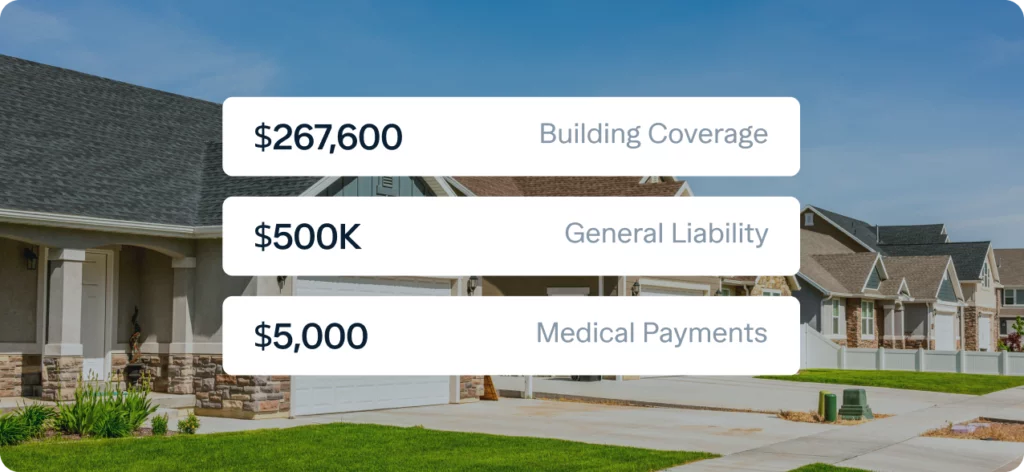

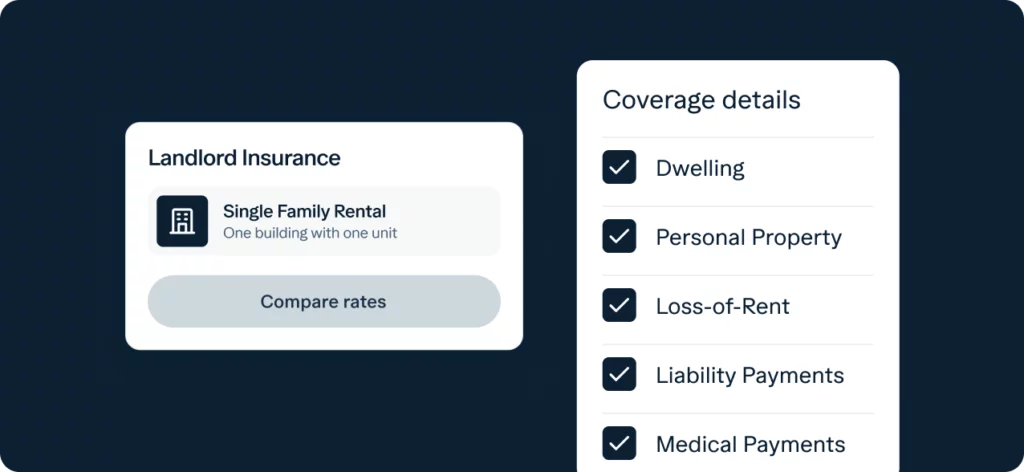

| Landlord Insurance | Homeowners Insurance | |

|---|---|---|

| Dwelling | ||

| Personal Property | Optional | |

| Loss-of-Use | ||

| Loss-of-Rent | ||

| Liability Payments | ||

| Medical Payments |

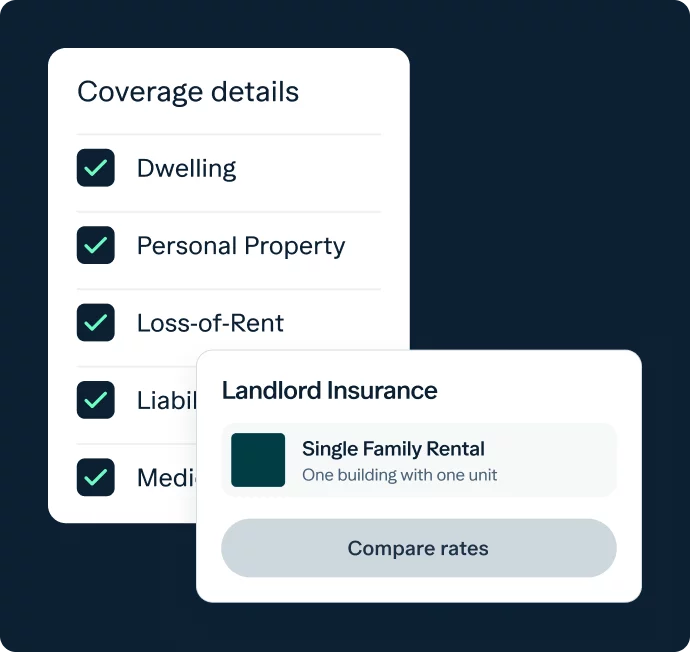

| Landlord Insurance | Homeowners Insurance | |

|---|---|---|

| Dwelling | ||

| Personal Property | Optional | |

| Loss-of-Use | ||

| Loss-of-Rent | ||

| Liability Payments | ||

| Medical Payments |