Managing financial statements across multiple properties and LLCs means tracking dozens of revenue streams, entity-level expenses, and separate Schedule E filings — and a single misclassified transaction can ripple across your entire portfolio. This guide breaks down the three core financial statements — income statement, balance sheet, and cash flow statement — with a focus on how to use them to evaluate individual assets, optimize across your portfolio, and stay audit-ready in 2026.

Key takeaways

- The income statement, balance sheet, and cash flow statement work together to give you a complete picture of profitability, equity, and liquidity across every entity and property in your portfolio.

- Investors who generate monthly P&L statements by property report more confidence in their tax positions.

- Commingling funds remains the top reporting error, with 59% of accountants flagging monthly mistakes tied to mixed personal and business finances.

- Platforms like Baselane auto-sync transactions and categorize them by property and Schedule E category, reducing manual data entry and giving portfolio-level and property-level financial visibility.

What are real estate financial statements?

Rental property financial statement focus on asset value, depreciation, and cash flow specific to a rental portfolio. They offer insights into revenue, expenses, and overall profitability, as well as your real estate business’s liquidity and solvency. This could mean understanding exactly how much cash is available to cover mortgage payments, emergency repairs, vacancies, or to acquire new properties.

These reports also serve as a benchmark for securing loans. Lenders consider your eligibility based on the Debt Service Coverage Ratio (DSCR), which is derived directly from accurate income statements.

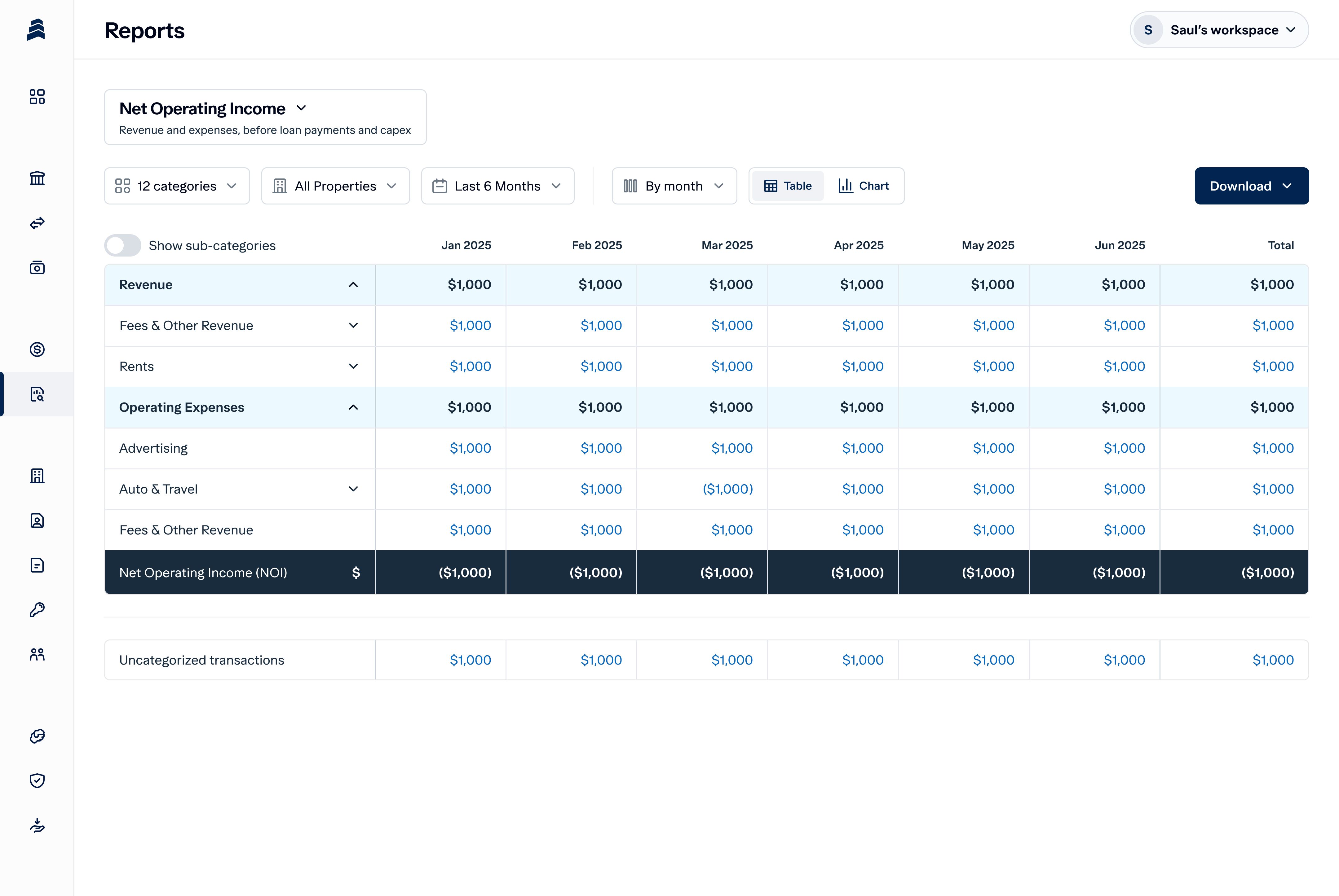

Real estate income statement (Profit & Loss)

The real estate income statement, often called a Profit & Loss (P&L), summarizes revenue and expenses over a specific period, typically monthly or annually. It helps you calculate Net Operating Income (NOI) and Net Profit.

Key components

- Revenue: All the income generated by the property. While rent is the primary source, rental income management also involves tracking late fees, parking fees, and laundry income.

- Operating expenses: Costs incurred to run and manage properties. Common items include property management fees, repairs, insurance, and utilities.

- Depreciation and interest: Unlike operating expenses, depreciation is a non-cash deduction that lowers taxable income. Calculate depreciation on rental property correctly to maximize tax benefits without affecting your actual cash balance.

Here’s what a sample real estate income statement looks like in Baselane. 👇

What is net operating income (NOI)?

NOI is a critical metric derived from the income statement and helps you understand your property's value. A lower NOI directly reduces your property's market value. It excludes debt service and capital expenditures.

Data indicates that a single missed rent escalation—such as a 3% increase on a $10,000/month base rent—reduces NOI by $3,600 annually until corrected. This seemingly small oversight can lower the property's valuation by over $50,000 at a 7% cap rate.

To track these figures effortlessly, many investors use a free rental property spreadsheet or upgrade to real estate accounting software.

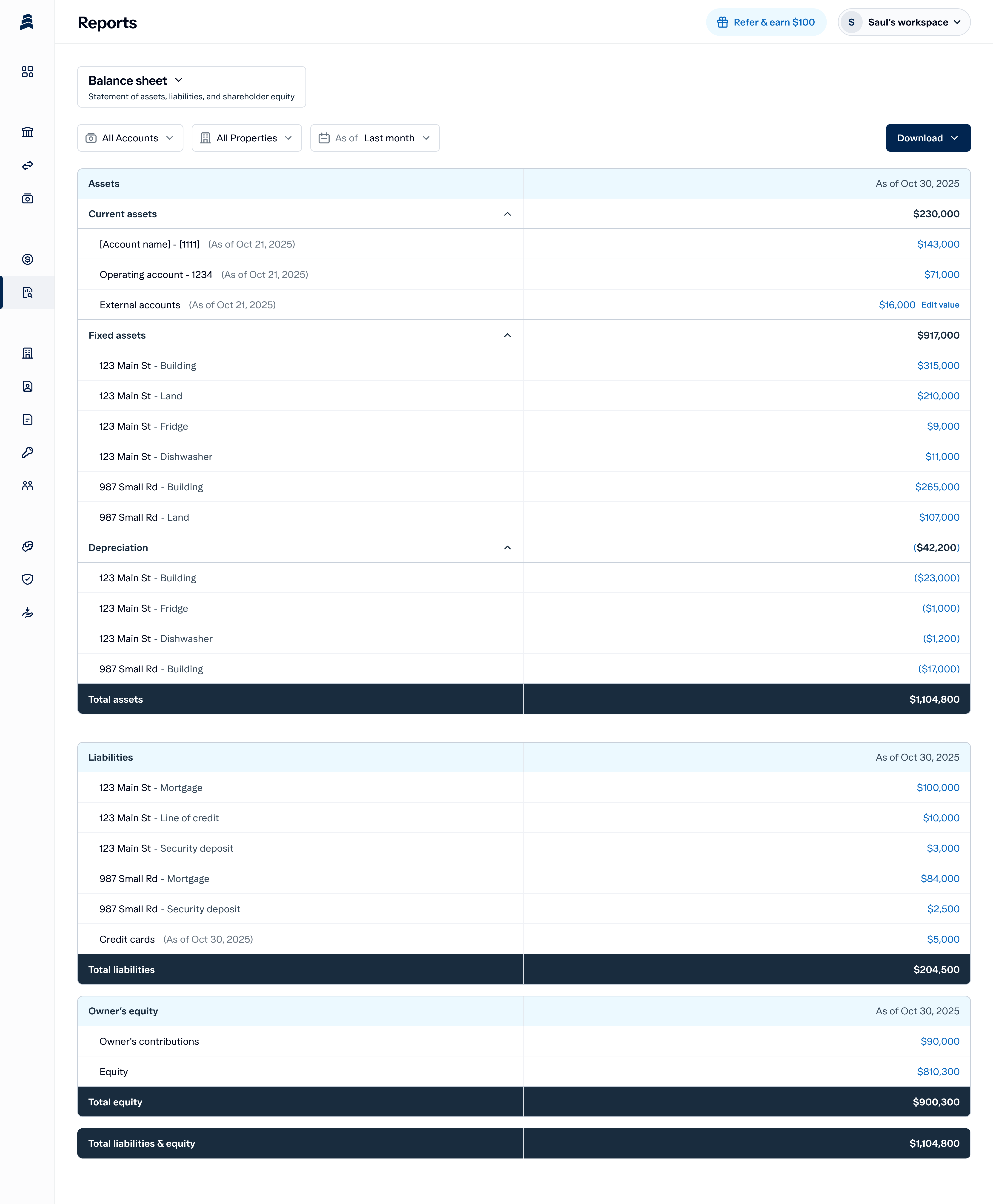

Real estate balance sheet

The real estate property balance sheet gives a snapshot of your financial standing at a single point in time. It outlines what you own (Assets), what you owe (Liabilities), and your net worth in the property (Equity).

Here’s what a sample balance sheet looks like in Baselane. 👇

Key components

- Assets: This includes the current market value of your property and cash in the bank. For tax purposes, the building value is separated from land value. Strategies such as real estate cost segregation can reclassify 20-40% of acquisition costs into shorter-life assets to accelerate depreciation deductions.

- Liabilities: This section lists mortgages, tenant security deposits, and any other loans.

- Equity: Represents your stake in the property. It increases as you pay down the mortgage principal and as the property appreciates.

Correctly tracking these items ensures you are ready for future tax implications, such as understanding bonus depreciation on rental property before it fully phases down.

Real estate cash flow statement

The real estate cash flow statement is often the most important report for measuring liquidity. Unlike the P&L, which includes non-cash items like depreciation, this statement tracks actual cash moving in and out of your accounts.

Profit does not equal cash. You can show a profit on your tax return but still have a negative bank balance if your mortgage principal payments are high. The cash flow statement reconciles these differences, showing cash from operating, investing, and financing activities.

Key components

- Operating activities: Net income adjusted for non-cash items (depreciation) and changes in working capital.

- Investing activities: Cash used for buying properties or major capital improvements (CapEx).

- Financing activities: Cash received from loans or paid out as mortgage principal.

Effective cash flow management software will automatically generate this statement, ensuring you never run out of liquidity for repairs.

Here’s what a sample real estate cash flow statement looks like in Baselane. 👇

Own your time,

not just your properties

Make your finances work harder, so you don’t have to.

Free 2026 rental property financial statement templates

Creating these reports from scratch can be daunting. To simplify the process, we have designed a free, customizable financial statement template for rental property that you can use to start measuring a property’s financial position.

Income/profit and loss statement template

Pre-formatted with Schedule E expense categories so you can track revenue and operating costs by property. Designed for investors managing multiple units or LLCs who need property-level P&L visibility without rebuilding reports from scratch each month.

Balance sheet template

Organized sections for property assets, outstanding loans, and accumulated depreciation across your entire portfolio. Compare equity positions property by property and identify which assets are building wealth versus dragging on your net worth.

Cash flow statement template

Built-in formulas that adjust net income for non-cash items like depreciation and reconcile the gap between paper profit and actual liquidity. See exactly how much cash each property generates after debt service — so you know where to reinvest and where to hold reserves.

How to leverage financial statements to make strategic decisions

Once you have your statements, the next step is analysis. This involves comparing data to spot trends and measuring performance against industry benchmarks.

Horizontal and vertical analysis

Horizontal analysis involves tracking trends over time, such as comparing utility costs in 2026 versus 2025.

Vertical analysis looks at expenses as a percentage of revenue; for instance, it identifies whether rental property expenses exceed the typical 35-45% operating expense ratio.

Ratio analysis and key metrics

Successful investors rely on specific KPIs.

- Cap rate: A typical desirable Cap Rate is ≥7%. This measures the property's return independent of debt.

- DSCR: Lenders typically look for a Debt Service Coverage Ratio of ≥1.25, meaning your NOI is 1.25 times your debt payment.

- Cash-on-cash return: This measures the cash return on the actual dollars you invested.

When analyzing these metrics, always consider the tax impact, including the depreciation recapture tax rate upon sale, and strategies for no taxes on rental income using lawful deductions.

Common mistakes & challenges in real estate financial reporting

Even when you’re a few years into the business, it’s natural to make some errors. Avoiding these pitfalls is essential for protecting your portfolio.

Commingling funds

The most frequent error is mixing personal and business funds. This pierces the corporate veil and makes bookkeeping a nightmare. The solution is simple: open a dedicated bank account for property owners and strictly separate transactions using a business bank account for rental property.

Misclassifying expenses

Confusing repairs (deductible immediately) with capital improvements (depreciated over time) is a major tax risk. Clear policies are needed to distinguish between fixing a leaky faucet and replacing a roof. Using a dedicated business vs personal bank account helps clarify these transactions during an audit.

Complex security deposit accounting

Security deposits are not income; they are liabilities. Mishandling these funds can lead to legal penalties. Use specific security deposit accounting practices, often requiring a separate account. Learning how to open an escrow account for rent ensures compliance with state laws. Specialized escrow management tools can automate this compliance.

Compliance and tax nuances

In 2026, tax laws regarding depreciation continue to evolve. For example, Section 179 and bonus depreciation options are phasing down. Using property tax software ensures you stay ahead of these changes and don't miss deductions.

Get real-time financial visibility with Baselane

By mastering the income statement, balance sheet, and cash flow statement, you move from reactive management to proactive growth.

Baselane offers an all-in-one financial platform for multi-property real estate investors. It integrates banking, rent collection, and bookkeeping for multiple properties and entities under one login. Cash flow, P&L, balance sheets, and other reports are generated automatically, giving you instant visibility to make decisions.

Take control of your financial future by signing up for Baselane and getting visibility into your property’s finances.

FAQs

How to read financial statements for real estate?

To read landlord financial statements, start with the Income Statement to check Net Operating Income (NOI). Then, review the Balance Sheet to assess leverage and equity, and finally, check the Cash Flow Statement to ensure the property generates positive liquidity after debt service.

What is the difference between NOI and Net Income?

Net Operating Income (NOI) measures the profitability of a property before mortgage payments and taxes are deducted. Net Income includes these costs, as well as depreciation, providing the final bottom-line profit or loss for tax purposes.

Can I use a standard business P&L for rental properties?

While possible, it is not recommended because standard P&Ls lack real estate-specific categories like "Capital Expenditures" or "Vacancy Losses." A real estate-specific template or software ensures you track metrics like Cap Rate and comply with Schedule E tax reporting requirements.

.jpg)

%20(1).jpg)