Managing rental income isn’t just about collecting payments; it’s about putting that money to work. A high-yield online savings account (HYSA) is a smart way to grow cash, whether you're saving for repairs, reserves, or security deposits. These accounts offer much higher returns than traditional savings, without sacrificing access to your funds.

In this guide, we’ll break down how high-yield online savings accounts work, why they’re ideal for rental businesses, and how to pick a bank that offers the best features and rates to support your financial goals.

Key takeaways

- An online high-yield savings account earns significantly higher interest than traditional savings, ideal for rental reserves, emergency funds, and security deposits.

- HYSAs are FDIC- or NCUA-insured, have low or no fees, and provide easy access to funds with no market risk.

- Online banking platforms offer high-yield savings rates, usually 3.00% APY or more, with fast, fee-free setup.

- Use multiple high-yield savings accounts to separate funds by property or purpose for better tracking and compliance.

- Automating transfers between HYSAs can help maximize ROI while keeping funds accessible for expenses.

What are high-yield savings accounts (HYSAs)?

A HYSA is a savings account that pays dramatically higher interest rates than the national average offered by traditional brick-and-mortar banks. A HYSA is where you put your reserve funds, security deposits, and any rental income you aren't immediately using for expenses.

Here's the simple breakdown:

- Higher interest rates (APY): You'll typically see rates of 3.00% or more, often 30 times the amount a traditional savings account might pay. With Baselane, for example, you can earn up to [v="apyvalue"] APY².

- Risk-free protection: Like all federally insured accounts, your deposits are protected up to $250,000 - $300,000 per bank by the Federal Deposit Insurance Corporation (FDIC).

- Easy liquidity: Unlike Certificates of Deposit (CDs) or other investment vehicles, you can access your funds when needed without penalties.

- Low-cost operation: Most top HYSAs, especially those offered by digital banking platforms like Baselane, have no monthly maintenance fees or minimum balance requirements.

In essence, a HYSA takes cash that's just sitting around waiting for a rainy day and turns it into a consistent, passive income stream

What are the benefits of a high-yield savings account

Some of the major benefits of a HYSA are as follows.

Multiply earnings on reserves and capital

Traditional bank savings accounts often offer interest rates as low as 0.01%–0.10% APY. HYSAs, conversely, typically pay rates of 3.00% or more, which can be up to 30 times what a conventional account offers.

By moving large balances of non-operational cash—such as funds for emergencies, vacancies, or capital improvements—to an HYSA, you convert that money from inert capital into an active, low-risk income source.

Letting $50,000 in reserves sit in a typical account at 0.10% APY would yield only $50 per year. In a competitive HYSA (e.g., 3.00% APY), that same money would earn $1,500 annually—a difference that can cover unexpected maintenance costs or offset operating expenses.

Preserve capital against inflation

Inflation poses a continuous threat to your financial well-being by eating away at the purchasing power of your cash over time. If your savings earn less interest than the rate of inflation, your money is effectively losing real value. A HYSA with a competitive interest rate offers a key defense against this loss, helping you counteract inflation's impact and safeguard the long-term strength of your reserves.

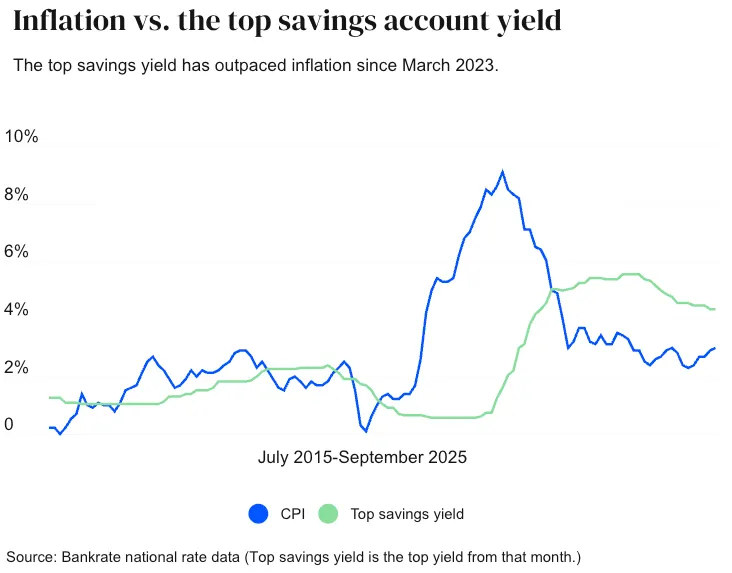

In fact, for the past two years, the highest savings yields, as tracked by Bankrate, have successfully kept pace with and even surpassed the inflation rate.

To illustrate the importance of earning interest, consider a simple example: Imagine spending $20 on goods and services in July 2019. If you had kept a separate $20 bill in a drawer, earning no interest, by July 2025, you would need $25.18 to purchase that same basket of goods, according to the U.S. Bureau of Labor Statistics’ CPI Inflation Calculator.

Because that $20 sat idle, inflation forced you to either reduce your spending or find an additional $5.18 to cover the cost. This starkly demonstrates the direct impact of inflation on stagnant savings. Keeping that money in a high-yield savings account earning a competitive yield would have performed much better against inflation than cash sitting idly at home. For context, since March 2023, Bankrate's top-yielding accounts have consistently remained ahead of the inflation rate.

Monetize required security deposits

In many states, landlords are required to hold tenant deposits in a dedicated account (known as escrow or trust account), which may or may not be interest-bearing. An HYSA is a perfect, compliant solution for this. Not only does it meet the legal requirements, but in many jurisdictions, you’re allowed to keep the interest earned on those deposits (less any administrative fee). This turns a legal obligation into an additional source of passive income for your business.

Read more about how to open an escrow account to hold a tenant’s deposit legally.

Maintain liquidity for emergencies

Unlike investment vehicles such as Certificates of Deposit (CDs), which lock up your capital for a fixed term and penalize early withdrawals, HYSAs provide easy access and high liquidity. You can quickly transfer funds to cover emergency repairs, address tenant issues, or sustain a mortgage during an unexpected vacancy.

Keeps your funds separated and organized

As CPA Mike Kelly, host of Money and Life TV, highlighted in one of our webinars, an LLC's legal shield is breached if you don't maintain a separate bank account for business funds. An HYSA inherently creates this necessary separation.

Furthermore, with Baselane, you can create sub-accounts within your HYSA, allowing you to segregate your business capital by specific purpose, such as:

- Security deposit account: A separate account for each tenant or property ensures compliance.

- Reserve account: Dedicated funds for covering repairs and capital improvements.

- Vacancy reserves account: Cash set aside to cover essential costs like mortgage payments and operating expenses when a unit is unoccupied.

Simplify bookkeeping and enhance financial reporting

Using a separate, structured HYSA for specific reserve purposes makes tracking cash flow infinitely easier.

Instead of sifting through dozens of transactions in one account to identify which funds are designated for which purpose, a segregated HYSA provides a clear, consolidated record of your savings activity. This drastically reduces the manual data crunching required and simplifies the process of generating accurate cash flow reports and Schedule E tax reporting.

Build a foundation for scalability

As your portfolio expands to multiple properties, units, or even different legal entities, the need for organization skyrockets. A landlord banking solution that offers unlimited HYSA accounts can help you scale your financial structure alongside your investments without the need to constantly open new, traditional bank accounts that often come with fees and minimum balance requirements.

This disciplined financial structure is also crucial when seeking further financing. Lenders require clear and organized financials to assess your property's performance and stability, making documentation straightforward and demonstrating professional management.

Comparing the yields offered by banks vs digital banking platforms

Digital banking platforms consistently offer superior yields because they have lower overhead costs than large, brick-and-mortar banks. While traditional banks like Chase offer a vast branch network and commercial lending options, they often impose high monthly fees and maintain minimal APY (sometimes as low as 0.01%) unless you meet minimum balance requirements.

Here’s a rundown of APY offered across traditional banks and digital banking platforms as of Dec’25:

Baselane ensures you avoid those fees and balance minimums while earning a high APY on the operational cash and reserves necessary to run your rental business. This small difference in percentage points is the key to maximizing your financial return without increased risk or effort.

How to best leverage a high-yield savings account

To maximize the benefits of an HYSA for your rental business, consider adopting these high-interest savings account best practices, focusing on strategic automation and financial precision.

Strategize to calculate your optimal reserve levels

You shouldn't rely on arbitrary savings goals. The best strategy is to fund your HYSA reserves based on calculated financial needs, which helps you avoid stress during vacancies or major repairs.

- Determine your fixed expenses rule: Maintain reserves covering three to six months of operating expenses per individual rental property. This buffer includes your mortgage (PITI), property taxes, insurance, and regular HOA/property management fees.

- Fund your CapEx (capital expenditures) contribution: Set aside funds specifically for large CapEx, like replacing a roof, an HVAC system, or major appliances. A general rule is setting aside a fixed amount per property, or performing a detailed Capital Spending Study, which provides a long-term view of when major repairs will be needed.

- Adjust reserves based on property risk: Adjust your savings goal based on the age and condition of your properties. Older properties require a larger reserve cushion due to higher maintenance risks, while newer or recently renovated properties may require a smaller reserve, as major updates have less remaining useful life.

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Automate to fund and replenish with precision

Automation is the simplest way to adhere to your budget and achieve consistency without effort, helping you take back time.

- Automate your savings: Set up automated transfers from your main rent collection (checking) account directly into your high-yield reserve accounts. This ensures your reserves are growing consistently without you having to manually remember to move money every month.

- Use the 10–20% rule: Set aside 10–20% of your gross monthly rental income directly into your HYSA reserves. You should apply the higher percentage for older or more seasonal properties to account for increased risk.

- Automate reserve replenishment: Set up automated rules to move money from your primary checking account (where rent is collected) back to your segregated HYSA accounts (where reserves grow). This ensures that after a large expense or repair is paid, your reserves automatically replenish to maintain target balances, saving you manual effort.

Organize using segmented accounts for clarity

Clarity is paramount for managing compliance and scaling effectively.

- Open a real estate-specific account: Look for platforms that integrate banking with management tools. Baselane offers unlimited real estate savings accounts that are purpose-built for real estate, along with automated bookkeeping and rent collection, all in one platform with no monthly fees.

- Set up segmented virtual accounts: Use dedicated accounts to separate funds for each property, unit, and reserve category—maintenance, security deposits, and taxes—to improve clarity and control. Separating your cash reserves into a separate, interest-bearing account prevents you from accidentally moving reserve funds into everyday operating expenses. You can even open separate bank accounts for multiple LLCs if that is your legal structure.

Protect your capital by understanding deposit insurance and tiering

When you're working with large cash balances, you must ensure your capital is protected and optimized.

- Advanced reserve layering (cash management tiers): You shouldn't keep all cash in one place. Instead, you should segment funds based on liquidity needs and return potential. This is often called "tiering" your cash.

- Tier 1: Immediate liquidity (HYSA): This holds 3–6 months of essential operating and vacancy reserves. This money prioritizes quick access and high APY.

- Tier 2: Excess capital (Short-term T-Bills/CDs): This holds funds you won't need for 6–12 months (e.g., future down payment savings). This capital can earn a slightly higher return in exchange for a short lock-up.

- Network bank coverage: For larger reserve pools, you need assurance that your capital is protected beyond the standard limit. While standard FDIC coverage is $\$250,000$ per depositor, per institution, Baselane works with a network of partner banks to offer significantly increased coverage—up to [v="fdic_short"]. This allows you to centralize large reserves without sacrificing coverage.

Earn high APY with Baselane

If you're holding reserves, security deposits, or rental income in a low-interest (or no-interest) account, now could be the best time to open a high-yield savings account. Open sub-accounts within Baselane’s high-yield savings account and earn up to [v="apyvalue"] APY² with no monthly fees or minimum balance requirements.

Ready to earn more passive income without adding any extra admin? Sign up today.

FAQs

What is the best bank to open a high-yield savings account?

The best choice depends on your goals, but online banks typically offer the highest rates and lowest fees. When comparing high-yield savings accounts, double-check rates aren’t promotional, and look for landlord-friendly features like multiple sub-accounts, auto-transfers, and no monthly fees. Check out our lists of the best banks for real estate investors and the best banks for Airbnb business owners.

What are the requirements to open a high-yield savings account?

Most high-yield savings accounts can be opened online. You’ll typically need a U.S. mailing address, government-issued ID, and either a Social Security Number or EIN. Check for monthly fees before signing up, so you don’t end up losing the extra money you’re earning.

Baselane high-yield savings accounts can be set up in minutes and don’t have monthly fees or minimum balance requirements–you get to keep everything you earn.

How often do high-yield savings accounts pay interest?

HYSA's interest is typically calculated daily and paid out monthly. Just be sure to compare current high-yield savings rates before choosing a provider. Read the fine print to confirm you’re getting the regular APY and not a promotional offer that drops your rate after a few months.

Are high-yield savings accounts safe?

Yes, most are insured by the FDIC (banks) or NCUA (credit unions) up to $250,000 per account. Choose a reputable provider offering the safest high-yield savings accounts with clear terms and no hidden fees.

Can I use a high-yield savings account to hold security deposits?

Yes, you can use HYSAs to hold tenant security deposits. Just make sure the account complies with your state’s requirements — such as separate accounts, interest accrual, or escrow handling if mandated (e.g., in New York, Massachusetts, Illinois).

Is interest earned on a high-yield savings account taxable for landlords?

Yes, interest income from a HYSA is reported as taxable income (usually via Form 1099-INT). You must declare it even if the funds are used for business-related reserves.

How can landlords separate funds by property using one HYSA?

With Baselane, you can open multiple sub-accounts or buckets within a single HYSA to track reserves per property (e.g., Property A: $5k, Property B: $10k). This helps with cash flow clarity and compliance.

Can I open a HYSA under my LLC or business entity for rental income?

Yes — but not all HYSAs allow business accounts. Landlords operating under an LLC should ensure the HYSA provider supports business ownership and EINs. Baselane and a few others do.

Should landlords keep security deposits and reserves in the same HYSA?

Not recommended. Security deposits should be isolated (often legally required). Instead, open a separate HYSA or sub-account labeled accordingly. This ensures compliance and makes bookkeeping cleaner.

Can I automate savings from rent income into my HYSA?

Yes — with the right platform, you can set rules (e.g., 15% of rent → HYSA) to automate reserve funding. This helps enforce discipline and ensures you’re prepared for big-ticket repairs or vacancies.

.webp)