Multi-unit property owners face operational costs that don't follow predictable schedules. A strategic cash reserve account positions you to handle emergency repairs, extended vacancies, and capital replacements without disrupting portfolio cash flow. This guide covers reserve sizing methods used by experienced investors, account structure strategies for properties held across multiple entities, and how to build reserves systematically.

Key takeaways

- Reserve sizing methods include per-property minimums ($5,000), expense-based calculations (3-6 months), and rent-based models (10-30% of gross).

- Use dedicated sub-accounts to separate operating funds from capital reserves by property or LLC.

- High-yield accounts with no withdrawal penalties and strong APY provide both liquidity and growth for long-term reserves.

- Automated funding rules (percentage-based or fixed transfers) build reserves consistently without manual intervention.

- Property-level account separation supports clean financial reporting and protects reserves during entity-specific events.

What is a cash reserve account for rental properties?

A cash reserve account is a dedicated, liquid account used to fund rental emergencies and planned capital expenditures. Unlike general savings accounts, cash reserves are earmarked for specific property-related uses: emergency repairs, vacancy coverage, major system replacements, or lender-required liquidity.

For multi-unit investors, cash reserves function as portfolio-level risk management. Proper reserves prevent you from tapping personal funds, taking high-interest debt, or selling assets during market downturns to cover property expenses.

How does a cash reserve work for property owners?

Cash reserve accounts work like most bank accounts. You deposit money regularly or as needed, building up a balance intended only for specific property-related uses. These funds are kept separate from your personal or even your property's operating cash flow reserve.

Why do property owners need a dedicated cash reserve?

Managing rental properties comes with unpredictable costs and fluctuating income. That’s why maintaining an investment property cash reserve, including a cash reserve for mortgage payments, is essential for long-term financial stability.

- Stability and peace of mind: An investment property cash reserve ensures you can cover expenses without tapping personal savings or relying on high-interest debt.

- Emergency repairs: Serves as an emergency fund for rental property to protect your asset and keep tenants satisfied.

- Maintenance reserve: Acts as a reserve for rental property repairs, vital for unexpected issues such as a broken furnace or a roof leak.

- Vacancy coverage: Investment property reserves help cover mortgage, taxes, and insurance during tenant turnover.

- Capital improvements: Functions as a replacement reserve real estate fund for planned expenses like HVAC replacements or renovations.

- Lender requirements: Some lenders require an investment property cash reserve to ensure you can manage expenses during slow periods. Lenders want assurance that you can cover costs, even during lean times, to protect their investment.

How much cash reserve should you keep for each rental property?

If you’re wondering, ‘how much cash reserve should I have?’, there is no single cash reserve amount that works for every landlord or rental property. The right reserve balance depends on factors such as property age, vacancy risk, repair frequency, and how quickly you can access funds when expenses arise.

Instead of relying on a single rigid rule, most property owners choose a reserve strategy based on their risk tolerance and portfolio complexity. Below are the most commonly used reserve benchmarks for rental properties.

Common cash reserve targets for rental properties

Use one of the following reserve approaches as a baseline, then adjust upward or downward based on their situation:

- Starter reserve: Around $5,000 per rental property

- Moderate reserve: Approximately 3 months of rent or fixed expenses per unit

- Conservative reserve: Approximately 6 months of rent or fixed expenses per unit

- Property manager reserve fund: About 1 month's rent held per property

Each approach serves a different risk profile and property type.

Method 1: $5,000 per property baseline

A flat dollar reserve per property is often used by new owners with smaller portfolios. This approach works best when properties are newer or recently renovated, maintenance costs are predictable, vacancy rates are low, and the landlord has quick access to additional liquidity if needed.

While straightforward, this method may not fully cover extended vacancies or major capital repairs in older properties. Multi-unit investors typically use this as a minimum floor, not a ceiling.

Method 2: 3 to 6 months of expenses

Holding three to six months of fixed expenses is one of the most widely recommended reserve strategies for rental properties. Fixed expenses typically include mortgage payments, property taxes, insurance, HOA fees, owner-paid utilities, and recurring service contracts.

This method scales naturally with property costs and provides stronger protection during vacancies or economic downturns. A three-month reserve may be sufficient for newer, stable properties, while six months is more appropriate for older buildings or higher-risk markets.

Method 3: Rent-based reserves (10-30% of gross rent)

Some property owners base reserves on rental income instead of expenses, using rent as a simplified benchmark. This approach is often used when expenses fluctuate month to month, multiple properties are managed together, or the landlord prefers an income-based rule.

Conservative investors allocate 15-30% of gross rent each month toward reserves with no upper limit. Rent-based reserves are easier to communicate and automate, but they may be less precise for properties with unusually high fixed costs.

Method 4: Property management reserve funds

When working with a property manager, owners are often required to maintain a property management reserve fund. In many cases, this reserve is equal to approximately one month's rent per property and is used to pay vendors quickly, cover emergency repairs, and avoid delays waiting for owner approval.

These reserves are typically replenished after expenses occur and are separate from operating cash flow. Understanding investment property reserve requirements helps you meet both lender expectations and property manager operating standards.

3 most common types of cash reserves you should plan for

Not all reserves serve the same purpose. Separating reserve types helps avoid using emergency funds for routine expenses.

- Operating reserve: Covers short-term cash flow gaps such as vacancies or delayed rent payments. An operating reserve bank account for rentals acts as your vacancy and repair buffer, kept liquid and separate from capital expenditure funds.

- Maintenance reserve for rental property: Funds routine repairs and recurring maintenance items. A maintenance reserve for rental property is typically funded monthly to cover predictable repairs and appliance replacement cycles.

- Replacement or capital reserve: Set aside for large, infrequent expenses such as roofs, HVAC systems, or major renovations. This replacement reserve real estate fund protects against sudden capital needs that could otherwise destabilize portfolio cash flow.

Keeping these reserves conceptually separate improves budgeting accuracy and reduces financial stress.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

How to fund cash reserves consistently

Rather than relying on leftover cash, build reserves gradually through automatic cash reserve payment systems. A common approach is to set aside a fixed percentage of rental income each month, transfer funds into a dedicated reserve account, and pause contributions once the target reserve level is reached.

This method creates consistency and prevents reserve funding from being skipped during busy or expensive months. Set an automatic cash reserve payment to move a fixed percentage of rent into your reserve sub-account each month.

Essential features to look for in platforms offering cash reserve accounts

- Accessibility and liquidity: Funds must be available instantly for urgent repairs or vacancies. An emergency cash reserve should have no withdrawal penalties and support same-day or next-day transfers.

- Competitive yield: A high cash reserve interest rate helps reserves grow while staying liquid. Look for a high-yield savings account or business cash reserve accounts with APYs significantly above the national average.

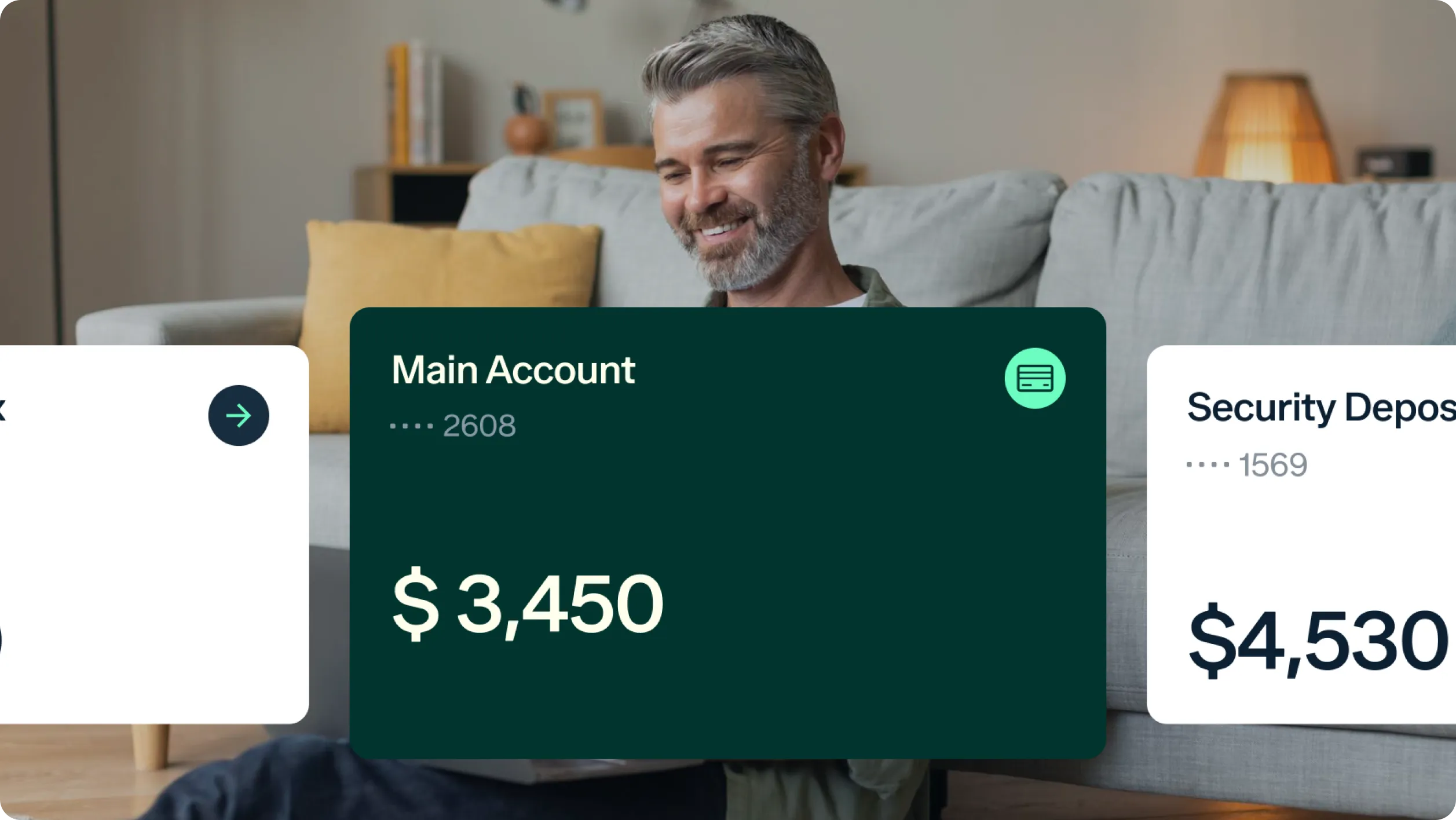

- Property-level organization: Multi-unit investors need a clear separation between properties and entities. Sub-accounts allow you to track reserves per property, per LLC, or by reserve type (operating vs. capital).

- Integrated tools: Landlord-specific platforms often combine reserve accounts with rent collection, bookkeeping, and cash reserve online banking, all in one place.

- No unnecessary fees: No-fee bank accounts help maximize available reserve funds. Fee structures that charge per account create friction when managing multiple properties.

- FDIC insurance coverage: Standard FDIC insurance covers up to $250,000 per depositor, per institution. Banking platforms partnering with multiple institutions can provide extended coverage for larger portfolios.

Best cash reserve accounts and platforms for real estate investors

Choosing the best cash reserve account depends on how you manage your rental finances. While traditional banks provide basic business checking or savings options, landlord-specific banking platforms offer features tailored for real estate investors, including:

- Separate accounts for each property

- Higher APY to grow your reserves

- Built-in tools for rent collection, expense tracking, and managing your emergency cash reserve

By contrast, traditional banks tend to offer lower APY rates and no support for property-level tracking. Accounting features often require third-party tools.

Comparing cash reserve account options for multi-unit investors

| Feature | Baselane | Stessa | Relay |

|---|---|---|---|

| APY | Up to [v="apyvalue"] APY² | 2.31% APY (higher for paid tier) | Up to 3.03% APY |

| Monthly Fees | $0 | $12-$28/month (free plan available) | $30-$90/month (free plan available) |

| Minimum BalanceRequirement | |||

| Separate Accounts Per Property | |||

| Accounting Integration | |||

| Rent Collection | ACH, Credit/Debit | ACH |

Traditional banks like Chase, Capital One, and U.S. Bank offer more familiar options, but often lack rental-specific tools or competitive interest rates. Here’s how they compare:

| Feature | Chase | Capital One | U.S. Bank |

|---|---|---|---|

| APY | 0.01% | 0.01% | 0.005% - 0.01% |

| Monthly Fees | $15-$95 | $15-$35 | $0-$30 |

| Minimum Balance | $2,000-$100,000 | $2,000-$25,000 | $10,000-$75,000 ($0 for free plan) |

| Separate Accounts Per Property | |||

| Accounting Integration | |||

| Rent Collection |

Landlords looking for a high yield on investment property cash reserves and integrated tools for managing rental property finances, traditional banks won’t check those boxes.

With no monthly fees, unlimited sub-accounts, and a competitive APY, Baselane is a top contender for the best cash reserve account for rental property owners.

Understanding investment property reserve requirements

Some lenders evaluate investment property reserve requirements in months of PITIA (principal, interest, taxes, insurance, and association dues) or total expenses. Document what applies to your loan type and maintain reserves that meet or exceed these minimums.

These reserves for investment property demonstrate financial stability to lenders and provide an operational cushion during portfolio expansion. Multi-unit investors often maintain reserves well above minimum lender requirements to support aggressive growth without liquidity constraints.

How to use sub-accounts for better reserve management

Managing reserves effectively requires separating funds by purpose and time horizon. Open separate sub-accounts for each reserve type within your banking platform. This structure helps keep funds organized, prevents capital reserves from being used for operating needs, and simplifies budgeting and reporting across properties and entities.

- One sub-account per rental unit or building for vacancy and repair coverage.

- Aggregate replacement funds at the LLC level for major systems (roof, HVAC, foundation).

- Dedicated accounts to meet state-specific security deposit requirements and issue security deposit receipts easily.

This multi-tier approach provides granular visibility into reserve health while maintaining clean entity separation for legal and tax purposes.

Why separating operating and reserve funds matters

Mixing reserve money with operating funds increases the risk of overspending reserves on non-emergency expenses. The best accounts for separating operating and reserve funds are those that support sub-accounts per property and clear labels.

A cleaner structure includes one account for day-to-day operating expenses and one or more reserve accounts dedicated to emergencies, repairs, and capital expenses. Clear separation improves financial discipline, simplifies reporting, and supports long-term portfolio stability.

Open a high-yield cash reserve account with Baselane

Building and maintaining a strong cash reserve is essential to running a successful rental property business, and the right banking solution makes all the difference. Baselane banking is purpose-built for real estate investors, offering:

- Unlimited sub-accounts to segment reserves by property or purpose

- Competitive [v="apyvalue"] APY² to grow your funds

- No account fees or minimum balance requirements

- Integrated bookkeeping for auto-expense tracking

Open your account today to start building and managing cash reserves systematically.

FAQs

What is a cash reserve account?

A cash reserve account is a dedicated, liquid account landlords use to cover rental property risks such as vacancies, repairs, and unexpected expenses. It is kept separate from operating accounts, so reserve money remains protected and traceable.

How does a cash reserve account work for rental properties?

Cash reserve accounts are funded over time and used only for predefined rental needs like emergency repairs or income gaps. The key requirement is liquidity, allowing landlords to access funds quickly without disrupting normal cash flow.

How much cash reserve should I have for a rental property?

Many property owners aim to hold three to six months of rent or fixed expenses per unit, adjusting based on property age, vacancy risk, and repair frequency. Older properties or high-turnover markets typically require higher reserve balances.

What type of bank account is best for rental property reserves?

High-yield savings accounts and money market accounts are commonly used for rental reserves because they balance accessibility and interest. The best option depends on withdrawal limits, transfer speed, and whether funds can be clearly separated by property or purpose.

What is the difference between a cash reserve account and a savings account?

A savings account is a general-purpose financial tool, while a cash reserve account is a savings account designated specifically for rental property risk. Many landlords use high-yield savings accounts as reserve accounts—the distinction lies in purpose and discipline, not account name.

How do I set up automatic cash reserve payments?

Automatic cash reserve payments are created by transferring a fixed amount or percentage of rent into a reserve account on a schedule. Baselane allows landlords to automate transfers between operating and reserve accounts so reserves grow consistently without manual intervention.

What are investment property reserve requirements?

Investment property reserve requirements generally refer to how much liquidity landlords should maintain to cover expenses during vacancies or repairs, and sometimes what lenders expect to see available. Requirements vary by loan type and risk profile, so landlords should document and consistently fund their reserve targets.

What are the best accounts for separating operating and reserve funds?

The best setup separates operating cash (rent inflows and monthly bills) from reserve funds used for repairs, vacancies, and capital expenses. Accounts that support clear labeling or sub-accounts help prevent accidental spending of reserves. Baselane supports dedicated accounts and sub-accounts so landlords can separate operating and reserve funds by property or purpose.

.jpg)