As a landlord or real estate investor, understanding tax deductions is crucial for maximizing your returns. Taxes are a significant expense, directly impacting your profitability. Knowing which costs you can legally write off can help you reduce your taxable income. This guide covers the essential rental property tax write-offs for the 2025 tax year.

Key takeaways

- Many ordinary and necessary expenses related to rental property management are deductible.

- Key deductions include mortgage interest, property taxes, and depreciation.

- There is a crucial distinction between deductible repairs and depreciable improvements.

- Specific rules like the SALT cap and passive activity loss limitations affect potential deductions.

- Meticulous record-keeping is essential for claiming all eligible write-offs accurately.

Understanding Rental Property Income

Before exploring deductions, it’s important to understand what counts as taxable rental income. Rent payments from tenants are the most obvious form of income you must report. Advance payments of rent are considered taxable income in the year you receive them, regardless of when they apply.

Security deposits are generally not taxable income when you receive them if you plan to return them to the tenant. However, if you keep a security deposit, the amount kept becomes taxable income at that time. If tenant funds are used for damages, the costs may offset the income if the repairs are properly documented. Some vacation rental income taxrules may differ slightly from long-term rentals.

Tenant-paid expenses, where a tenant pays costs for you (like utilities), are also typically considered income to you. You may then be able to deduct these expenses if they qualify. Accurate tracking of all income sources is the first step in managing your rental property finances.

Essential tax write-offs for landlords

Landlords can deduct many expenses incurred from renting out property. These deductions help reduce your overall taxable income from your rental business. Understanding the major categories is key to effective tax planning.

Mortgage interest

Mortgage interest is often one of the largest deductions for rental property owners. You can deduct the interest paid on mortgages used to purchase or improve your rental property. The bank will send you Form 1098 showing the amount of interest paid during the year.

This deduction applies to loans secured by the rental property itself. If you use a personal loan for rental property purposes, the interest may still be deductible, but different reporting rules might apply. Keeping clear records of all loan payments and purposes is vital.

Property taxes

Real estate taxes levied by local authorities are deductible expenses for rental property owners. This includes taxes assessed on the value of the property itself. However, there are limitations on this deduction.

For 2025, the deduction for state and local taxes (SALT), which includes property taxes, is capped at $10,000 per household ($5,000 if married filing separately). This cap applies to the total of state and local property taxes, income taxes, or sales taxes. You can use property tax software to help track these costs.

Depreciation

Depreciation is a method to recover the cost of your rental property over time. You can deduct a portion of the property’s cost each year to account for wear and tear or obsolescence. This is a non-cash expense, but is a significant tax benefit.

Residential rental property is typically depreciated over 27.5 years. Land and the cost of your personal residence (if renting part of it) cannot be depreciated. You begin depreciating property when it is placed in service, meaning it is ready and available for use as a rental, even if it’s not yet rented. Depreciation can be complex, and proper calculation is essential. Understanding concepts like [1301 property exchange] also involves considering depreciation recapture.

Repairs vs improvements

One of the most important tax distinctions for landlords is between repairs and improvements. Repairs are expenses that keep your property in good operating condition and are generally deductible in the year you pay for them. Examples include fixing a leaky faucet, patching a hole in the wall, or repainting a room. These costs restore the property to its original condition.

Improvements, on the other hand, add value to the property, prolong its useful life, or adapt it to new uses. Examples include replacing the roof, adding a new room, installing a new HVAC system, or significantly remodeling a kitchen or bathroom.

The cost of improvements cannot be fully deducted in one year; instead, they must be depreciated over 27.5 years, similar to the property itself. Correctly classifying these costs is crucial for accurate tax reporting.

Other common deductible expenses

Beyond the major write-offs, numerous other operating expenses can be deducted. These costs are incurred regularly in the process of managing your rental property. Keeping detailed records for these smaller expenses is just as important as for the larger ones.

Operating expenses

Many day-to-day costs associated with running a rental property are deductible. These include utilities you pay for (if not the tenant’s responsibility), like electricity, gas, and water. Insurance premiums for landlord insurance, fire insurance, and even flood insurance (if applicable) are also deductible. The costs of advertising your rental property to find tenants are fully deductible. Supplies used for cleaning or minor maintenance are also included here.

Professional and Management Fees

Fees paid for professional services related to your rental business are deductible. This includes fees paid to accountants for tax preparation or bookkeeping advice. Legal fees for services such as drafting leases or handling eviction proceedings are also deductible. However, legal fees paid to defend your title to the property are generally not deductible and must be added to the property’s basis. If you hire a property management company, their fees are fully deductible business expenses. Landlords managing short-term rentals might consider charging a management fee for short-term rentals for clarity, but this is generally not a deductible expense, as you cannot deduct payments to yourself.

Travel and Vehicle Expenses

Travel expenses incurred for operating and maintaining your rental property are deductible. This includes trips to collect rent, perform repairs, or manage the property. You can deduct either the actual expenses of using your car (gas, oil, repairs, depreciation/lease payments) or use the standard mileage rate. For 2025, the standard mileage rate for business use is $0.70 per mile.

Commuting costs between your home and the rental property are generally not deductible. An exception applies if your home is considered your principal place of business for the rental activity. This typically requires meeting specific criteria related to the use of a dedicated home office space.

Legal Fees

As mentioned, legal fees directly related to your rental business operations are usually deductible. This covers costs associated with lease agreements, tenant issues, or property-related disputes.

However, the nature of the legal service dictates deductibility. Costs related to acquiring the property or defending ownership are usually capitalized, not deducted immediately.

Home Office Deduction

If you use a portion of your home exclusively and regularly as your principal place of business for your rental activity, you may be able to claim the home office deduction. Your home must be the main location where you conduct your rental business, such as managing properties, bookkeeping, and communicating with tenants. Meeting the strict IRS criteria for this deduction is essential. Using the home office for personal activities disqualifies the space.

Casualty Losses

Losses from a federally declared disaster area may be deductible (IRS.gov). If your rental property sustains damage or is destroyed due to a sudden, unexpected, or unusual event like a hurricane, fire, or flood, you may be able to deduct the loss not covered by insurance . Theft losses may also be deductible. Calculating the deductible amount involves determining the decrease in the property’s value or the adjusted basis, whichever is less, reduced by any insurance reimbursements.

Wages Paid

If you employ someone to manage or maintain your rental property, the wages paid to that employee are deductible. This could be for a property manager, maintenance worker, or administrative assistant. Payments to independent contractors for services like cleaning or repairs are also deductible business expenses. Be sure to understand the distinction between employees and independent contractors for tax reporting purposes.

Key tax rules and limitations for 2025

Understanding specific tax rules and limitations is crucial for accurately calculating your deductions for the 2025 tax year. These rules can impact how much of your rental property losses you can deduct in a given year. Proper classification and reporting are essential.

Passive activity loss rules

Rental activities are generally considered passive activities by the IRS. Losses from passive activities can typically only be offset by passive income. However, there are exceptions that may allow you to deduct up to $25,000 of passive losses against non-passive income (like wages or investment income).

This exception applies if you “actively participate” in the rental activity (Investopedia, TurboTax). Active participation means you make management decisions, such as approving tenants, deciding on rental terms, or approving repairs, and own at least 10% of the property.

The ability to deduct up to $25,000 in losses phases out as your Modified Adjusted Gross Income (MAGI) rises above $100,000, becoming fully phased out at $150,000 MAGI. If you do not actively participate or your MAGI is too high, losses are carried forward to future years or deducted when you sell the property. There is also a “real estate professional” exception, which allows unlimited passive loss deductions, but the requirements are stringent.

State and Local Tax (SALT) Cap

As noted earlier, the deduction for state and local taxes (SALT) is limited. For 2025, the maximum deduction for property taxes, state income taxes, or state sales taxes combined is $10,000 per household ($5,000 if married filing separately). This cap can significantly impact the tax benefit of owning rental properties in high-tax states.

While property taxes themselves might exceed $10,000, you can only deduct up to the cap amount for federal tax purposes when combined with other state and local taxes.

Qualified Business Income (QBI) Deduction

Rental real estate activities may qualify for the Qualified Business Income (QBI) deduction, also known as the Section 199A deduction. This deduction allows eligible taxpayers to deduct up to 20% of their qualified business income from a qualified trade or business. The criteria for a rental activity to be considered a “trade or business” for QBI purposes can be complex and depend on the level of rental activity. Material participation standards may apply.

What you can't deduct

Just as important as knowing what you can deduct is understanding what you cannot. Incorrectly claiming non-deductible expenses can lead to issues with the IRS. Avoiding these common errors is essential for accurate tax filing.

Personal expenses related to your home or lifestyle are generally not deductible. The cost of improvements to your rental property is not deductible in the year incurred; instead, it must be depreciated over its useful life. Commuting costs between your home and the rental property are typically not deductible unless your home qualifies as your principal place of business for the rental activity. Local benefit taxes assessed for improvements like streets or sidewalks are also not deductible. Fines or penalties paid to governmental entities are also non-deductible.

Importance of meticulous record-keeping

Accurate and organized record-keeping is the cornerstone of maximizing your rental property tax deductions. The IRS requires landlords to keep records to support income and expenses reported on their tax return. Poor record-keeping is a common reason for missed deductions or issues during an audit.

You should keep records for all income received and all expenses paid, including receipts, invoices, and canceled checks. Documents related to the property’s purchase, including the closing statement and records of any improvements, should also be retained (IRS.gov). Organized records simplify tax preparation and ensure you claim all eligible write-offs.

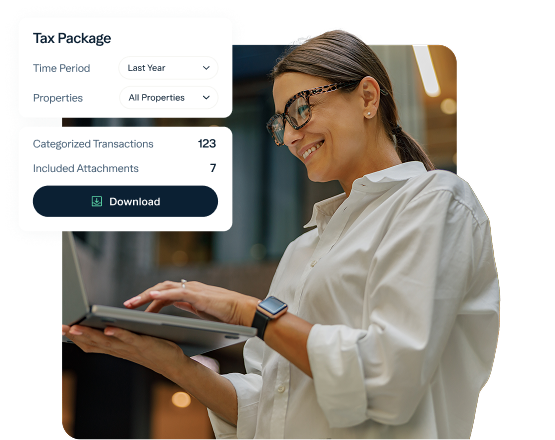

Using dedicated tools can significantly streamline this process. Rental property accounting software can automatically categorize transactions and generate reports like Schedule E.

Platforms like Baselane are designed to handle bookkeeping and standard rental property expenses, integrating banking and bookkeeping to simplify tracking income and expenses by property, making it easier to generate tax-ready reports.

Baselane’s features also help with tracking items like security deposit accounting and expenses related to security deposit deductions, linking costs directly to income.

How to report rental income and expenses

Rental income and expenses are typically reported on Schedule E, Supplemental Income and Loss, Form 1040. Schedule E is used to report income and losses from rental real estate, royalties, partnerships, S corporations, estates, trusts, and REMICs. You will list each rental property separately on this form.

On Schedule E, you will report your gross rents received and list the various deductible expenses. The form calculates your net income or loss from the rental activity. If you have multiple properties, the totals from each property are combined. Other forms might be required depending on your specific situation, such as Form 4562 for Depreciation and Amortization.

Tips for maximizing your rental property tax savings

Beyond claiming the obvious deductions, several strategies can help you further minimize your rental property tax liability. Being proactive and organized throughout the year makes tax time much smoother and potentially more beneficial.

Ensure you have meticulous records of all income and expenses, categorized appropriately. Understand the difference between repairs and improvements to ensure correct deduction or depreciation. Take advantage of depreciation rules, including bonus depreciation or Section 179 deduction if applicable (check 2025 rules). Explore strategies like a 1031 exchange if you plan to sell and reinvest in another property to defer capital gains taxes. Maximizing deductions requires diligence throughout the year. Implementing the right systems can result in no taxes on rental income in some cases.

Bottomline

Navigating rental property taxes requires careful attention to detail and a thorough understanding of deductible expenses. By claiming all eligible write-offs, from major items like mortgage interest and depreciation to smaller operating costs, you can significantly reduce your taxable income. Proper classification of expenses, particularly distinguishing between repairs and improvements, is critical.

Understanding complex rules like passive activity limitations and the SALT cap is also essential for accurate reporting in the 2025 tax year. The foundation of successful tax management for landlords is meticulous record-keeping. Tools that integrate banking and bookkeeping can automate much of this process, saving you time and ensuring accuracy.

While this guide covers key areas, consulting with a qualified tax professional is always recommended to address your specific situation and maximize your savings. A platform like Baselane can provide the necessary financial visibility and organized records to make working with your tax professional much easier.

FAQs

A deductible rental property expense must be ordinary and necessary for managing, conserving, or maintaining your rental property. Examples include mortgage interest, property taxes, operating expenses like utilities, insurance, repairs, and professional fees.

Depreciation allows landlords to recover the cost of their rental property over its useful life, which is typically 27.5 years for residential properties. You deduct a portion of the property's cost (excluding land) each year as a non-cash expense.

A repair keeps the property in good condition and is deductible in the year paid, such as patching a wall. An improvement adds value or extends the property's life and must be depreciated over 27.5 years, such as replacing the roof.

Yes, you can deduct rental property losses, but they are generally considered passive losses. If you actively participate in the rental activity and meet income limits, you may be able to deduct up to $25,000 of passive losses against other income.

Landlords typically report their rental income and expenses on Schedule E, Supplemental Income and Loss, Form 1040. This form is used to calculate the net income or loss from your rental activity.