level tracking: All rent and expenses flow through a single rental operating account, but transactions are clearly separated by property. This approach reduces the number of accounts while still maintaining visibility—as long as the tracking is reliable and consistent.

If you operate through an LLC, a business operating account isn’t optional. All rental income and expenses should flow through that account, not your personal one. This helps maintain the legal separation between you and the business and avoids commingling funds.

As your portfolio grows, many investors also add a savings or reserve account. This account is used specifically to hold money for repairs, vacancies, and larger capital expenses. Keeping reserves separate from operating cash reduces the risk of overspending and makes it easier to plan ahead.

No matter which structure you choose, the goal is the same: a system that stays clean as you scale, without requiring more spreadsheets, more memory, or more cleanup later.

Related: Sole Proprietorship Bank Account: Requirements and Best Options for Landlords

Common bank accounts for rental properties (at a glance)

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Platforms to use to set up multiple property accounts

Most traditional banks weren’t designed for rental property finances. They treat every account the same, which forces you to do the organizing yourself. If you want to track money by property, you’re left juggling multiple accounts, exporting statements, or relying on spreadsheets to fill in the gaps. That manual work becomes harder to maintain as you add more properties.

This is where property management software makes a difference.

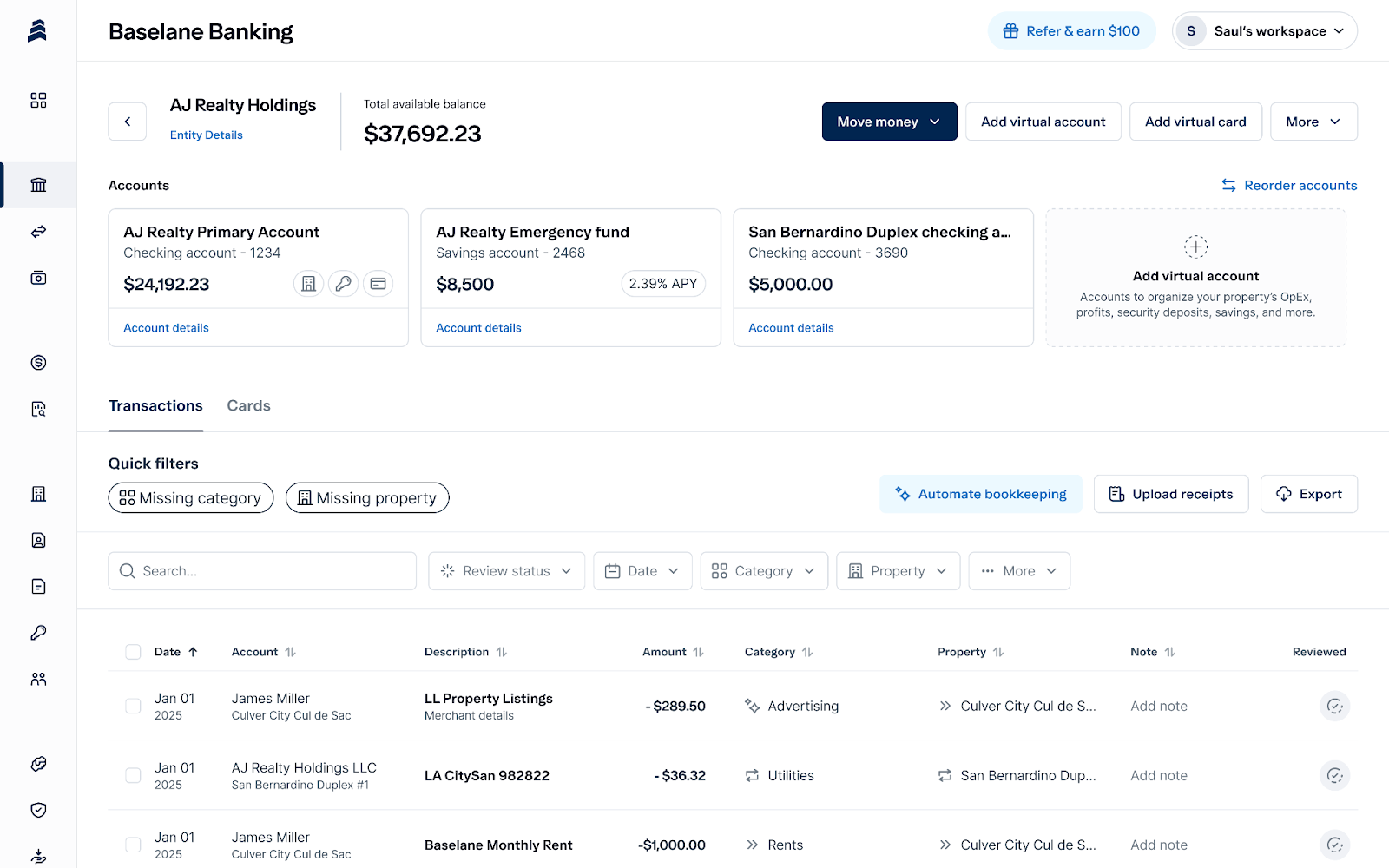

Baselane, an all-in-one banking platform, simplifies how you separate and manage money across properties by combining property-level banking with automated bookkeeping. Instead of opening and monitoring dozens of accounts across multiple banks, you centralize finances using Baselane’s unlimited checking and savings accounts.

Transactions are automatically categorized for tax reporting, and you can see cash flow and performance by property in one place. The system enforces financial separation by design, so you’re not relying on memory, labels, or after-the-fact cleanup to stay organized.

Once your portfolio grows, reviewing the best banks for real estate investors and the best multifamily property management software becomes less of a nice-to-have and more of a competitive advantage.

How to set up and organize your Baselane account

Whether you have one rental property or a growing portfolio across multiple LLCs, the goal is the same: you should know exactly what every dollar is for, without extra spreadsheets or manual juggling and Baselane’s property-level banking and accounting helps you do just that.

Step 1: Start with your primary operating account

When you create your Baselane banking profile and get approved, you get a primary Baselane checking account, aka your operating account. This is where you collect rent and pay day-to-day property expenses—like maintenance, utilities, mortgage payments, and property management fees.

- If you own just one property, one operating account is enough.

- If you own several properties under a single entity, you have two options:

- Separate operating accounts per property to manage finances at a property-level

- One operating account with property-level transaction tracking inside Baselane, which saves time and reduces account clutter.

Step 2: Add a reserve (or savings) account

Open a savings account (or even a second Checking account) as your financial safety net. Use it to stash money for:

- Repairs and maintenance

- Vacancy reserves

- Property taxes or insurance premiums

- Future capital improvements (like a roof replacement or HVAC upgrade)

Label the savings account in your Baselane dashboard—like “Property A Reserves” or “LLC Maintenance Fund.” Set up auto-transfer rules to move a percentage of your monthly rental income (e.g., 5–10%) into your savings account to maintain a minimum balance.

Step 3: Set up your security deposit account

Keep your security deposit separate and maintain clear tracking by opening a dedicated security deposit savings account.

While we don’t offer an escrow or trust account, you can still use a checking or savings account. Here’s how:

- For states that don’t require an escrow account, you can legally receive and keep deposits in one of your Baselane accounts.

- For states with escrow requirements, you can still receive funds in Baselane for clear record-keeping and then transfer them to state-based financial institutions.

Before collecting funds, make sure you understand how much security deposit a landlord can charge and how to open an escrow account for rent so you stay compliant and avoid costly mistakes.

Step 4: Use sub-accounts and tags to simplify tracking

Baselane offers unlimited sub-accounts, which act like “buckets” inside your main Baselane account.

A sub-account is a separate, named balance under your main Baselane account that you can use to receive money, hold it, and pay it out, just like a mini checking or savings account. You might name them things like “123 Main – Operating,” “Portfolio Reserves,” or “Property Taxes.”

This lets you separate money by purpose or property without opening a bunch of full standalone bank accounts at different banks. You still see one overall balance for your portfolio, but you always know how much of that money is earmarked for each bucket.

Here are a few simple ways to use sub-accounts:

One property, one bank:

- Main Baselane account = your “Rental Bank.”

- Sub-accounts: “Rent & Bills,” “Repairs & Emergencies,” “Property Taxes.”

You collect rent into “Rent & Bills,” then set up small recurring transfers into “Repairs & Emergencies” and “Property Taxes” so money is already set aside when something breaks or taxes are due.

Multiple doors, same LLC:

- Sub-accounts like “123 Main – Operating,” “456 Oak – Operating,” plus a shared “Portfolio Reserves” bucket.

Rent for each property lands in its own operating sub-account, so you can open Baselane and instantly see which property is pulling its weight and which one is tight.

Step 5: Review and adjust regularly

Set a reminder every quarter to review balances, automate transfers, and validate that each account still serves its purpose. As you acquire or sell properties, Baselane makes it easy to open or archive accounts so your structure always matches your portfolio.

Once it’s all set up, you’ll always know where your money stands, and your finances will finally look as organized as your properties.

Transition from a mixed to a clean setup with Baselane

Organizing and separating your bank accounts protects you legally, simplifies your taxes, and gives you the visibility you need to grow your rental business with confidence. The earlier you set it up, the easier everything else becomes.

And, Baselane makes this setup even easier with its integrated banking and bookkeeping. Create a checking or savings account you need, automate bookkeeping, and get real-time insights into your cash flow. Open your Baselane account today!

FAQs

Do I need a separate bank account for each property or purpose?

You don’t always need a separate bank account for each property, but you do need separation by purpose. Some people use one operating account with strong property-level tracking, while others prefer separate accounts per property for maximum clarity. The right setup depends on how many properties you own and how much visibility you want.

How do I organize multiple bank accounts for rental properties?

Keep personal finances separate from rental finances, then use a dedicated rental operating account for income and expenses. As your portfolio grows, add reserve or property-level accounts.

How do I separate money in a bank account for different purposes?

The most reliable way to separate money in a bank account is to use dedicated accounts. Use one operating account for rental activity, a reserve account for savings, and your personal account only for personal spending. This approach makes it easier to manage a bank account without confusion.

How can I organize bank statements for easier tracking?

The easiest way to organize bank statements is to use a digital banking solution like Baselane to ensure each account serves only one purpose. When rental and personal transactions aren’t mixed, statements are easier to review and categorize. Automation can further simplify how you organize bank statements by tagging transactions consistently.

What is the best way to divide money across multiple bank accounts?

The best way to divide money across multiple bank accounts is to assign each account a single job:

- Operating account for day-to-day transactions

- Reserve or savings account for future expenses

- Personal account for non-rental spending

This structure simplifies your bank account setup and reduces bookkeeping errors.

How many bank accounts should I use to stay organized?

Use the fewest accounts possible while still staying organized. Most landlords need at least one rental operating, one reserve or savings account, and one personal account. You can add more accounts as your portfolio grows, but only if they reduce complexity instead of increasing it.

How can automation help organize money in bank accounts?

Automation helps organize bank accounts by categorizing transactions automatically and grouping them by purpose or property. You spend less time managing a bank account and more time understanding your numbers. Read more about the best landlord apps to use to automate your rental finances.